When our grandparents and their grandparents spoke of wealth, they never talked about mutual funds or initial public offerings (IPOs). Their definition of wealth was rooted in two tangible things: real estate and gold. For generations, these assets were the bedrock of financial security in India.

Gold vs Real Estate: What You Should Know

Both gold and real estate have long been preferred investment choices for Indians. They hold sentimental value, too. We compare the two and assess if one or both assets can complete your portfolio

Advertisement

Gold, even in the form of jewellery, has been and still is seen as an emergency backup that can be pawned for medical expenses or major goals like children’s education and wedding. On the other hand, buying a home, for most families, is the largest investment they ever make, and it carries both financial and emotional weight.

Gold is back in vogue, not just as a hedge against inflation but as a global safe haven for a world rattled by geopolitical tensions. Central banks are piling it, a clear signal that even the biggest players see its value. Real estate, after years of stagnant and in some cases negative returns, is also booming now. The money though is mostly flowing into high-end properties, squeezing the affordable housing space.

Both assets have their merits and demerits. But can they form the entirety of your portfolio?

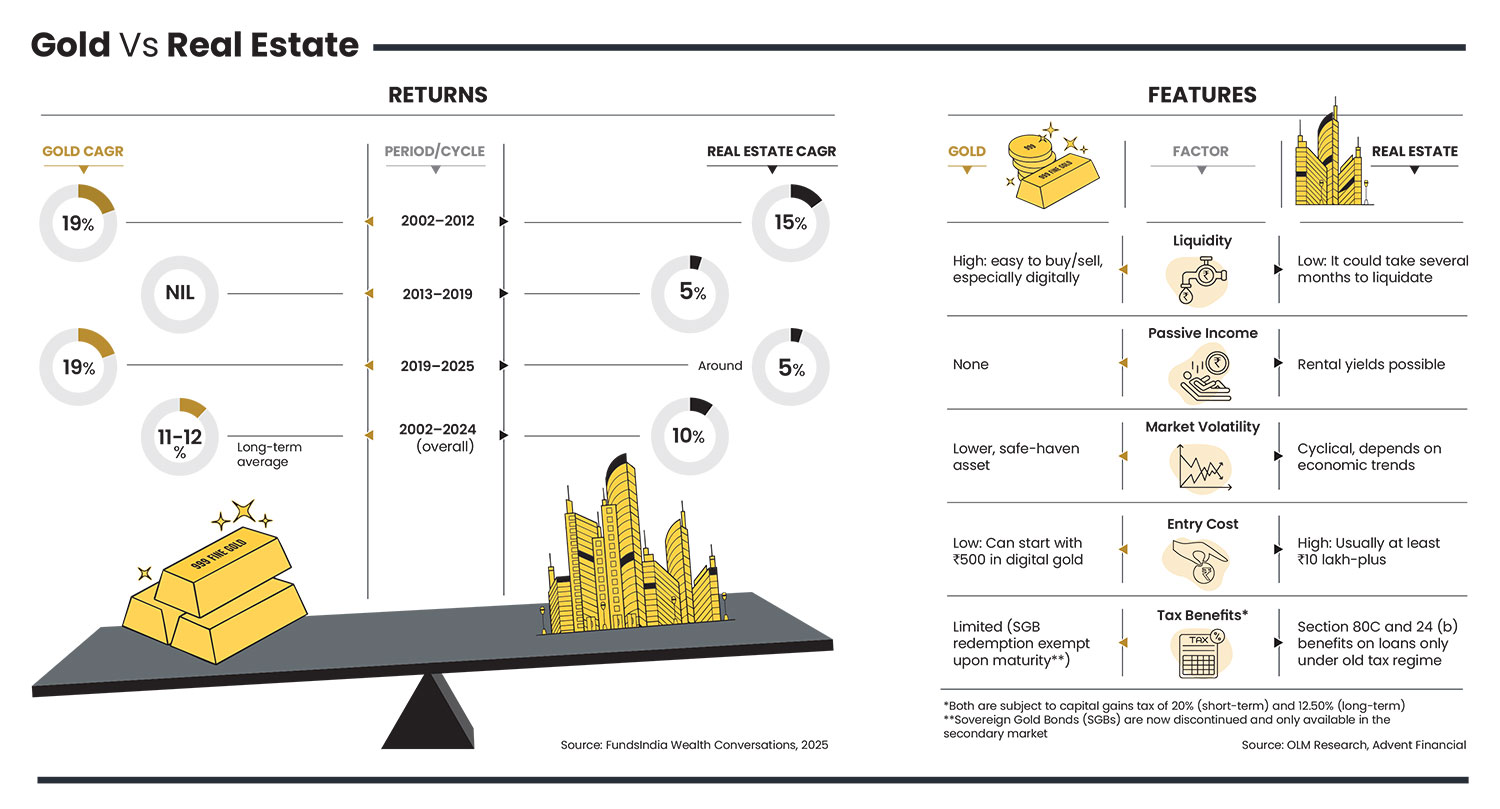

What Gold Offers

Whether as jewellery, coins, or financial instruments, gold remains a store of value when trust in other assets falters. Typically, when markets slide, or the rupee weakens against the dollar, gold climbs. It is no coincidence that the Reserve Bank of India (RBI) expanded its gold reserves from 695 tonnes in FY21 to nearly 880 tonnes by FY25. Central banks worldwide are signalling confidence in gold as a reserve asset.

Advertisement

Recently it has dazzled investors. At the end of 2024, 24K gold was trading at Rs 7,718 per 10 grams. Gold had rallied to its all-time high during the first half of September, 2025 registering a year-to-date (YTD) gain of 44 per cent reaching Rs 1,06,863 per 10 grams, according to data from the World Gold Council.

However, gold’s returns are entirely dependent on price appreciation, which in turn hinges on global demand, US interest rates, and geopolitical risks. For every phase of stellar growth, gold has endured long stretches of stagnation too.

Says Rahul Agarwal, a Securities and Exchange Board of India-registered advisor (Sebi RIA) and founder of Advent Financial, a financial planning firm: “Investors should keep in mind that gold is almost as volatile as equity. Considering gold is at all-time highs even on an inflation-adjusted basis, one should be mindful and not extrapolate past returns into the future. In fact, one should be prepared to withstand volatility, price correction, and prolonged periods of subdued performance.”

Advertisement

What Real Estate Offers

The real estate sector is seeing a strong run. According to the India Brand Equity Foundation (IBEF), India’s real estate market is expected to touch $1 trillion by 2030. Current projections by Grant Thornton suggest a compounded annual growth rate (CAGR) of 9.20 per cent between 2023 and 2028, supported by urbanisation, infrastructure spending, and demand from younger demographics. In 2025, home prices in major markets saw a CAGR of 13-15 per cent during 2023-25, though this is expected to cool to 3-5 per cent in 2026.

