For most of 2025, the uncertainty on US trade tariff kept the markets on the edge. The year 2026 has come with far deeper challenges: the Middle East crisis, a weakening rupee, persistent selling by foreign institutional investors (FIIs), the fear of a slowing economy, and interest rate hike, which have all rattled investors. After being among the strongest-performing equity markets globally for several years, India has recently slipped behind some international peers.

India's Best Funds: Should You Continue Your SIPs, Diversify Into Global Stocks?

A list of top-rated mutual funds in terms of performance

Advertisement

The mood has changed drastically since the end of 2024. At the time, equity markets saw record inflows through systematic investment plans (SIPs), mid- and small-cap funds were delivering superior returns, and first-time investors who entered the markets post 2020 were excited and optimistic. Mutual funds became part of everyday financial conversations.

The first signs of discomfort came at the beginning of 2025, when valuations stretched on the domestic front, and attractive bond yields made developed markets attractive for foreign investors. Then came the uncertainty over US trade tariffs. Concerns over global trade disruptions created nervousness across equity markets.

FII money that had once chased growth opportunities in emerging markets started moving back. This year, geopolitical tensions in the Middle East has added another layer of uncertainty. Till May 23, 2026, FIIs have sold equity worth over Rs 2.22 trillion year-to-date (YTD).

The strong outflow has jolted the market, in turn affecting the performance of mutual funds. Several diversified equity funds that once delivered annual returns of 20-25 per cent are now struggling to generate even low double-digit gains. SIP investors who started investing during the peak euphoria phase are experiencing flatter returns now.

Advertisement

Eroding Confidence In SIPs

Several investors are now questioning the effectiveness of SIPs. Many of them have never seen a phase of higher volatility or subdued returns. A large number of retail investors started their SIP journeys during the post-pandemic bull run when the benchmark indices were scaling new highs.

The growing dominance of SIPs in MFs’ assets under management (AUM) has amplified the discussion. According to data from the Association of Mutual Funds in India (Amfi), as of April 2026, SIP assets account for over 20 per cent of the industry’s overall AUM.

This is not the first time that SIPs have come under scrutiny. In the past, whenever the markets witnessed a sharp fall, SIP investors, particularly those who enter the market at a peak, have questioned their effectiveness.

In the past, whenever the markets fell sharply, SIP investors who entered the market at a peak have questioned their effectiveness

