By now you would have realised that the proceeds from a life insurance policy can go a long way towards stabilising a family's finances. In case of exigencies, the proceeds can help the dependent family cope with immediate expenses and also plan their other financial goals. In families where the deceased may be the primary earner, the loss of that income can be devastating. How will the family repay the home loan? Will there be enough money for the child's college? The answer to all these questions is having the right life insurance policy.

When planned well, life insurance can address the long-term financial needs including income protection for dependents, wealth creation and savings. There are also policies that will address loan repayment security, children's future, retirement corpus and annuities, which are among the many prominent variants of a life insurance policy. Life insurance is able to address all these needs, because it is typically a long term product which has the ability to absorb short-term shocks to deliver what it promises. Life insurance is able to deliver on the promise because it is structured to manage of a life insurance policy. Life insurance is able to address all these needs, because it is typically a long term product which has the ability to absorb short-term shocks to deliver what it promises. Life insurance is able to deliver on the promise because it is structured to manage risk. And by purchasing insurance, you can transfer your personal risk to the insurer, pay a price for the services, and relax.

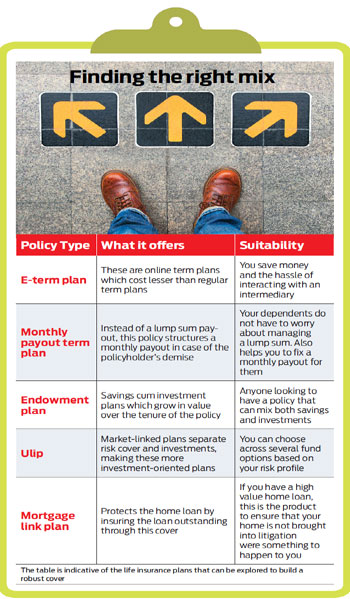

Right selection

Start by identifying what risk you wish to transfer and it will help you identify the policy that will fill that gap. "When one gets married and has kids, insurance requirements go up. A child is dependent on a parent for 20 years; so life insurance requirements go up substantially after the birth of children," explains Suresh Sadagopan, financial planner, Ladder 7 Financial Advisories. While you need to increase the insurance cover on your life, you also need to consider a dedicated child plan which will address your child's future financial needs like education and marriage.

Take for instance Mumbai-based Anjesh Prajapati's case, who bought a child insurance policy to fund his daughter's education. "She is in 12th standard now and the objective was to put money in safe avenues which will be there when she finishes school," he says. What the child plan does is force him to pay an annual premium, which is locked-in in such a manner that he cannot touch it till it is time for maturity. There is also the backup in case Prajapati does not live to see the maturity. Either ways, the policy ensures that education is not compromised.

The structure of child plan disciplines a parent as there needs to be an annual payment of premium. What's more? Premiums paid towards such policies also qualify for tax deductions under Section 80C and the maturity is tax free under Section 10 (10D), as is the case with all life insurance policies.

Retirement corpus

Like child plans, retirement plans from insurers are also targeted towards a financial goal, something that no other financial product offers. Insurers offer you an avenue to accumulate savings, whereby you pay premiums and the money accumulates through the tenure of the plan in an accumulation phase. Once you reach your retirement age, the plan generates a lump sum on retirement, which would generate regular income through an annuity plan.

"Retirement plans instil a sense of discipline that is required in retirement planning. Retirement is a big event in an individual's life and takes care of that from an end-toend perspective with compulsory annuitisation post vesting," says Deepak Mittal, MD and CEO, Edelweiss Tokio Life Insurance. There are retirement plans these days that function like Ulips and offer better returns. Such plans are again useful for people who otherwise do not have the discipline to save and invest regularly towards their future.

Linked to markets

Unit-linked insurance plans were the most abused life insurance plans in the mid 2000s purely for the way they were structured and sold. But viewed dispassionately after regulatory changes, their structure is very much suited to a first time investor in the markets. "They have lower charges compared to term insurance plus mutual fund combination which is what it substitutes. They have drawbacks, but are good for those who lack discipline," feels Sadagopan.

One of the biggest drawbacks with Ulips is that the investment option is available only from the insurer from whom you buy it. So, if the fund scheme is not faring well, you cannot exit it to a fund that fares well, making it restrictive for you. In comparison, mutual funds allow you to shift across mutual fund schemes of different operators. Nevertheless, these serve the purpose of a certain class of people.

The flexibility within Ulips could be used well by policyholders to suit their risk appetite and also use the learning experience of shifting across fund schemes with their other investments. Most insurers offer a wide range of funds based on the investment objectives, risk profile and time horizons. A policyholder can shift across funds without any charges a couple of times each year, but that is just on paper as very few policyholders actually get into shifting across fund schemes.

"Majority of Ulips introduced post 2010 now come with a minimum 10 years policy term which gives an opportunity to the consumer to benefit in the long term from equity exposure," feels Kshitij Jain, MD & CEO, Exide Life Insurance. Good or bad, one should not forget that investments in Ulip are risky, which one should know of before getting into them. Moreover, Ulips should not be assessed based on their returns alone as the minimum life insurance cover that is mandated takes care of a basic risk protection.

Income plan

A recent trend among insurers is to provide a monthly payout with term insurance. What it means is that in case of a claim, the payout is not a lump sum, but a monthly sum. This is a huge convenience to the dependents of the policyholder who may otherwise not be tuned to handle the lump sum. "It is a real challenge for families to manage large amount of money when given out as lump sum and thus the basic premise of securing the family financially may get lost," explains Murlidhar of Kotak Life.

Deferred term plans disburse the claim amount in a staggered manner-you can also choose variants that offer fixed monthly payouts or increasing payouts to cover inflation. "This feature provides the required income to the family to ensure all expenses are met and also saves them from the hassle of handling and investing money which they might not be experts in," adds Murlidhar. While one may argue the better realisation from taking a lump sum and managing it on one's own, it is not everyone's cup of tea.

Life insurance policies are now also offering specific chronic disease covers to address heart and cancer related ailments. While the scope of health insurance addresses treatment of these diseases, the life plans are structured to make an outright payment to the policyholder when the incident strikes. So, in case of detection of cancer, the policyholder gets a defined sum. In short, life insurance can help replace income, build wealth, create corpus to meet financial goals and provide peace of mind. Make sure you take the right policy for the right need.