Yet the sector is not without cracks, with new luxury and premium offerings becoming out of reach for the common man. Housing sales in Q2 2025 slipped below 100,000 units across India’s top nine cities, a 19 per cent drop year-on-year (y-o-y), according to PropEquity. Mumbai and Thane saw the steepest falls at 34 per cent. Oversupply in certain metros, liquidity constraints, and regulatory hurdles continue to challenge the market.

Advertisement

Real estate offers the potential of regular rental income, and financing it provides tax benefits under the old tax regime, but it also carries developer-related risks of delay and fraud, possibilities of legal tangles and, most importantly, is illiquid.

Says Agarwal: “With Real Estate (Regulation and Development) Act, 2016, (Rera), a lot of developer-related risks have been addressed. But real estate is illiquid, and the actual price realised while selling a property is typically lower than the market value by 5-10 per cent.”

Gold Vs Real Estate

Returns: While both asset classes have given good returns cyclically, gold has outpaced property in recent years (see Returns: Gold vs Real Estate). Typically, returns from real estate are more tied to location, development, and the broader infrastructure.

Rental yield, which is the annual rental income expressed as a percentage of the property’s market value, is another form of return.

In 2024, Bengaluru reported the highest average rental yield among all major cities at 6 per cent, followed by Mumbai at 4.15 per cent, and Gurugram at 4.10 per cent, according to a research by Anarock.

Advertisement

Kolkata registered a rise in rental yield from pre-Covid levels, up from 3.30 per cent to 3.80 per cent. Delhi recorded a rental yield of 2.90 per cent, and Chennai and Hyderabad 3.10 and 3.20 per cent, respectively.

The report noted that rental yields in developing nations across the world can be as high as 6-8 per cent, so Indian yields are relatively low. This difference becomes crucial when rental yields are accounted for return on investment (ROI) in real estate.

Gold usually responds to macroeconomic shocks and can be volatile. It has suffered drawdowns of more than 20 per cent in the past, so you need to be ready for that.

Liquidity: Real estate is illiquid. When you need money, there’s no guarantee you will get the right price or the right buyer. Selling property can also take months, and the sale price is typically lower than expected.

Gold is broadly liquid though there are some complications depending on the type of gold you are holding. For instance, gold exchange-traded funds (ETFs) can be bought and sold on real time through the stock market. It is the same with gold mutual funds. However, challenges may arise in case of physical gold. Many jewellery shops may not have a buyback policy. Also, jewellery, bars or biscuits bought from one jeweller, if sold at another, typically involves verification and purity tests. Even banks do not buy back gold they sell.

