Until December 2024, information technology (IT) stocks were the undisputed darlings of D-Street, backed by predictable earnings, dollar tailwinds and strong global demand. IT stocks also saw a super rally during Covid-19 as lockdowns forced businesses and people to shift online, and digital adoption accelerated at an unprecedented pace. Companies across sectors rushed to build digital infrastructure, creating the perception that IT companies were entering a multi-year growth cycle. So, investors also flocked towards IT stocks.

Is It The Right Time To Buy IT Stocks?

The IT sector has buckled under the pressure of AI disruption and global uncertainty, with stocks falling 35-40 per cent. Does this correction present a buying opportunity, or is there more pain ahead?

Advertisement

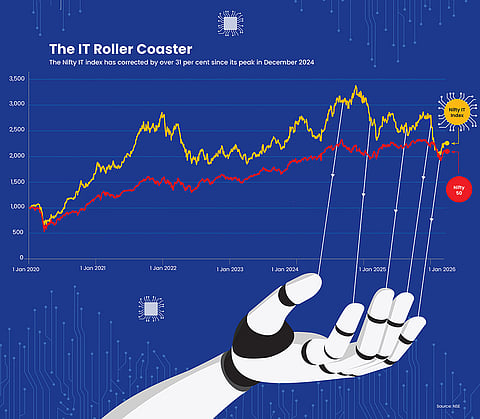

The Nifty IT Index, which was at 11,865 on March 24, 2020, the day the lockdown was imposed, surged more than threefold to around 39,000 within two years, as on January 3, 2022. The Russia-Ukraine war made IT stocks stumble briefly, but they were back in action soon, with the Nifty IT index reaching its lifetime high of 45,995 on December 13, 2024.

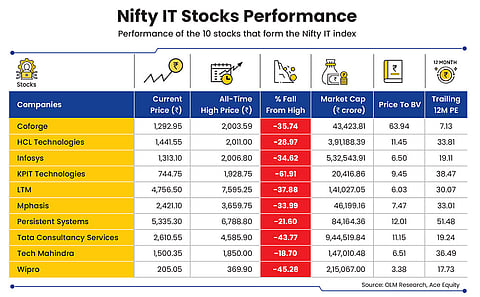

Roughly a year and four months later, the Nifty IT Index has fallen more than 31 per cent, as on April 21, 2026 from the all-time high it achieved in December 2024 (see The IT Roller Coaster). Some of the big names like TCS, Infosys, and Wipro are down by over 35 per cent from their peak. The sector has seen an absolute correction of 20 per cent in the last four months.

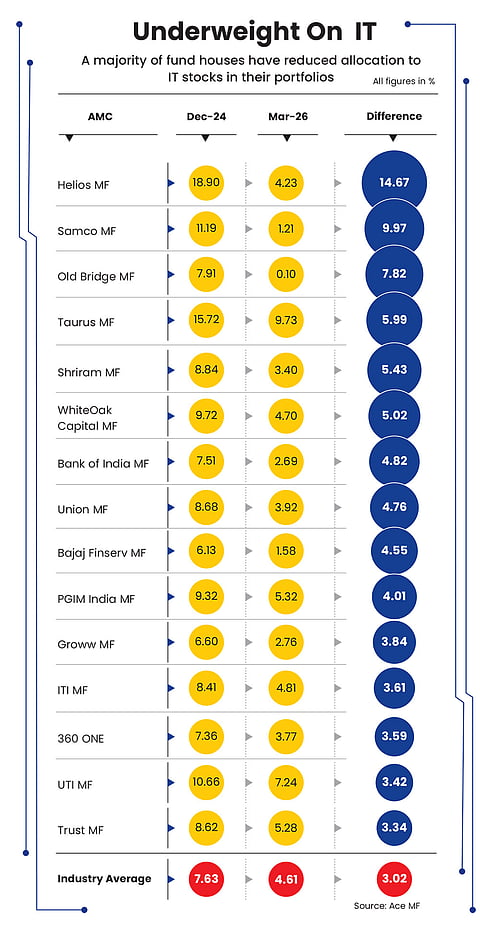

Over the years, fund managers have also drawn down and reduced their IT exposure by almost half (see Underweight On IT). “We have an underweight call on the IT sector, especially on traditional IT services companies. These are likely to be impacted by artificial intelligence (AI)-led disruption, geopolitical conflicts and more insourcing especially in the West,” says Vivek Sharma, senior fund manager, PGIM India Mutual Fund. The fund house has reduced its exposure in IT stocks from 9.32 per cent in December 2024 to 5.32 per cent in March 2026.

Advertisement

So, how does one make sense of the IT index movement? Is it just a cyclical slowdown or a structural shift?

What’s Behind This Fall?

Between December 2024 and mid-April 2026, the world moved on. The Trump tariff game dominated most of 2025, creating upheaval, only to be followed by the ongoing conflict in West Asia that has shaken oil supplies and major economies. Growth has slowed and deal pipelines have become uncertain. Besides, the emergence of technologies like AI, which gained pace over 2025, has changed industry dynamics faster than expected and left a deep mark.

Geopolitical Uncertainty: Experts say one of the reasons for the slowdown in demand for IT services is the elongated period of global uncertainties, including Trump tariffs, West Asia crisis and the deteriorating interest rates outlook.

The Indian IT industry derives over 75 per cent of its revenue from the US and Europe. This heavy dependence makes the sector highly sensitive to global economic conditions.

Advertisement

Global demand has slowed as clients in the US and Europe cut discretionary tech spending amid economic uncertainty. According to companies’ guidance, deal pipelines are healthy, but conversions are delayed, impacting near-term revenue visibility.

