From dining tables to boardrooms, conversations in recent times have revolved around three interconnected topics of rising crude oil prices, weakening rupee, and volatile markets, in the wake of the US-Iran conflict. Together, the troika form a powerful economic equation that affects household spending, corporate earnings and investment decisions.

Hedge Against Rupee Volatility

The recent US-Iran peace agreement and measures by the government and RBI have helped contain rupee volatility, but uncertainty remains. Here is what it means for you and why your financial strategy should be above and beyond such movements

Advertisement

Higher crude oil prices and capital outflow from the market affect the rupee. A weaker rupee increases the cost of imports as India imports more than it exports, putting pressure on inflation and household budgets. At the same time, market volatility influences investment returns, retirement savings and wealth creation. All this put together typically makes investors risk averse.

A potential easing of geopolitical tensions could help stabilise crude oil prices, ease pressure on India’s import bill and provide some support to the rupee. “Indian currency had weakened quite sharply in the last few months, hence any positive development in the resolution of the West Asia crisis will provide a reprieve to the currency,” says Rajani Sinha, chief economist at CareEdge Ratings.

Though the US-Iran peace talks have kindled hope with the rupee recovering 2 per cent from its May low, nothing is certain. The ongoing Israeli strikes in Lebanon and Iran’s threat to shut the Strait of Hormuz again have kept tensions simmering. With uncertainty still clouding global markets and the rupee being under pressure for the last two years, fears over the currency’s future direction continue to persist.

Advertisement

The Story Behind The Fall

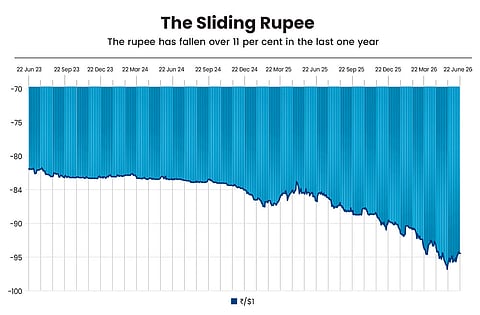

The rupee slid to an all-time low of 96.84 against the dollar on May 20, 2026. It fell around 6.50 per cent since the US-Iran conflict, which started on February 28, 2026. In the last one year, it has fallen 11.56 per cent as on June 22, 2026.

From rising crude oil prices that have inflated India’s import bill to persistent foreign capital outflows amid global uncertainty, a combination of domestic and international factors have weighed on the rupee recently.

US-Iran Conflict: The currency has been under pressure for the past two years, but the pace of depreciation intensified during the US-Iran conflict as crude oil became costlier. As India imports 85 per cent of its oil and pays for it in dollars, the rise in oil price puts pressure on the rupee.

Concerns over a widening trade deficit on the back of elevated crude oil price, a stronger dollar, elevated global interest rates and foreign portfolio investor (FPI) selling pressure added fuel to the fire.

Advertisement

Historically, periods of sharp increases in crude prices have often coincided with the rupee weakening.

FPI Outflow: When the US economy remains strong and interest rates in the US rise, global investors tend to move money into dollar-denominated assets as they are considered safe havens. The risk-return matrix plays a crucial role here; the US 10-year Treasury Bonds are currently offering 4.50 per cent yield with relatively lower risk. In such a scenario, FPIs pull out money from emerging markets such as India and move it to the US. This increases demand for the dollar as they convert rupees to dollars and the rupee weakens.

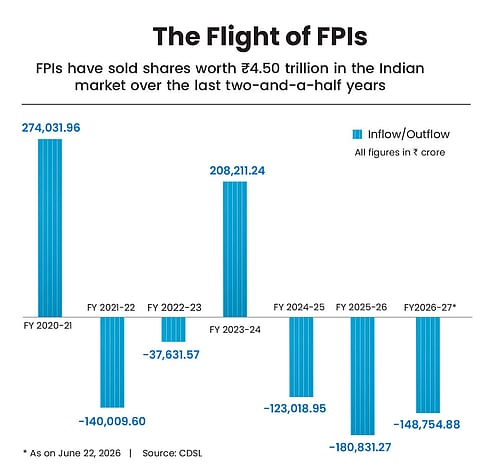

Since financial year 2024-25 till date (as on June 22, 2026), FPIs have been net sellers in the equity market and have sold equity worth `4.52 trillion. The reason behind the massive sell-off is poor performance by the Indian equity market compared to its other global counterparts, such as China, and South Korea, among others.

