The two-day IDFC FIRST Bank presents Outlook Money 40After40 Retirement Expo opened in Mumbai on February 7, 2025. Speakers highlighted several aspects of retirement planning, including how to deal with investments, how to fight biases, the importance of insurance and lifestyle and mindset changes.

Celebrate Retirement

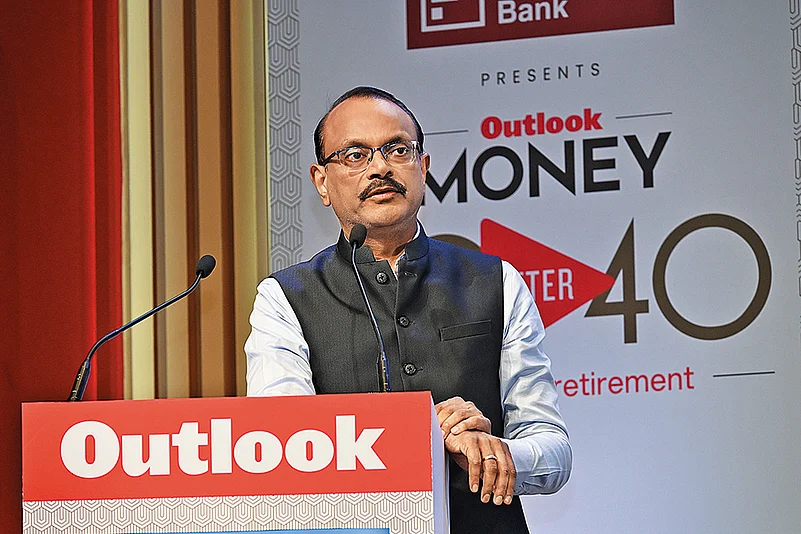

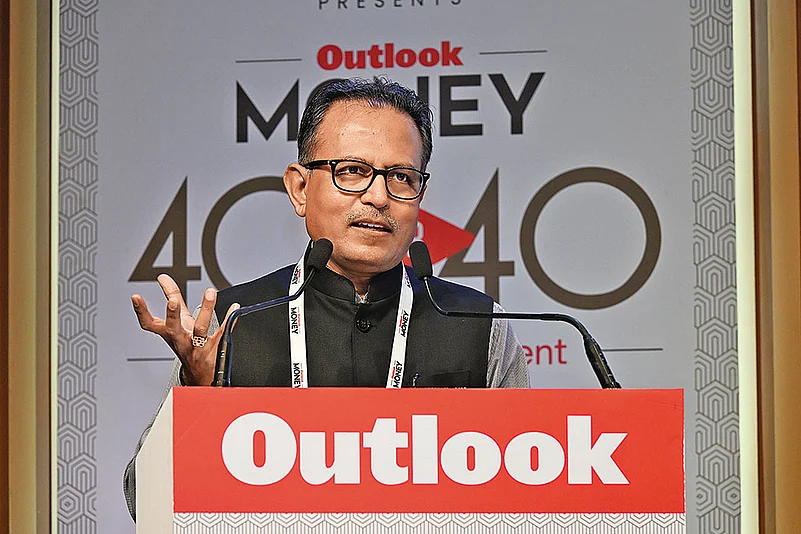

V. Vaidyanathan, managing director (MD) and CEO of IDFC FIRST Bank, said that one should celebrate retirement and see it as a transition to another phase of life. “They should be involved and engaged in some social, or commercial activity or have something to forward to”.

1 August 2026

Get the latest issue of Outlook Money

The fact that 60 per cent of Indians believe funds will not last them more than 5-10 years into retirement, means that “retirement planning is the need of the hour,” he added.

Talking to Sonia Shenoy, business journalist, he said: “One must start early because a lot many think they will start planning when they are older. But then they do not have time for their money to compound.”

He said now there are many schemes into which people can invest, such as Employees’ Provident Fund (EPF), Public Provident Fund (PPF), National Pension System (NPS), and Atal Pension Yojana (APY). They can use government schemes to save for retirement, he said.

Investment Strategy

Samir Arora, founder, group chief investing officer (CIO) and fund manager, Helios Capital, spoke about his investment strategy to find multi-bagger stocks. The key is to eliminate the bad ones, he said.

“It is easier to know what is bad than to know what is good. That is the formula. The end result is you will get multi-baggers over time.”

He said over a long time-frame, equities typically beat fixed income assets, such as bonds or fixed deposits. He also cited a book, Triumph of the Optimists: 101 Years of Global Investment Returns, where the authors took about a 100 years of data on 15-16 countries between 1900 and 2000 and found that over this time period, equities had beaten fixed income by an average of 5-6 per cent per annum.

