At 39, Mumbai-based Prashant Dixit is excited about planning his retirement six years later. He is one of those young Indians who are looking at taking an early retirement; much before they turn 60, the age long considered ideal for retirement. Today, retiring early is perhaps one of the top goals among working Indians. Achieving this goal, however, is not easy in the absence of good old-fashioned planning. So what are the elements of a sound “retireearly” plan? The sooner you start a plan, the more financially secure you can be in later years.

First of all, retirement is not an individual decision. It is a decision that you need to make with your spouse and family. While it is tough to decide when you want to retire, it is equally tougher these days to choose where you want to retire. Most people work in multiple cities through their careers, which makes it a difficult task to zero down on which city to eventually retire in. However, this should not be the reason to postpone planning for your retirement.

Start early, retire rich

When it comes to savings for retirement, most tend to wait; infact, delay the start as they feel they have plenty of time. The advantage of starting early on the other hand, however small a start it may be, is far better than the impact the cost of waiting can have on your retirement balance. “Someone in their 30s may not have an idea of the exact expenses after retirement which makes it difficult to estimate expenses in retirement at this stage. In such a situation one should compare income to expenses and go with a 75-80 per cent of the current income figure to save for,” advises Hemant Beniwal, CFP, Principal Financial Planner, Ark Financial Planners.

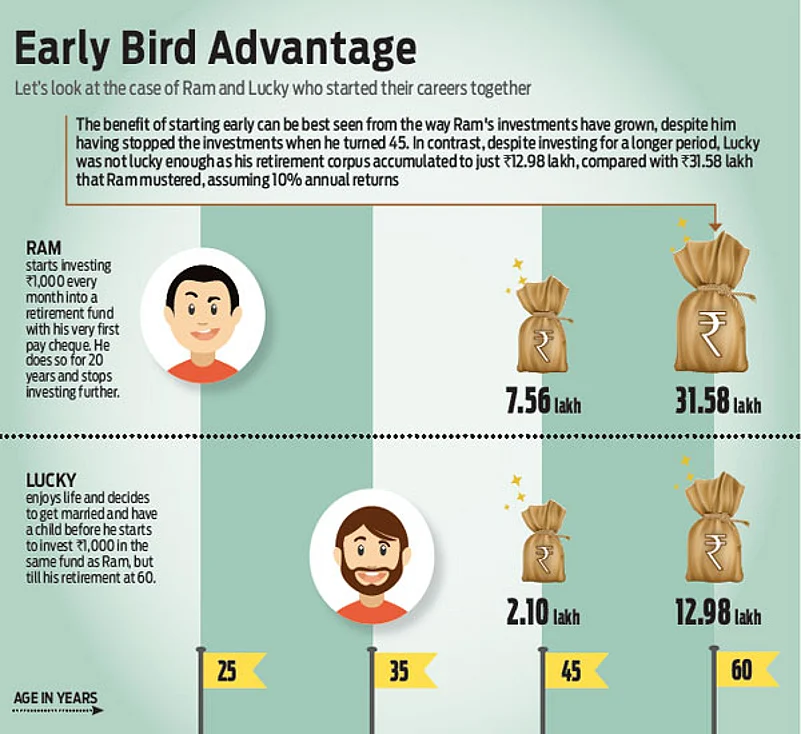

Like every other financial goal, there is a cost of delaying, which could be significant on how long you delay. Here’s an example. Two friends—Ram and Lucky—start working for the same company at age 25. During their first 10 years there, Ram saves Rs 1,000 a month through a retirement plan, while Lucky saves nothing. After 20 years, Ram stops contributing entirely. Meanwhile, after a decade of no savings, Lucky starts saving at age 35, saving that same Rs 1,000 a month. But unlike Ram, Lucky continues investing till he retires at 60. Ram has put only Rs 2.4 lakh into his account while Lucky has saved Rs3 lakh. But because Ram started sooner, he has Rs31.58 lakh in his account at retirement, versus only Rs12.98 lakh lakh for Lucky,assuming they both earn 10 per cent a year on their money (See: Early Bird Advantage). That’s the power of time and compounding.

Says Sunil Subramaniam, CEO, Sundaram Mutual: “The moment one starts earning a regular income, they should start retirement planning. The earlier the better because the power of compounding can come to aid that much more.” In your 20s you have your first proper job with a proper salary, and even though retirement may seem a long way down the future, the mandatory contribution to the provident fund scheme is a good option to take seriously and get used to. Another reason for most people to stay away from planning their retirement early on is the fact that they tend to be risk averse and stay off investing for their retirement.