Advertisement

Another factor contributing to FPI outflows from India has been the growing enthusiasm for artificial intelligence (AI)-linked companies, which has attracted massive investor interest in the US, with technology and semiconductor giants emerging as the biggest beneficiaries of the trend. The strong performance of AI-driven stocks, coupled with a resilient US economy and higher interest rates, has made US markets increasingly attractive. Consequently, foreign investors have trimmed their exposure to Indian equities and shifted capital to technology-focused investments overseas.

Also, wars, geopolitical tensions and economic uncertainty typically drive FPIs towards safe-haven assets.

What’s India Doing?

The Reserve Bank of India (RBI) and the government have come up with several measures to improve India’s balance of payment (BoP). RBI monitors currency markets and intervenes when volatility becomes excessive. Even in the past, RBI has taken measures to contain rupee fall.

In its June monetary policy, RBI introduced a dollar-rupee forex swap facility for Foreign Currency Non-Resident (Bank), or FCNR (B), deposits mobilised by banks for a period of 3-5 years. The facility will remain available until October 16, 2026, for eligible deposits raised between June 8 and September 30, 2026. RBI said it would bear the full hedging cost on fresh FCNR (B) deposits of 3-5 year maturity mobilised by banks until September 30, 2026. The move is part of a broader set of measures aimed at boosting foreign currency inflows amid pressure on the rupee.

Advertisement

The RBI introduced a dollar-rupee forex swap facility for FCNR (B) deposits as part of a broader move to boost foreign inflows

Following RBI’s announcement, several lenders have revised their FCNR (B) deposit rates upwards. The State Bank of India (SBI), the country’s largest lender, raised rates by around 300 basis points (bps) across similar tenures. For deposits of up to $1 million, SBI now offers 5.25-5.75 per cent on 3-5 year deposits. For deposits above $1 million, the rates range between 5.50 per cent and 6 per cent. HDFC Bank, the country’s largest private sector lender, has increased rates by 235-265 bps, and is now offering up to 6 per cent on deposits with maturities of 3-5 years. Other banks have also increased rates on FCNR deposits.

“RBI’s measures for FCNR (B) and External Commercial Borrowing (ECB) can attract up to $70 billion,” wrote BNP Baribas in a recent report. It added that the government’s easing of taxation on foreign institutional investors (FIIs) should increase foreign participation in the bond markets and would also be incrementally positive for the inclusion of Indian government securities (G-secs) in global indices. On June 6, 2026, the Indian government enacted an ordnance exempting FIIs from taxes on G-secs. The ordnance eliminates the 12.50 per cent long-term capital gains (LTCG) tax and 20 per cent withholding tax on interest, making these returns entirely tax-free for foreign investors.

Advertisement

Post these measures, BoP for FY27 can potentially move to surplus as against a deficit for the last two years, which reduces the near-term risk of sharp currency depreciation, the BNP Paribas report added.

Says Sinha: “The Indian currency has already seen some strengthening in response to the recent measures by RBI and the government to incentivise capital inflows. We expect the rupee to average 92-93 per dollar over FY27, assuming early resolution of the West Asia crisis and global crude oil prices averaging $90 per barrel during the year.”

When RBI announced a fresh FCNR (B) mobilisation scheme and concessional swap facility in its June 2026 monetary policy, markets immediately drew parallels with September 2013. This eventually mobilised nearly $34 billion, stabilising the rupee and restoring confidence in India’s external position.

However, experts say that though the instrument may be the same, the macroeconomic backdrop is fundamentally different. Says Sneha Pandey, fund manager-fixed income, Quantum Mutual Fund: “In 2013, India needed dollars. In 2026, it is seeking to strengthen an already robust external position while improving domestic liquidity and lowering the economy’s cost of capital. With foreign exchange reserves above $680 billion, a manageable current account deficit and stronger financial sector fundamentals, this looks less like a crisis response measure and more like a proactive balance-sheet optimisation exercise.”