He added that the Indian equity market in dollar terms has beaten ace investor Warren Buffett’s returns in the last 20 years.

He also cited an example. He said he bought Kotak Mahindra Bank’s shares in 2004 or 2003 and has held them for 25 years. The stock is up over 400 times, which is proof that if “you buy a good company and hold it for the long term, you make lot of money”, adding that in 2003, nobody would have known this.

Devina Mehra of First Global advised investors to diversify their portfolios by including stocks beyond just Indian markets.

“If you look at equities, India is less than 5 per cent of the market cap of the world. There is no reason why 100 or 90 per cent of your assets should be in India,” she said.

She also advised investors to be realistic about stock picking, as a reasonable percentage of their picks may not perform up to expectation.

She added: “Always buy a portfolio of stocks, at least 25-30 stocks. Out of those 25-30 stocks, maybe 5-7 stocks are going to be duds where you will need to get out. Some will give reasonable returns, and if you have picked them well, and your luck also favours you, maybe you will get 2-3 multi-baggers out of that.”

Nilesh Shah, MD, Kotak Mutual Fund, highlighted some of the obstacles investors face in their retirement planning and suggested some key strategies to navigate through market volatility.

One strategy would be to extend the investment horizon, second would be risk appetite measurement, and the third would be asset allocation.

He also advocated a disciplined approach to investing to manage volatility. “Regular contributions create a smooth investment path, regardless of market fluctuations.”

Lastly, he said, investors could be classified into three categories based on their investing habits during a crunch or a difficult market situation. These are aggressive, conservative and average risk takers.

Sankaran Naren, executive director and chief investing officer (CIO), ICICI Prudential AMC, talked about three fundamental principles of investment. These were temperament, journaling, and knowing when to exit.

He cited instances from 2007, 2008, and 2020, when most people sold rather than bought, which reflected on people’s ability to handle temperament. The second aspect, he said, was spending time on research. “By maintaining a record of investment decisions, investors can assess and learn from past actions.”

Lastly, people should know when to exit to protect their money. “When markets have delivered huge returns, the goal should be to protect your money. When markets have suffered losses, the goal should be to make money,” he said.

He said the best equity strategy today is not to put all your money in equity. “Investing entirely in mid-caps and small-caps is extremely risky. What we recommend is asset allocation—investing across equity, debt, and global markets rather than concentrating all funds in one asset class,” he said.

R.K. Jha, MD and CEO, LIC Mutual Fund, shared insights on how one can become a successful investor by following the four Ds of Discipline, Duration, Diversification and Diligence in order to reap the long-term benefit of the power of compounding.

He also emphasised on the importance of staying informed and focusing on the value of asset allocation as well.

Mahendra Kumar Jajoo, CIO, fixed income, Mirae Asset Investment Managers (India), said that for a typical Indian household, debt constitutes about 60 per cent of the overall portfolio as it is seen as a safe way to protect wealth.

When people transition from wealth accumulation to wealth preservation, allocating a significant portion of their portfolio to debt becomes important, he said.

“Once you have created wealth, you start protecting your wealth. That is the stage where debt becomes important for your portfolio,” he said.

Leveraging Artificial Intelligence In Work Life

Ronnie Screwvala, chairperson and co-founder of upGrad, investor and philanthropist, spoke about how the advent of artificial intelligence (AI) is reshaping business.

He advised leaders to adopt a 360-degree vision like a ‘drone’. That way they can be ‘problem spotters’ rather than ‘problem solvers’ and quickly address evolving issues.

“For leadership today, a 360 degree approach is very important. That means you need to be a little bit of a drone which is just hovering above a little bit about everybody else, but has a sharp eye to be able to zoom in to whatever you want to do from time to time,” he said.

He added that employees across levels need to accept the presence of AI. “AI might not displace jobs currently, but it can significantly reduce the workload,” he said.

Behavioural Biases

Ananth Narayan Gopalakrishnan, a whole-time member of the Securities and Exchange Board of India (Sebi), spoke of the behavioural biases among investors. These were fear, greed, overconfidence and overtrading, neglecting asset allocation, influence of finfluencers, following a herd mentality, and underestimating risk.

He said individual investors must take responsibility for their biases, while Sebi, on its part ensures adequate disclosures by promoting financial literacy and responsible investing through investor education and awareness.

At a panel discussion with MF industry leaders, experts spoke about conquering deadly sins of investing.

Fear and Greed: Navneet Munot, managing director and CEO, HDFC Asset Management, emphasised on avoiding emotional reactions driven by greed and fear.

