SEBI unbundled fee structure increases direct plan investor costs

Smaller fund houses face higher expense ratios from low scale

Large asset management companies optimize commissions to control costs

Direct Plan Penalty: How Sebi’s New TER Rules Are Leading To Higher Costs For DIY Investors

Data for the 43 schemes in the Flexicap category for the months of March 2026 (pre regulation) and May 2026 (post regulation) showed that instead of lowering costs the new framework has led to an increase in TER.

Summary

Advertisement

The Securities and Exchange Board of India (Sebi) introduced the new Total Expense Ratio (TER) regulation framework in the month of April. The regulator introduced the new framework to increase transparency for mutual fund investors by mandating fund houses to report the costs they were charging the investor.

Under the old framework, mutual funds charged a single, consolidated flat fee which often combined management costs and statutory taxes together. The new framework unbundled the charges by capping the base management fee while allowing external brokerage costs and government taxes to be added to the fee.

However, data sourced from the Association of Mutual Funds in India (Amfi) website showed that the unbundling of transaction fees has caused total expenses to rise for several schemes. The impact is more noticeable in the direct plan category. This in turn disproportionately impacts the ‘DIY investor’ cohort that chose to opt out of distributor networks to save on fees.

Advertisement

Regular and Direct Plan Investors Hit By TER Jump

Data for the 43 schemes in the Flexicap category for the months of March 2026 (pre regulation) and May 2026 (post regulation) showed that instead of lowering costs the new framework has led to an increase in TER. Notably, the increase in TER for the flexicap category is indicative of a similar trend within the broader mutual fund industry as the category represents one of the single largest mutual fund categories in terms of Assets Under Management (AuM).

Unlike sectoral funds or small-cap funds which tend to have erratic trading volumes and unique cost structures, Flexi-Cap funds have a relatively balanced footprint as they invest in Large, Mid, and Small-cap stocks, making them a benchmark category to assess how Sebi’s new TER framework affects mutual fund investors.

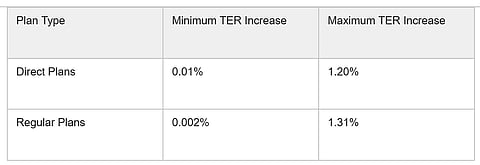

For direct plans the increase in TER ranged between 0.01 per cent to 1.20 per cent. On the other hand, the increase in TER for regular plans ranged between 0.002 per cent and 1.31 per cent. Out of the 43 active schemes analysed between March and May, all regular plans and all direct plans witnessed an increase in TER. Indicating that the cost escalation was industry wide and not limited to a specific fund-house.

Advertisement

Notably, the Wealth Company Flexi Cap Fund’s direct plan witnessed the maximum increase in TER in the two month period of nearly 1.2 per cent while the UTI - Flexi Cap Fund’s direct plan saw the lowest jump in TER of 0.01 per cent.

Investors tend to choose Direct Plans for the relatively lower cost they offer compared to commission-heavy Regular Plans. However, the new framework has squeezed this spread. In March, the average absolute difference between a regular plan and a direct plan sat at 1.14 per cent. By May, the steep rise in Direct Plan TER expenses lowered the absolute average difference down to 1.12 per cent. However for select schemes where the TER increased significantly such as the Wealth Company Flexi Cap Fund the cost advantage of choosing the direct plan over the regular one plummeted from an 83 per cent in March down to 56 per cent in May.

Advertisement

What The Increased TER Means For Investors

The increase in TER is expected to have led to an increase in out of pocket costs for investors. While these TER numbers and jumps may seem huge on paper, it is important to remember that these percentages represent annualised costs, meaning they are charged proportionally over the course of a full year rather than as a single lump-sum hit.

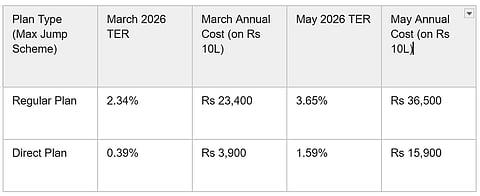

Even so, the compounding effect over twelve months is noticeable. Consider an investor with Rs 10 Lakh invested in the schemes which witnessed the biggest jump in TER between March and May 2026.