Advertisement

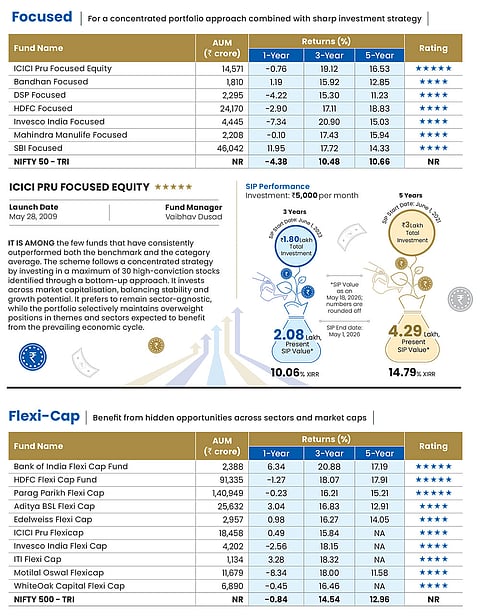

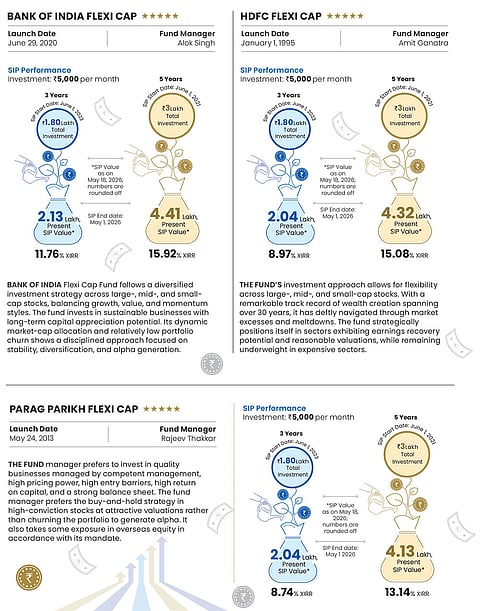

Reality Check: We ran some numbers to check the scale of negative returns, assuming an SIP of `5,000 per month, which started on June 1, 2024, and was continued till May 18, 2026. In the large-cap category, 20 out of 31 schemes delivered negative SIP returns over the last two years, with losses ranging between -4.59 per cent and -0.62 per cent. The trend is not limited to large-cap funds alone. The flexi-cap category, which is considered relatively agile because of its freedom to invest across market capitalisations, has also struggled. Out of 39 flexi-cap schemes, 20 generated negative SIP returns during the same period. Similarly, focused funds which typically run concentrated portfolios with high conviction bets have also failed to shield investors from market weakness. Out of 28 focused schemes, 15 generated negative SIP returns during the same period.

However, if you look at long-term performance over a 10-year period, none of the schemes in the above categories have delivered negative returns. For instance, all 23 large-cap schemes that have been in existence for at least the last 10 years have generated positive returns, ranging from a high of 14.60 per cent by Nippon Large Cap Fund to a low of 9.31 per cent by PGIM Large Cap Fund. Similarly, all the 20 flexi-cap schemes have delivered positive returns, ranging from a high of 19.27 per cent by Quant Flexi Cap Fund to a low of 9.66 per cent by UTI Flexi Cap Fund. A similar trend is visible across other categories. The average return across all 13 small-cap schemes stands at 17.71 per cent.

Advertisement

Market experts, however, argue that such phases are not unusual in equity investing. SIPs are designed to benefit from market volatility over longer horizons as investors accumulate more units at lower valuations.

Still, the current phase serves as a reminder that SIPs are not immune to market cycles. While disciplined investing remains one of the most effective wealth creation strategies, investor expectations need to be aligned with the realities of equity markets, where temporary periods of negative returns are an inherent part of the journey.

Focus On Global Diversification

There’s another noticeable trend that we should be aware of. The current market environment has turned the focus on diversification through global investing. Once limited to sophisticated investors, it has now entered mainstream retail portfolios.

While some international markets, particularly the US technology-heavy indices, continue to show resilience, many investors are wondering whether they should move a part of their money overseas.

Advertisement

Reality Check: The conversation around global diversification deserves a balanced approach rather than blind enthusiasm. Overseas investing can certainly help investors to diversify portfolios across geographies and reduce concentration risk. Besides, exposure to sectors underrepresented in India, such as global technology, can add value.

However, chasing foreign markets purely because recent domestic returns have moderated can become another form of performance chasing behaviour, which can prove detrimental at times.

Typically, when domestic markets underperform, overseas investing suddenly becomes fashionable. Consequently, the narrative fades when the Indian market outperforms its global counterparts.

Conclusion

Successful investing is rarely built around narratives, driven by short-term market movements. The true test of an investor is not during bull markets when optimism is at its peak. It is during uncertain phases, when headlines are negative, returns are muted, and remaining patient becomes difficult. That is when investment behaviour matters the most.

As we release our latest fund ratings amid this turbulent backdrop, one thing remains clear: cycles will change, narratives will evolve, and markets will continue to fluctuate. But disciplined investing, diversification with purpose, and patience through volatility remain timeless principles. Total monthly SIP inflow of `31,115 crore as of April 2026 is testimony that many investors are maturing. For them, India’s Best Funds list will be valuable to check if their funds got five- or four-star rating. We have taken Morningstar ratings to assess the performances over three time periods. These are not recommendations, but a checklist.

Advertisement

If you want our recommendations for fresh investments, check our OLM 50 list (Page 52), which is a curated basket of funds that have been picked not just on the basis of performance but other metrics such as investment process and fund manager track record.

How We Did It

While Morningstar India rated the funds, we ran the rest of the numbers ourselves. We chose key categories in the equity, hybrid and debt segments.

In India, most individuals invest more in equity-oriented schemes. Therefore, we have included all the equity categories defined by capital markets regulator Securities and Exchange Board of India (Sebi). But we excluded contra and dividend yield categories because the number of schemes in these are very less—three in contra and nine in dividend yield.

Hybrid funds are also becoming popular among retail investors as they help balance out market volatility. We included three categories from hybrid funds, which have the maximum retail participation.

From the debt space, which is largely dominated by institutional investors, we have covered five sub-categories that cover the universe in terms of duration, which is the key to making debt fund investments.

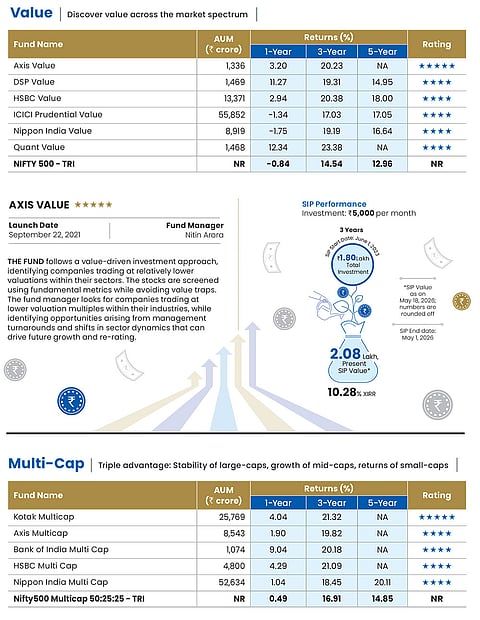

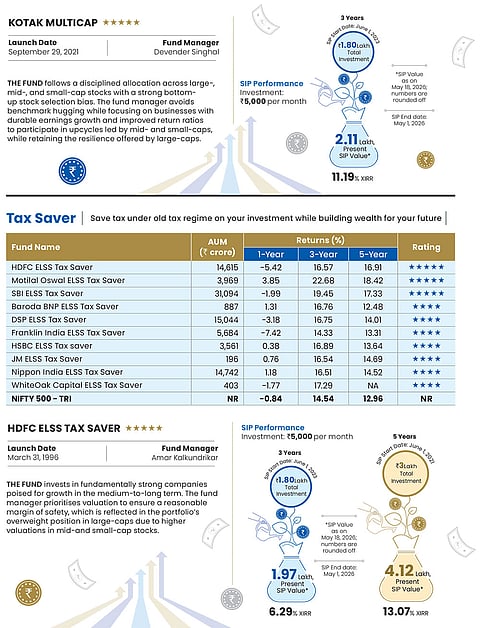

We went a step ahead to analyse Morningstar’s 5-star rated schemes in each category to show their SIP performance over three and five years.

Advertisement

Morningstar Rating Methodology

Outlook Money’s rating partner Morningstar India helped us rate mutual fund schemes with an investment track record of more than three years. The cut-off date for this exercise was March 31, 2026.

The ratings are based on the funds’ risk-adjusted returns. Morningstar uses three steps to calculate Morningstar Risk-Adjusted Return (MRAR). The calculations are done on a monthly basis first and then the results are annualised. Here’s the three-step process.

Total Return: This is the first step in which the monthly total returns for the funds are calculated.

Morningstar Return: At the second step, it calculates or collects monthly total returns for the appropriate risk-free rate. It then adjusts returns for the risk-free rate to get the Morningstar Return.

MRAR: The third step in the selection process is about adjusting the Morningstar Return for risk to get MRAR. Morningstar Risk is then calculated as the difference between Morningstar Return and MRAR. On the basis of these scores, Morningstar India then assigns the star ratings. Morningstar ranks all mutual funds in a category using MRAR, and the funds with the highest scores get the most stars.

Advertisement

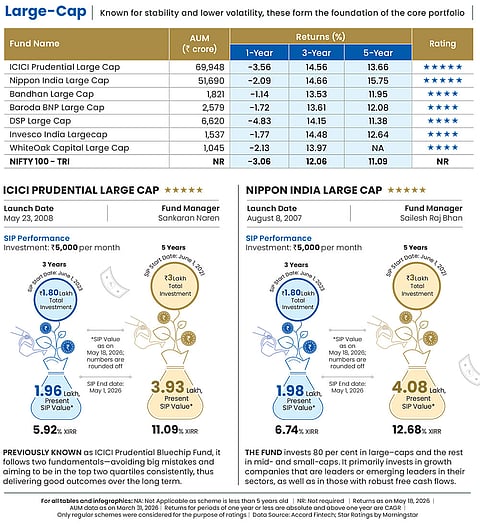

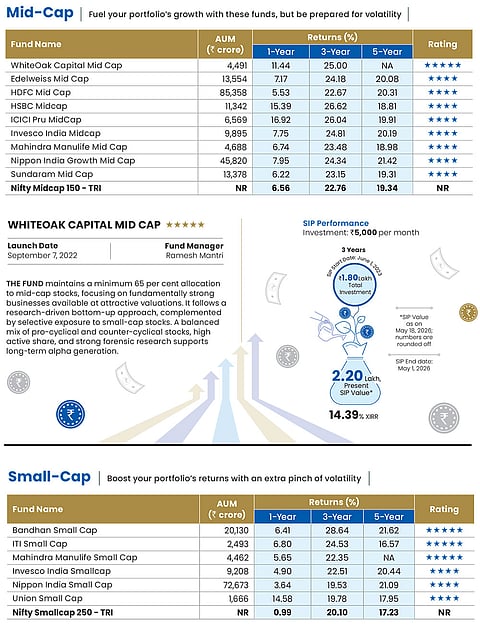

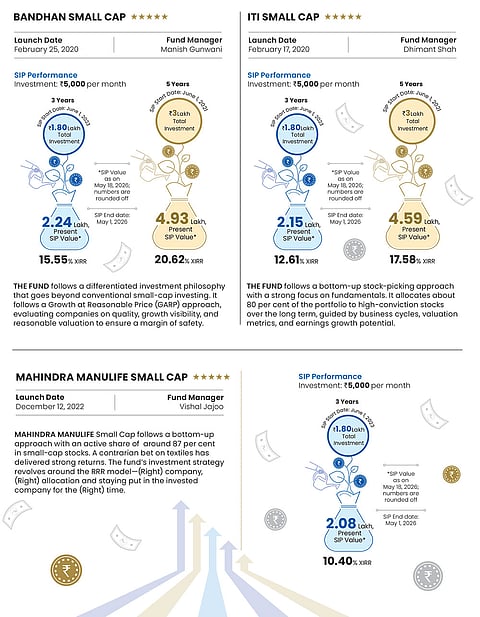

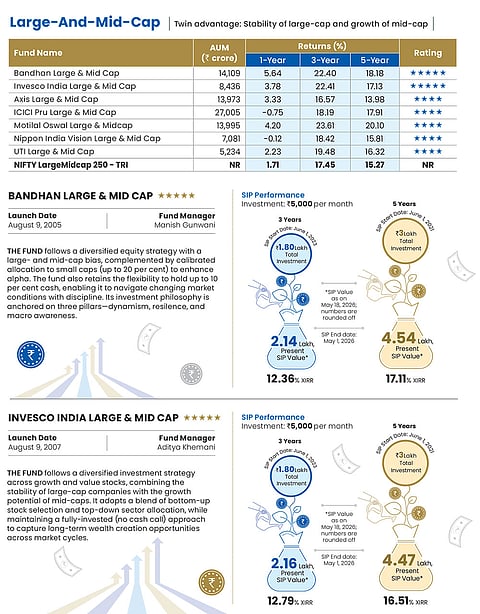

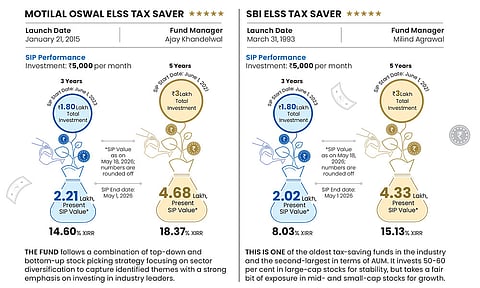

EQUITY

Large-cap funds, regarded as a safe harbour during volatile market conditions, bore the brunt of the recent market correction starting 2025. Heavyweights in banking, IT and financial services dragged down fund performance.

