Every morning when you leave your home, you lock the front door to protect your personal belongings inside. But, is that protection enough for your life's biggest financial asset? In the hurry burry of our daily lives, we tend to overlook some very potent risks that some of our cherished possessions face. The list is long-your gadgets, your car or bike. Worry not, there are insurance policies available to bring all these under the ambit of insurance, and providing you the necessary financial cushion.

The beauty of these policies is that they do not cost you a bomb, which is what you would end up paying were your house was to get impacted by a short circuit, ruining all the gadgets that you are so used to. The non-life insurance domain is such that there is insurance cover for practically every type of risk. There is a personal accident insurance, motor insurance, home insurance, insurance for professionals like doctors and architects and travel insurance, besides health insurance, which is an ocean in itself.

The right choice

Choosing a suitable insurance plan can be an arduous task. To make it easy, start by listing your valuable possessions and evaluate what it will cost you to replace them. If you can afford the replacement on your own, you can ignore insurance, but were you to find the cost of replacement expensive, you would be better off with an insurance policy. For instance, for a small sum, you could have your high-end Smartphone insured than rue over paying a tidy sum to get it repaired or purchase a new one.

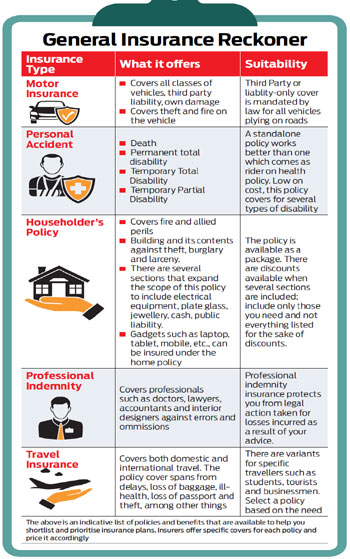

Although insuring your vehicle is a must to ply it on roads as mandated by the Motor Vehicle Act, you also need to insure it for damages due to accidents. "There are additional features in the motor insurance policy which provides for on the spot repair, towing services and zero depreciation, which could come in handy," explains Rajiv Kumar, MD and CEO, Universal Sompo General Insurance. Of course it costs to take these additional covers, but they are worth every rupee when one experiences a claim.

Some covers like engine protection come in handy in case of monsoons or floods and the Return to Invoice (RTI) is an add-on option which covers the gap between the insured declared value and the invoice value of the car. It's an option that will fetch you the entire amount of loss (the on-road price you paid for your car) that you incurred. Typically, an RTI costs around 10 per cent more than the normal policy but considering that a submerged car in rains is a huge loss, this cover acts like the accident safety bag for your finances.

The importance of home insurance crops up every time there is a natural calamity like floods or earthquakes. People who lose their houses and valuables are left to pick up pieces and prepare for the long road to rebuilding. "Majority of households are uninsured against these risks. The lack of insured homes is reflected every time there is a natural calamity in the country," rues G. Srinivasan, CMD, New India Assurance. People spend their savings and even borrow for their dream house, but tend to miss out on securing it with insurance.

Typically, a householder's insurance covers both the structure and contents inside the house. The structure is insured for damage and the contents of the house are covered for damage due to fire and other perils, besides theft. Some policies necessitate listing of all items in the house to be insured, while others are much simpler, having done away with the need to declare each item if the total value is over a particular threshold, say, Rs 5 lakh, making it easier for individuals to calculate the sum insured.

"Normally for a home valued at Rs 50lakh and contents worth Rs 5lakh, the premium would come to Rs 7,000 per year," says Sasikumar Adidamu, CTO, Bajaj Allianz General Insurance. Like any insurance, a home insurance plan also comes with exclusions like misrepresentation, suppression of key information and pre-existing damage to buildings. In case of contents, your policy may not cover loss of money, securities, stamps, bullion, and antiques unless independently insured. Damage to documents like bonds, shares and stock certificates are also excluded.

An international holiday is meant to be rejuvenating, but one does occasionally come across tales of unpleasant experiences. Imagine a scenario where you land up losing your baggage or passport? Interconnecting flights are prone to cancellations. Most importantly, what if you were to fall sick when traveling? The odds that you would have factored in all these exigencies are very remote. The power of travel insurance is felt only on such instances.

There are policies to address every type of traveler's needs-short stay, long stay and even for frequent travelers. The short stay is for a typical vacation taker, while long stay could be for students pursuing courses abroad. The frequent traveler is a business traveler who travels abroad regularly and would rather have a policy taken once to address the travel schedule than take multiple policies.

The claim game

Most people take insurance policies with the hope of not making a claim. After all, who would want to meet with an accident just because they have an accident cover? However, the proof of a policy's promise is experienced when you make a claim. "My car met with an accident with damages all around. I was worried over the expenses I would have to incur. But, the insurance paid for most of the repair costs," beams Kolkata-based Pushpak Banerjee. Banerjee is among those happy policyholders. The repair bill was Rs 1.5lakh and the insurer paid him Rs 1.2lakh, leaving him to fund the balance, which was in-line with what the policy covered.

However, Gurgaon-based Pankaj Adlakha is an unhappy man. His car met with an accident last June where his car's bumper and rear got hit by an auto rickshaw. "The insurer agreed to pay the claim pertaining to the bumper amounting to Rs 4,700, but refused to compensate the damage on the car's rear. The surveyor's contention was that the dents did not confirm that it was hit by an auto," he complains. Yes, there are probably more instances of being unhappy with insurance at the time of claims, but, that is also to do with policyholders not fully understanding the benefits.

"While opting for an insurance cover some people do not even compare the price of similar products available from different insurers. This can be simply done by a bit of research on the websites of different insurers in order to make an informed choice," says Kumar. "In case of complex products where detailed information on the coverage is variable and dynamic, the customers could consider opting the same through agents, brokers or other intermediaries," says Pushan Mahapatra, MD and CEO, SBI General Insurance.

The onus is on the policyholder on fully understanding what policy they are buying. "Online route is beneficial for a well-informed customer, others need to consult agents," stresses Adidamu. It is a good step to take the right policy to mitigate risks, but do so with the right information and understanding, lest you are left high and dry when you need the policy the most-when you experience a claim scenario.