Advertisement

Risks: Holding physical gold comes with storage and theft risks. Bank lockers are an option, but they come for a fee. Besides, banks do not guarantee the contents stored in a locker in cases of theft, natural disaster or other circumstances. Including gold under home insurance may work, but that, too, involves a process, and terms and conditions.

Says Abhijit Chokshi, Sebi RIA and founder of Stockifi, a financial advisory firm: “Indians love physical gold for weddings, gifting, and emotional value, but it comes with purity risks, storage costs, and low resale. Digital options like ETFs are far superior for salaried investors.”

In real estate, besides the liquidity risk, there is the risk of falling into a legal tangle. Verifications, title clarity, risk of fraud, and delay in possession have to be considered, among others.

Adds Chokshi: “Both gold and property carry risks. Gold is highly liquid, but its price swings with the dollar, global interest rates, and RBI’s policy. It generates no income. Real estate offers rental yield, but involves high entry costs, stamp duty, goods and services tax (GST), legal/title verification, and recurring maintenance. It is also illiquid. Selling can take months and prices may stagnate, especially in Tier-2/3 cities. Many retail investors underestimate tax on capital gains and property registration hassles.”

Advertisement

Costs: Besides the high entry costs and maintenance, there is also the interest factor if you take a home loan, and capital gains tax at the time of sale.

Buying physical gold involves making charges, which are not considered at the time of selling. In gold funds, there is an expense ratio. At the time of selling, only the price and weight of gold is considered.

Inflation Hedging: Both gold and real estate are often called inflation hedges, but the way they behave is different. Gold reacts directly to high inflation or rupee depreciation. Prices surge quickly in such periods, making it an immediate shield. Families also rely on it during crises, pledging or selling gold to cover other expenses.

Real estate behaves unevenly. In prime metros, property can keep pace with or beat inflation. But rural land or flats in oversupplied Tier-2 and Tier-3 cities often lag. Inflation-linked rental increases exist, but they are capped and rarely match double-digit consumer inflation.

Advertisement

Says Chokshi: “In India, gold has historically protected households against inflation better than real estate. During high inflation or rupee depreciation, gold prices rise, quickly making it a direct hedge. Real estate, however, works only in certain micro-markets like top-tier metros where demand is strong. Rural land or flats in oversupplied cities often lag behind inflation.”

What Should You Do?

Over-allocation to either asset can hurt. Investors who parked too much in real estate during the slowdown of the last decade missed out on equity market gains. Similarly, those betting heavily on gold during its stagnant years earned less than even a simple Public Provident Fund (PPF). During the period between 2013 and 2018, the average annual return from gold in India was around 3 per cent, while PPF offered a steady interest rate at 8.70 per cent till 2016 and then between 7.60 per cent and 8 per cent through 2018.

Advertisement

Agarwal says: “Notwithstanding the relative benefits and drawbacks of gold and real estate, it is always prudent to follow a diversified portfolio approach which has allocation not just to gold and/or real estate, but other asset classes, such as debt and equity. The allocation to each asset class can be decided based on a careful evaluation of the risk-return trade-offs of each and how it all comes together to deliver on your target objective.”

When it comes to choosing between gold and real estate, the decision cannot be binary. An investor’s time horizon, liquidity needs, and risk appetite should determine allocation. Gold suits those seeking liquidity and protection in uncertain times. Real estate favours those with long-term horizons and capacity to handle illiquidity.

Says Abhishek Kumar, a Sebi RIA: “There is no one-size-fits-all approach. Your decision should be based on risk tolerance, investment horizon, and financial situation. Gold can be best for short-term security and liquidity. Real estate works for long-term wealth creation.”

Advertisement

Kumar also advocates balance: “Diversifying your investments can help balance risk and return. A mix of gold and real estate allows investors to capitalise on the stability of gold and the growth potential of real estate.”

For most households, investing 5-10 per cent in gold and owning a house in which you can live is a rational path.

What To Consider Before Investing

Real Estate

Illiquid, selling can take months, often below the market value

Huge entry cost, down payment, stamp duty, GST, brokerage and so on

Rental yields in India are low (2-4 per cent in many cities)

Prices can stagnate, especially in oversupplied Tier-2 or Tier-3 cities

Legal/title risks, fraud, regulatory hurdles, and paperwork nightmares are possible

Gold

Highly volatile, swings with USD, Federal Reserve rates, global tension

Long stretches of dead returns (can stagnate for years)

If you hold physical gold, you will face storage hassles and risk of theft

Selling physical gold is costly as jewellers deduct making charges

Not all places from where you can buy physical gold like banks, buy it back

shivangini@outlookindia.com

Show comments

Published At:

Tags