However, strong domestic inflows in mid- and small-cap segments, which saw the highest inflow from domestic investors, helped cushion volatility.

Flexi-cap funds, despite their mandate to dynamically allocate across market capitalisations, were not spared either. Many schemes witnessed sharper declines, especially those that chose to remain in the large-cap space.

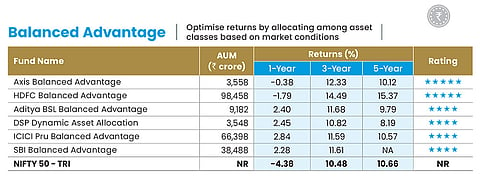

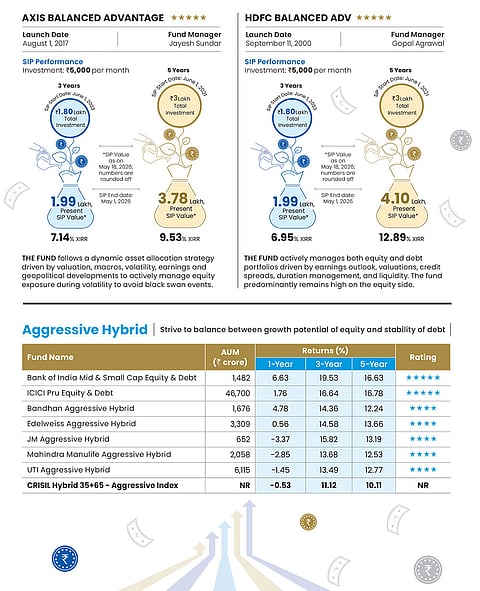

HYBRID

Balanced advantage funds (BAFs) which were dynamic enough to shift from equity to debt contained the downside risk, while those with higher equity exposure suffered in FY26. ICICI Pru BAF, which had lower equity allocation, beat the Nifty 50, giving 2.84 per cent, while HDFC Balanced Advantage delivered -1.79 per cent. In the aggressive hybrid category, more than half of equity- oriented hybrid funds beat the CRISIL Hybrid 35+65 – Aggressive index. This category saw divergence in return of around 8 per cent between the best and the worst performing funds.