Lust: Kailash Kulkarni, CEO, HSBC Mutual Fund, spoke about the “sin of lust”, which makes long-term investing strategies less appealing. Envy: Rajeev Thakkar, CIO and director, PPFAS Asset Management, said how focusing on others’ perceived successes can lead to poor investment decisions.

Pride: Ganesh Mohan, CEO, Bajaj Finserv Asset Management discussed the “sin of pride”, which can manifest as an unwillingness to admit investment mistakes.

Overconfidence: One shouldn’t rely on past successes as they don’t guarantee future returns.

Sloth: The “sin of sloth” could lead to complete neglect of portfolio.

Wrath: Impulsive reactions triggered by market downturns can lead to poor decisions.

Insurance

Disclose Pre-Existing Illnesses: Tapan Singhel, MD and CEO, Bajaj Allianz General Insurance, spoke about the need to disclose pre-existing diseases before buying health insurance policies to ensure that claims are not rejected.

He said that if someone buys a policy after being diagnosed with a major illness, then the claim will not be honoured. “If someone tells you an insurance company will always pay, regardless of circumstances, do not fall for it. Companies conduct investigations, and fraudulent cases make up only 2-3 per cent of claims. The remaining 96-97 per cent are processed smoothly.”

“If you declare pre-existing conditions, the company may initially exclude them for 3-5 years, but after that, claims will be honoured. However, if you hide history, problems arise,” he said.

Prioritise Life Insurance: Sumit Madan, chief distribution officer, Axis Max Life Insurance called for prioritising term insurance as the first step in financial planning. He said 65 per cent of Indian households have only one breadwinner, which makes term insurance essential.

He added that delaying the purchase of term insurance is one of the most common errors young professionals make.

Retirement Planning

Vishal Kapoor, CEO of Bandhan AMC, said procrastination was a major hurdle to retirement planning and 90 per cent of Indians regret not having started earlier.

“Almost half of us still feel that it will be not our own savings for retirement, but soething else that will get us through,” he said.

He said while deposits and pension schemes are popular, equity mutual funds and stocks are becoming very attractive.

He added: “Retirement portfolios tend to be very conservative. While it will be safe, the challenge with that is post-tax returns, and it will be very difficult for you to beat inflation.”

Deepak Mohanty, chairman of the Pension Fund Regulatory and Development Authority (PFRDA), emphasised on the value of incorporating pension plans into individual savings, as they provide long-term financial security and stability, which is vital in today’s time due to increasing longevity.

He also expressed concerns on how the increased dependency of the older population could exert pressure on the young population.

He described the NPS as a flexible, low-cost, market-driven approach that has revolutionised pension accessibility in India by providing benefits to people in the private sector, gig economy, government employees, and even children through NPS Vatsalya.

At a panel discussion on the role of NPS, experts explored the accessibility, cost-effectiveness, and strategic importance of NPS in a diversified retirement portfolio. They said NPS is a robust tool for retirement planning, but its efficacy depends on how well it’s integrated into one’s broader financial strategy.

Suparna Tandon, CEO of NPS Trust, said NPS accommodates individuals aged 18-70, and with the newly introduced NPS Vatsalya scheme, even parents can open accounts for children.

Krishan Mishra, CEO of FPSB India highlighted the cost-effective nature of NPS, which ranges from 0.005-0.009 per cent, and makes it more affordable than mutual funds.

Kiran Telang, certified financial planner and Sebi-registered investment advisor (Sebi-RIA) said advisors assess individual financial situations, goals and risk appetites, positioning NPS as a viable long-term savings option.

Nikhil Varma, head, bancassurance and wealth management, IDFC FIRST Bank, said retirement planning often takes a backseat in India, as the first priority remains children’s wedding and education. However, neglecting that could be dreadful due to the long-term impact on inflation on finances and increasing longevity.

He said the secret to beat inflation is through the power of compounding. If one starts investing Rs 20,000 a month at age 25, they could amass a huge corpus over time, but if someone starts at 45, they will need to put in three times the amount for the corpus.

He said allocating income wisely is the key to financial independence. “About 40 per cent should be directed towards immediate needs, 30 per cent should go into generating a steady income—through options like the NPS or fixed deposits—and the remaining 30 per cent should be invested for long-term growth,” he said.

Chinmay Dhoble, head of retail liabilities and branch banking, IDFC FIRST Bank spoke how they have made their banking app senior-friendly, by providing tools to make investments and tracking simple.

Early Retirement

Sarthak Ahuja, director of NIAMH Ventures, investment banker, said that early retirement is a new reality and many professionals in their early 40s are considering, which is accelerating the timeline for retirement, forcing individuals to think critically about how their money works for them after 40.

