Omank Naithani (28) hails from a small town in Uttarakhand where his parents continue to reside. A mechanical engineer by profession, Omank is employed by a company in Chennai and is right now pursuing a course in IIM Ahmedabad which has been sponsored by his company through a soft loan.

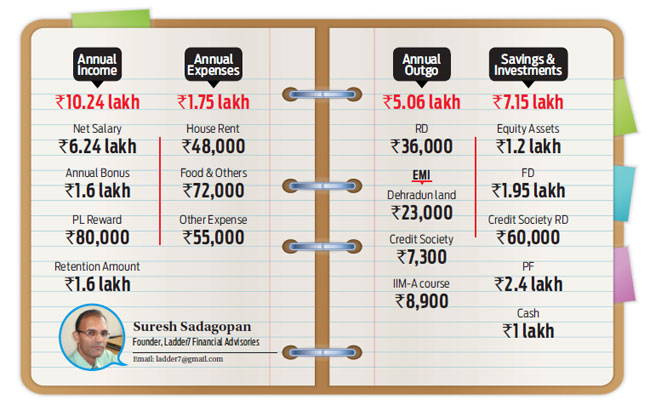

The year 2016 will bring in a lot of change for Omank as he gets ready to tie the knot. Looking at his finances, Omank seems to be doing very well. He has even thought about his retirement, even though the provisioning for it is still hazy and hopefully it will take a more realistic shape in coming years. To begin with, Omank’s insurance requirements are taken care of, which is very impressive. Also, liquidity or contingency provisions are in place and well taken care of. His expenses, too, are very much under the thumb. In fact, for a young person, he is showing exemplary restraint in his spending habits.

Looking at his investments, though he understands the need to invest, the instruments that he has chosen leave a lot to be desired. His biggest mistake is that he is having bulk of his investments in debt instruments as opposed to equity-oriented assets. At his age, he can have a high preponderance of equity assets. His monthly surpluses are going towards RDs in credit society. RDs offer low returns and interest earned on them is fully taxable. He should move at least 50 per cent of this monthly investment to equity oriented mutual funds.

For his marriage scheduled this year, Omank has a requirement of about Rs.4-5 lakh. He may have to liquidate his investments for that, which can part-fund this. He should also consider withdrawing some amount from his PF for this purpose. Since he gets a bonus every quarter and there is also a performance linked incentive provided by his company, withdrawal from all these will help fund his marriage related expenses. He can also go for a loan from the credit society.

Omank seems keen on acquiring properties and putting them on rent. Properties can be a part of one’s portfolio but one need not go overboard. Besides, residential properties give a mere 2 per cent net return annually which means one will continue to get low returns on such investments for a very long time and hope to make up for it through capital appreciation. Commercial property returns are higher but all properties have the headache element in terms of managing them—following up and collecting rent maintenance and repairs of the premises, dealing with brokers, intransigent tenents, etc.

A well-diversified portfolio is what he should endeavour to build. Future surpluses should hence be directed towards equity-oriented assets. He should buy a home at a later point in life, after he has saved enough to pay the upfront amount of about 25 per cent as well as after he has decided where he would settle down. Else, he would buy property in one city and may have to move out and stay on rent in a different city, beating the purpose of buying a home.

A plan to act on

Emergency Fund

■ He has a buffer of Rs.1 lakh in cash which is good enough to provide a decent cushion against any emergency that might arise

■ Along with this, his quarterly bonus and performance linked incentives also are available to provide enough liquidity. At the moment, the liquidity that is available seems adequate. A seperate contingency provision may not be needed as of this moment

■ His parents are not financially dependent on him. They are also medically covered through the medical insurance that his younger brother has, as well as the one that is made available to him by his employer, making them adequately covered

Insurance

■ He has taken a term insurance of Rs.1 crore from HDFC Life and pays a premium of Rs.14, 000 per annum. He has another LIC policy, Jeevan Saral, with a sum assured of Rs.5 lakh, where he pays Rs.2, 000 per month

■ Since he has no dependants and the loan is about Rs.25 lakh only, the cover he has may be higher than necessary. But then, he would get married this year and he would anyway need a higher life insurance cover. Hence, the cover can be retained

■ He has medical insurance through the employer which covers full medical expenses. Parents are covered by his company’s insurance and even more comprehensively through his younger brother’s family insurance

Marriage

■ He has a requirement of about Rs.4-5 lakh for marriage in 2016. Omank may have to liquidate his investments for that, which will part fund this

■ He can consider withdrawing some amount from PF. He would be getting a bonus every quarter and a performance linked incentive which probably will round off what he needs

■ He can also take a loan from the credit society, if necessary

Car

■ He has plans to buy a car worth Rs.6-7 lakh in the next 1-1.5 years

■ He could accumulate Rs.4 lakh from his PL incentive, bonus and retention amount (amounting to approx Rs.3.5 lakh) coming this year and the next. The remaining balance would have to come from loan

■ But, servicing a loan, even a small one could be a problem as the surplus is very low. Hence, it is suggested that he goes for a small car amounting to Rs.4 lakh

Home

■ He intents to sell the property in Dehradun and use it for buying a house. The realisation is expected to be about Rs.30 lakh after five years after paying off the outstanding loan

■ The balance amount would need to come from savings and loans. The value of the property itself will depend upon which part of the country he would be buying the property in

■ At the moment, Omank himself is not sure where that would be and hence the value is not known

■ Also, it would depend on whether his wife would be working and if she will be able to contribute some money towards the property, as well as the loan repayments

■ Omank should evaluate this at the end of five years and go in for a property only if it is going to be feasible without over-stretching his finances.