Advertisement

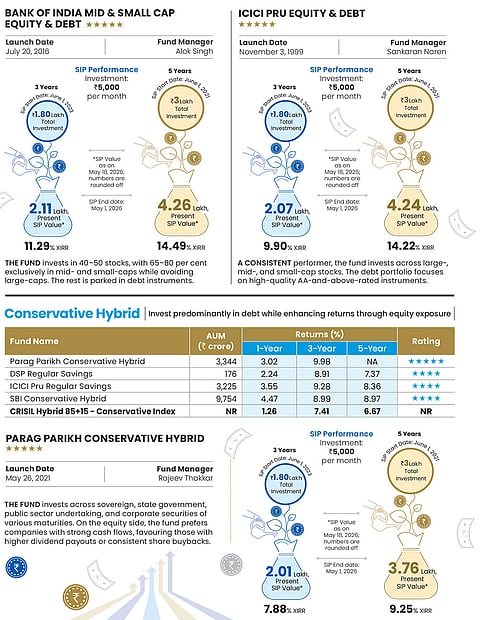

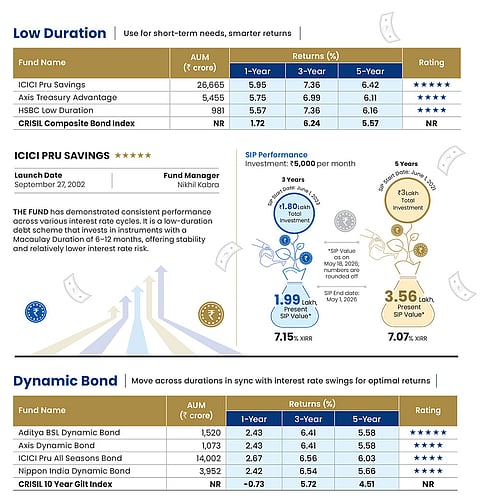

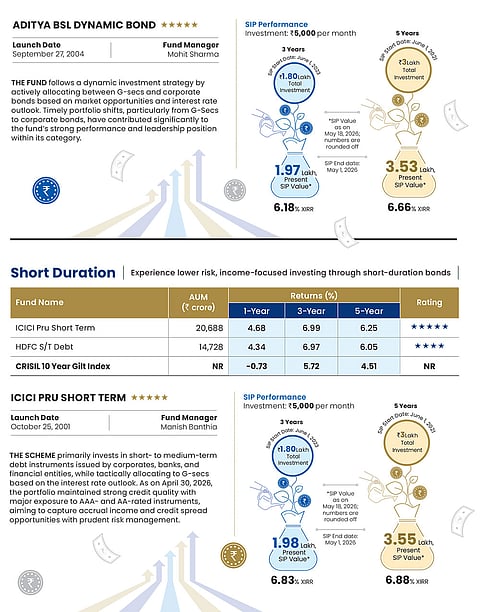

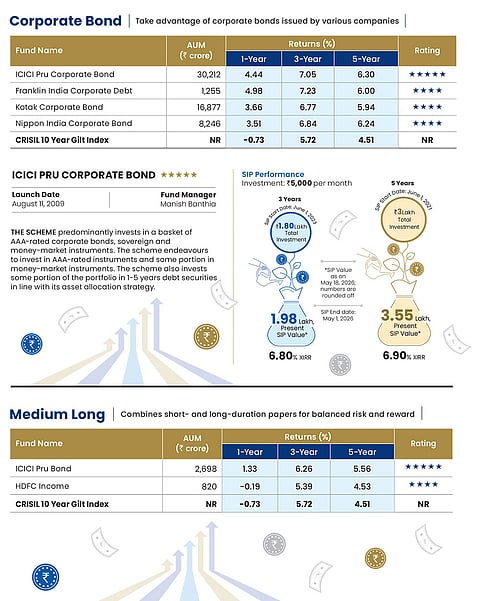

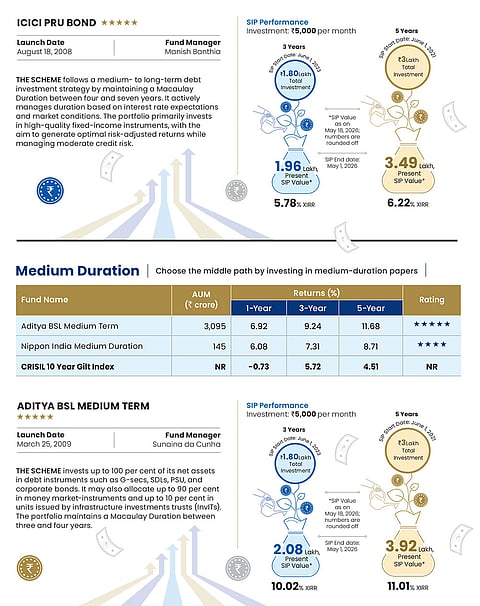

DEBT

Experts believe that debt markets will likely remain range-bound in the near term, with the benchmark 10-year government bond yield moving in the 6.9-7.1 per cent band. For investors, the current environment favours a cautious strategy, with short-duration G-secs and high-quality corporate bonds continuing to offer stability. SDLs are also emerging as attractive options due to their higher spreads. Fund managers advise caution in lower-rated credits and long-duration bonds until there is greater clarity on inflation, interest rates and rupee stability. Dynamic bond funds could help navigate rate cycles better.

Show comments

Published At:

Tags