He said they could explore entrepreneurial ventures targeting emerging affluent demographics, especially in smaller cities where access to luxury goods and services remains limited. “A simple business model involves identifying popular fashion brands trending on social media, sourcing products in bulk, and listing them locally. This model has proven successful in various markets,” he said.

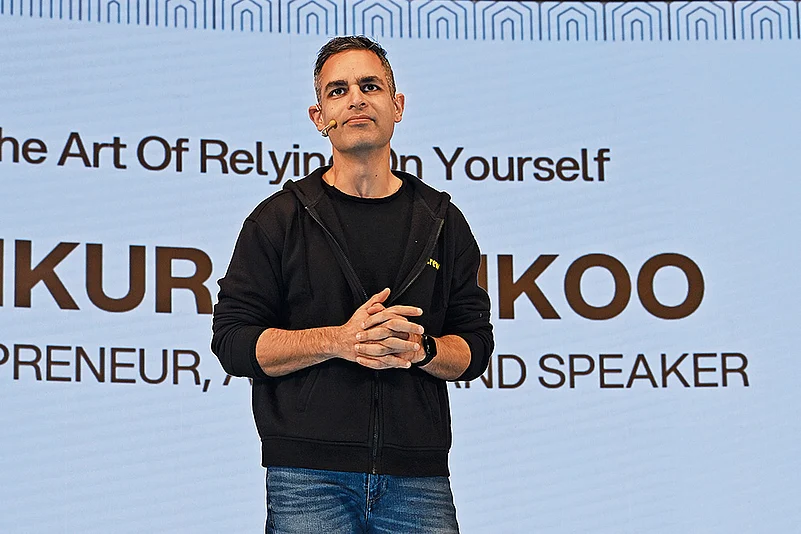

Rely On Yourself

Entrepreneur and author Ankur Warikoo shared his insights on the art of relying on oneself. He said, as a first, people should interact with people who are different from them in order to learn from different and diverse experiences. The second would be to get out of one’s comfort zone because as people start getting intellectually comfortable, they are numbing themselves in the process. The third thing is to learn something new in order to grow.

Monk and motivational speaker Gaur Gopal Das spoke how one should be process-oriented and not goal-oriented in order to manifest goals. He said that life will have its ups and downs and one should try to laugh away the smaller problems.

He gave an analogy of a crane that stands in the water and lets small fish pass through, but catches the big fish. He urged people to treat the smaller problems like the small fish and keep their energy and time reserved for the ‘big fish’.

He said while growth is critical it should not be chased. “One should build a garden to attract the butterflies instead of chasing them”.

He advised people to invest in themselves as they plan their retirement. “We use the best materials for our families and in our social life, but when it comes to crafting our own life, our own peace, we pay no attention to it. As you move towards retirement, you’ll realise that you’re living a life which is made of poor choices and which is why every single day you should invest in yourself,” he said.

Workshops

There were many workshops organised at the event. These included such as Future Ready Financial Strategies To Secure Every Milestone by Girish Ajgaonkar, chief operating officer, Happyness Factory; Power Of Asset Allocation In Wealth Creation by Premal Pipala, EVP & head, learning and development, Bandhan Mutual Fund; How To Prepare Your Portfolio For A Rainy Day by Bhavin Shah, director, Latin Manharlal Group; Avoiding Mental Traps by Peshotan Dastoor, group president & head, sales, UTI Mutual Fund; Fix Your Financial Fitness In 40 Minutes by Vaibhav Shah, head, products, business strategy & international business, Mirae Asset Investment Managers (India); Are You Making The Most Of India’s Safest Savings Plans by Amitabh Singh, chief post master general, Maharashtra circle, India Post; Boodhe Hoke Kya Banoge-Planning For A Worry Free Retirement by Sanjay Pailkar, zonal training manager, west, Aditya Birla Sun Life Insurance; Retirement 2.0 - Planning For A Lifelong Celebration by Tariq Ali, head, retirement and pension,HDFC Life; Where The Money Is: The Sectors You Can’t Afford To Ignore By Shashank Kanodia, CFA, lead analyst, metals & auto, ICICI Direct Research; A New Horizon To Women’s Health by Dr. Rujuta Shrotriya, product lead, Privé Health and GTM Strategy, and Shubham Khurana, manager, brand communication, Bajaj Allianz General Insurance; and Build A Market-Proof Portfolio With The Right Mutual Funds by Ganesh Kamath, chief manager, product development, SBI Mutual Fund.

letters@outlookmoney.com