Most investors spend a lot of time trying to figure out what markets will do next. It is an understandable instinct. But it is also, for most people, the wrong one. Long-term wealth is built less on prediction and more on preparation.

Stop Trying To Beat The Market. Build A Portfolio That Outlasts It.

Sriram Vaidyanathan of Integrated Enterprises explains why asset allocation beats market timing every single time.

Advertisement

The familiar version of investing goes like this. Find the next winning stock. Buy before the rally. Sell before the fall. It is a compelling story, and it celebrates foresight. But for most investors, it proves to be an unreliable foundation. There is an old saying in finance that only fools and liars catch the market top and bottom. Timing the market is wishful thinking, not strategy.

Real strategy starts with asset allocation. That means deliberately spreading capital across equity, debt, gold, cash and other assets, based on your goals, your time horizon and how much risk you can actually live with. This approach rarely makes headlines. But it offers something more valuable than headlines: structure.

Howard Marks of Oaktree Capital put it simply: “You can’t predict. You can prepare.” Markets will always carry uncertainty. But a well-built portfolio does not need certainty to work. It just needs to be designed for a range of outcomes rather than one optimistic scenario.

Advertisement

No single asset class wins in every market phase. Equities drive long-term growth but can fall sharply. Debt provides stability and income when equities struggle. Gold tends to hold its ground during inflation shocks and periods of stress. Cash preserves flexibility. Insurance, particularly term and health cover, protects everything else from being undone by an unexpected event. Together, these assets create a balance that is more durable than any single market call.

At Integrated, we plan investment journeys through our GIP framework: Growth, Income and Protection. It addresses all asset classes and is built to generate returns appropriate to each one. A portfolio structured around GIP and sound asset allocation can absorb volatility because it is designed for different market environments, not just the good ones.

Stock market returns are not linear. They are back-ended, not front-ended. Compounding works only when you give it time and do not interrupt it. That is why time in the market matters more than timing the market.

Advertisement

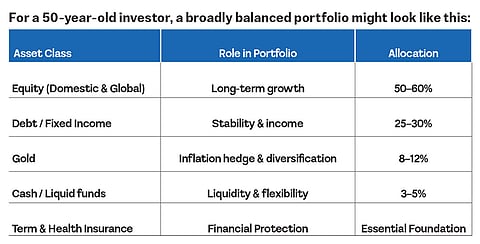

The exact numbers depend on individual goals and risk appetite, but the principle holds across profiles.

The discipline that keeps asset allocation working is rebalancing. When equities rally, trimming brings the portfolio back to its intended structure and locks in gains. When markets fall, adding gradually restores balance. It requires no forecasting. It simply converts volatility from something to fear into information that guides portfolio decisions.

Successful investing rarely comes from repeatedly getting the market right. It comes from avoiding large mistakes, staying invested through cycles and letting compounding do what it does best inside a well-structured portfolio.

Asset allocation is not the most exciting part of investing. But it is the most dependable. Because the real edge in markets is not prediction. It is preparation.

Disclaimer: The Views are Personal and not a part of the Outlook Money Editorial Feature

Show comments

Published At:

Tags