Take the case of Mumbai-based couple Soniya and Bhaven Doshi who have fairly different risk profiles. When it comes to saving for retirement, both agree that it is a priority for them. “I seriously started looking into retirement planning only a few years after I got married in 2011,” says Soniya. In contrast, Bhaven has been planning for retirement from the day he got his first pay cheque. “My dad educated me on the investment opportunities from tax saving and retirement perspective,” he says. The two are very concerned about their retirement and ensure that it is one financial plan that they do not wish goes wrong.

Giving shape to a retirement plan

You have several choices to save and invest your money for retirement. You don’t have to pick just one, and in fact, many people use a combination of different types of plans to achieve their retirement savings goals. There are numerous financial instruments from the traditional bank deposits to those that are tailored towards retirement like the NPS, retirement-linked mutual funds and the provident fund.

“Broadly, like any financial plan, you have to put your money in a mix of assets—fixed return and market-linked,” says Kolkata-based Arup Mitra, 46. Mitra has parked his money into mutual funds, insurance, banks and even stocks to manage his finances, including his retirement.

“Retirement mutual funds are one of the most tax efficient ways of saving for retirement in the Indian context as per the current tax laws, while working beautifully like a pension scheme”, says Ashok Kanawala, Head - Products, HDFC AMC. Kanawala adds that HDFC AMC has a tailormade scheme for those looking to save for their retirement.

“HDFC Retirement Savings Fund,an open ended notified tax savings cum pension scheme with no assured returns, is a mutual fund vehicle targeting retirement corpus for an investor with a lock-in period of 5 years. Upon completion of 5 years, the units can be redeemed with an exit load of 1 per cent till the age of 60. After completion of 60 years, the investor can redeem the units without any exit load,” Kanawala says.

There are financial instruments like the ubiquitous Employee Provident Fund (EPF) and the Public Provident Fund (PPF) which offer fixed returns on contributions towards retirement, and also market-linked products like the NPS, retirement options from life insurers and mutual funds.

Your choice of financial instruments depends a lot on your risk profile, which means you need to be careful to evaluate the risk-adjusted returns from each investment product and its ability to help you achieve the target. The concept of risk-adjusted returns evaluates returns from different investment products on the basis of risks that are taken to achieve those returns. For most risk averse Indian investors, the choice rests with the fixed return instruments, which address concerns over risks, but fail to achieve returns which can help build wealth in the long run.

There are several instruments in which you can deploy money to build a retirement corpus. For instance, if you are not part of a formal employment to make contributions towards the EPF, you may consider a closer cousin—Public Provident Fund (PPF), NPS, Mutual funds and even insurance plans which have an accumulation component. “These days, companies also offer a choice by encouraging contributions to the NPS, instead of the EPF,” says Sumit Shukla, CEO, HDFC Pension. The New Pension Scheme or NPS is a perfect retirement product open to all individuals across the country. In fact, there is an additional Rs 50,000 deduction to grab under Section 80CCD (1B) this financial year.

Money flow in retirement

If you have planned well so far, you will find that when you actually retire, you will have enough money to live off peacefully. “As the only earning member in my house, there have been so many pressing financial needs to manage. You need to strike a balance to contribute towards retirement, savings as well as manage your life,” says 53-year-old Mumbai-based Mandar Bhatt, 53. Yet, with deft planning, he has a plan that he is putting to good use, by way of owning the house in which he is staying and savings which he thinks will help him in his retirement.

Typically, the best retirement plan is the one which starts paying you money the moment you stop working for money. Although there are several products that focus on the accumulation phase, there are very few financial instruments to take care of the payout phase or income flow in retirement. One of the reasons for the popularity of products favouring accumulation is the available tax exemptions, unlike annuity, which is treated as income and taxed accordingly.

It, thus, becomes very important to make income in retirement tax efficient. There are several ways to do this—one way is to park your money in instruments that are tax free at the time of redemption such as the EPF and the PPF. The other way out is to put money in financial instruments that can be used in a tax efficient manner in retirement, such as investment in stocks and mutual funds. These are so structured that you can redeem your investments after just one year of holding in equity and related schemes for long-term capital gains to kick-in, which is nil in their case.

There is also the systematic withdrawal option available when investing in mutual funds so that you can create an income stream depending on your needs through investments in equity mutual funds. This way you can create an income stream to meet your needs. “I have savings and investments in a mix of assets, which I know can be used depending on my needs when I retire,” explains Mitra. There are several others who have two homes — one to live in and the other to live off. There are also ways in which you could structure investments in fixed return instruments like the NSC and even bank deposits to work as an income stream by timing their maturity.

Whatever be the way, remember that changing social norms are pointing more towards the need to be selfreliant during one’s sunset years. To do that you need to not just start early, but also do so smartly by using a mix of financial instruments to maximise your returns.