There is concern that automation due to rise of generative AI could reduce the need for traditional IT services in areas like coding, testing and maintenance

AI Disruption: The rise of generative AI is both an opportunity and a threat. While companies are investing in AI capabilities, there is concern that automation could reduce the need for traditional IT services, especially in areas like coding, testing, and maintenance. Says Viraj Kulkarni, vice president-equity, Bandhan Mutual Fund: “The advent of any new technology creates uncertainty regarding business models, growth and cash flows of incumbents. The same is happening in the tech space across the board from IT services to SAAS to cybersecurity.”

Investors have seen several such technology cycles in the past 30 years, from the dot com phase in 2000s (popularly known as Y2K, a computer bug that arose because many older systems stored years using just two digits) to the rise of digital and cloud services in 2015 to AI now.

Advertisement

Says Kulkarni: “There’s little doubt that AI has the potential to be among the most disruptive of these tech changes. Investors like certainty and hence, higher the certainty, higher the multiples and vice-versa. With every new and better AI model that is released, the uncertainty levels increase and valuations drop. The correction in IT services now is pure valuation derating with no impact on earnings and cash flows yet.”

Vaibhav Dusad, senior fund manager, ICICI Prudential AMC, says, “This compression in valuation has been led by the rise in risk of revenue and earnings deflation caused by the rise of AI models.”

Moreover, higher capex towards new technology has put pressure on traditional IT companies. “Over the last few years, the US capex growth has been dominated by AI (tech-related hardware, such as servers, GPUs, chips), while investments in many of the traditional sectors have been stagnant and, in some cases, have even declined,” says Dusad.

Advertisement

There’s also lack of clarity on how to evaluate tech spends given the rapidly evolving AI technology and models. “This combined with excessive competition in a weak demand environment has led to higher deflation in deal renewals which could partly be influenced by rise in AI automation,” adds Dusad.

Will IT Survive The Disruption?

The Indian IT services industry has come a long way from its origins as a labour-arbitrage model. Today, companies derive a large part of their value from consulting, domain expertise, system integration, and managing complex digital ecosystems. “The Indian IT services industry started 30 years ago as a pure labour-arbitrage model, but it has evolved over time. At present, most of the global capability centres (GCCs) and IT services companies provide significant value-add,” says Kulkarni.

Incidentally, coding accounts for only 20-30 per cent of work. The rest is in the form of domain expertise, integration, and orchestration.

Advertisement

So does AI pose a threat? Says Kulkarni: “AI disruption is real, but it is more evolutionary than existential. Large companies adopt new technologies cautiously due to security, compliance, and reliability risks. This gives IT firms time to adapt and embed AI into their offerings and reposition themselves as transformation partners.”

He explains how this works with two examples. First, the launch of electric vehicles (EVs) and the rise of new EV companies resulted in derating of incumbent auto original equipment manufacturers(OEMs). The NSE Auto Index was flat for five years from 2017 to 2022. Over time, existing companies adapted to the new tech, and the auto index has more than doubled since then. The second was the impact of OTT, YouTube and other streaming services. The incumbents haven’t really been able to adapt to the new tech and, as a result, stock prices have languished ever since.

What may, however, work for the IT sector is that, historically, these companies have shown a strong ability to adapt to changing technological and business environments. During the Y2K phase, they capitalised on global demand for system upgrades and built long-term client relationships. The shift to cloud computing was another turning point, where Indian IT companies successfully transitioned from traditional services to cloud migration, infrastructure management and digital transformation.

Advertisement

In the current phase, companies have already started adopting AI. Says C. Vijayakumar, chief executive officer and managing director, HCL Technology: “Our new AI-led service offerings are getting traction in the market, reflected in the annualised advanced AI revenue crossing $620 million in Q4. Our priority in FY27 is to ensure the company is positioned to take advantage of AI opportunities for multi-decade value creation.”

Other companies are also aligning their revenue model towards AI. TCS is integrating AI into its platforms to automate routine coding tasks, while focusing more on high-value services, such as cloud transformation and enterprise consulting. Infosys is leveraging AI to enhance productivity, but continues to rely on human expertise for complex client needs.

What’s Ahead?

The outlook for IT stocks is nuanced. In the near term, growth is expected to remain moderate, with management commentary across companies indicating cautious optimism rather than aggressive expansion.

Advertisement

Says Dusad: “The growth outlook for FY27 is likely to remain soft, making this the fourth straight year of weak demand. We expect most large caps in IT to report low- to mid-single digit dollar growth. We are hopeful for growth to accelerate in FY28 to mid- to high-single digit range.”

This recovery is likely to be driven by enterprises getting AI-ready, which would involve increased investments towards modernising internal IT infrastructure (software, databases, process). “Once the integration of AI into the core architecture fabric is completed, the next stage would be operationalisation of intelligence, driven by the launch of AI native apps and platforms,” says Dusad.

Should You Buy Now?

IT stocks have fallen in the range of 35-40 per cent from their 2024 high. After recent corrections, valuations have become more reasonable, providing a margin of safety for long-term investors. “Risk-reward is definitely favourable as downsides (especially in large-caps) are limited and potential upside is quite reasonable, especially if AI-related fears aren’t as bad,” says Kulkarni.

Advertisement

Still, he advises caution. “Investors will need to monitor this space and reassess the impact of AI from time to time,” he says.

Innovation remains the key differentiator when it comes to picking stocks. Companies that adapt quickly and embrace new technologies will have the potential to survive and thrive. “Certain sub-segments wherein the companies themselves are innovating, having new delivery or service models, or pivoting faster, would be our areas of interest,” says PGIM’s Sharma.

Experts say that long-term investors could consider gradual accumulation, focusing on quality companies with strong deal pipelines and AI capabilities. Selective investing in mid-cap IT stocks may offer higher returns, but involves higher risk. Caution is the key.

kundan@outlookindia.com

Show comments

Published At:

Tags