Advertisement

What It Means For You

For most people, the movement of the rupee against the dollar appears to be a distant economic statistic flashed briefly on television screens. Yet, every decline in the rupee has consequences that affect households, businesses, and investors. What begins as a movement on a currency chart soon translates into higher costs, changing spending habits and pressure on family finances.

Pain For Consumers: A weaker rupee makes imports expensive. India imports crude oil, electronic components, machinery, fertilisers and other industrial inputs. When the rupee depreciates, the cost of these items rises. Higher import costs eventually get passed on to consumers in the form of increased prices which results in inflation.

A weaker rupee also increases the cost of overseas education. Families with children studying abroad end up spending more rupees to meet the same expenses. For instance, if you are sending money to your child studying abroad and the exchange rate moves from `80 to `90 per dollar, then a tuition fee of $10,000 that earlier required `8 lakh would now require `9 lakh, an additional burden of `1 lakh without any increase in the actual fee. Similarly, expenses on accommodation, food, insurance and travel rise in rupee terms, putting further pressure on family finances.

Advertisement

Mixed Bag For Investors: The impact on investors varies across sectors and asset classes. Export-oriented sectors such as IT, pharmaceuticals and specialty chemicals benefit as their foreign earnings translate into higher rupee revenues. However, import-dependent firms can face margin pressure.

Gold often becomes attractive as domestic prices tend to rise when the rupee weakens. International funds investing in overseas markets may also gain from currency depreciation.

A falling rupee does not affect everyone negatively. For instance, NRIs benefit as their remittances gain in rupees terms.

What Should Investors Do?

Currency movements are a part of the economic cycle, influenced by factors, such as global interest rates, crude oil prices, trade balances and investor sentiment. Says Pandey: “For investors, the opportunity is not necessarily about making a binary call on the rupee or attempting to predict the exact scale of FCNR inflows. The more relevant question is how investors should position their portfolios in a market where liquidity is improving, government borrowing risks are easing, and interest rates may gradually decline.”

Advertisement

The key is to focus on long-term financial goals and hedge against currency fluctuations for goals such as foreign education

Equity markets are driven by multiple factors, including corporate earnings, economic growth and valuations. While some sectors may face headwinds, others may benefit. A diversified portfolio is better equipped to handle currency volatility.

For debt fund investors, dynamic bond funds merit consideration. “Unlike traditional duration-oriented funds, dynamic bond funds have the flexibility to actively adjust portfolio duration, maturity profiles and asset allocation as interest rate expectations evolve,” says Pandey.

If FCNR-related inflows, ECB issuance and improving liquidity conditions create room for lower yields, a dynamic approach may be better to capture opportunities across different segments of the curve rather than being locked into a static duration profile, she adds.

The key is to stay focused on long-term financial goals. Also, it makes sense to hedge against currency fluctuation for goals such as foreign education. Vishal Dhawan, CEO, Plan Ahead Wealth Advisors, a Sebi-registered investment advisory firm, says: “There are two ways to hedge. One, by investing in an appropriate investment instrument in that particular currency in which you need to fund the end goal, by matching the appropriate asset class with the time horizon. Second, by sending money out in advance to the destination where you need funds so that you are protected. But keep in mind the Foreign Exchange Management Act (FEMA) rules and Liberalised Remittance Scheme (LRS) limits applicable to holding money overseas without investing.”

Advertisement

Other experts also call for factoring in country and currency risk in asset allocation. Says Lovaii Navlakhi, managing director and CEO of International Money Matters: “Asset allocation starts with determination of country and currency risks, which investors tend to ignore. Further, in the long run, the difference in interest rates between the US and India will be the rate of depreciation of the rupee though there could be temporary swings with extremes which ultimately get normalised.”

For most investors and households, prudent financial planning remains a far more important determinant of financial well-being than the daily movement of the exchange rate.

kundan@outlookindia.com

Show comments

Published At:

Tags