Let’s assume an investor had Rs 10 lakh invested in the regular plan of the scheme which witnessed the biggest jump in TER in the flexicap category. In March before the regulation came into effect the average TER was 2.34 per cent indicating an annual fee of Rs 23,400. On the other hand by May as the total average TER increased to 3.65 per cent, it would have led to an annual cost of Rs 36,500.

Advertisement

For direct plan investors in the same scheme the average TER for March was 0.39 per cent leading to an annual fee of Rs 3,900 on an investment of Rs 10 lakh. However, as the TER increased in May to 1.59 per cent, the annual cost would have gone up to Rs 15,900.

Why Direct Plans Face Higher Relative Friction

Prior to the introduction of the new rules, mutual fund houses operated under a more inclusive cap. Components of the cost such as operational taxes, brokerage commissions, and statutory fees were bundled together within a flat expense ratio. However, the new guidelines altered this by lowering the "Base Expense Ratio" (BER) while allowing other non discretionary costs (such as brokerage commissions, Securities Transaction Tax (STT), Stamp Duty, and Goods and Services Tax (GST)) to be added on top of that base. These costs tend to fluctuate based on the fund’s buying and selling activity and fund houses pass them along to the investor.

Advertisement

Manasvi Garg, a Sebi-Registered Investment Advisor (Sebi RIA), CFA charterholder, and the founder and CEO of Moneyvesta Wealth Management to Outlook Money that the transition from a consolidated structure to an explicit unbundled breakdown has naturally driven up the final reported expense ratio figures.

"The rise is mainly due to cost unbundling. Under Sebi’s revised structure, the investor’s total cost is now shown as: TER = BER + Brokerage Cost + Transaction Cost + Statutory Levies (such as GST). Here, BER covers the core scheme expenses, while brokerage, transaction costs, and statutory levies are shown separately. So earlier, some of these costs were more effectively bundled into one overall expense figure; now they are being disclosed more clearly, which makes the total reported TER look higher. SEBI also reduced the BER cap only modestly, so the cut in the base fee was not enough to fully absorb the extra items now being added separately," Garg said.

Advertisement

Bigger Schemes Houses Smaller TERs

The data routed from Amfi showed that schemes which have greater AuMs were able to keep the TER low compared to smaller ones. Schemes like the Parag Parikh Flexi Cap Fund saw the regular plan witnessing an uptick of 0.002 per cent, Kotak Flexicap Fund’s regular plan also witnessed a 0.01 per cent increase. On the other hand smaller schemes like TRUSTMF saw the TER rise by 0.84 per cent for the regular plan and 0.93 per cent for the direct plan

Garg explained that smaller schemes lack the necessary scale to effectively dilute their administrative and compliance overheads across their portfolio.

"Smaller fund houses are affected more because they have a smaller asset base over which to spread fixed costs. Their BER includes scheme-level operating and compliance expenses, such as administration, reporting, and distribution-related costs. When the same cost structure is spread over a smaller AUM base, it takes up a larger share of assets and therefore pushes TER up more sharply. The regulation is the same for everyone, but the impact is not: smaller AMCs have less scale to absorb the costs, so the percentage increase in TER is much higher," Garg said.

Advertisement

Conversely, Garg highlighted that larger asset management companies with larger schemes are managing the new landscape by optimising their operational capabilities and passing the primary financial burden onto their distribution networks.

"Major fund houses keep TERs in check because they can spread fixed costs over a much larger AUM base and absorb the new framework more easily through commission optimization and operating efficiency. In HDFC AMC’s Q4 FY26 call, management said the new BER regime is still at an early stage, estimated the gross impact on the existing book at about 3–4 bps, and said it plans to largely offset this through commission-structure optimisation and prudent management of direct and indirect costs, Nippon AMC gave a similar message in its Q4 FY26 commentary,” Garg said.

Garg added that the TER change is an adjustment phase for AMCs, not a severe earnings shock at this stage.

“HDFC’s message suggests the impact can be absorbed through commission and cost management, while Nippon’s message shows the industry is likely to pass through much of the burden to distributors first, with the fuller effect to be seen over the coming quarters," Garg said.

Advertisement

Despite the rise in TER, investors must understand that this is not a failure of regulatory intent as Sebi’s new framework achieved its core goal of enhancing transparency and disclosing where every single rupee is going. It is likely that the market is currently experiencing a transitional phase as it adjusts to the new TER framework.

Show comments

Published At: