Don’t pledge your gold, use it only as a last resort. We’ve all heard that before. While it’s tough to let go of this obsession of holding on to gold, it’s tougher to overlook the glitter of gold loans these days. According to the RBI, total gold loans saw a compound annual growth rate of 64.9% from 2008 to 2012 and the total outstanding from gold loans rose from Rs.20,000 crore in April 2008 to more than Rs.1,50,000 crore by February 2012. The ease of accessing credit against gold at a relatively lower interest rate has really buoyed this surge. Though it all looks nice and shiny but how does pledging gold for credit stack up against other finance options such as credit cards and personal loans?

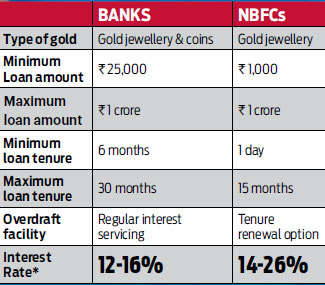

Going for Gold: Bank vs NBFCs

For those looking for emergency funds

How fast can I get a loan? That’s probably the one question that plays on your mind when you are hard-pressed for cash. A personal loan takes at least 3-5 days for processing. On top of that, it would come at a higher interest rate.

Says Anil Rego, CEO and Founder, Right Horizons: “Gold loans are one by Naveen Kumar of the cheaper options compared to a personal loan or credit card. They can be prioritised. Ensure that one has the capacity to repay the loan.” Though credit card is an instant option but the credit limit may fall short of your requirement. If you need cash then the cost would be too high. “In case of credit card cash withdrawals, the charges are too high plus the rate of interest is minimum 36-48 per cent, which can leave a hole in your pocket. So getting a gold loan in few hours makes much more sense.”

For those who don’t have credit cards

If you don’t have a credit card, your emergency funding options are quite limited. Says Rego: “In case of short-term needs, where an individual does not have access to credit cards, the first option that one can consider is friends and relatives. Loan against gold can be considered as the next best.” A gold loan in such cases becomes handy for people without access to formal credit. Alexander George Muthoot, director, Muthoot Group, says: “We provide personal loans secured by gold jewellery primarily to individuals who cannot access formal credit within a reasonable time or to whom credit may not be available at all to meet their personal or business purposes.”

For those who have poor credit history

People who do not have credit cards and are denied personal loan due to poor credit history would find gold loans as a good bet. Rishi Mehra, co-founder, Deal4loans, a loan comparison website, says: “Most companies give you a gold loan even if you have a bad credit history. If you start servicing your gold loan with a good repayment track, it will start improving your credit score.” Since gold, apart from working as a security, has a sentimental value attached to it, it increases the propensity of repayment. A Surendran, head-retail and international business, Federal Bank, says: “Prompt repayment improves the credit history of the borrower.”

For those seeking flexible repayment options

Gold loans provide you the maximum flexibility in terms of how you choose to repay. Says Muthoot: “The maximum tenure for the total repayment of availed credit at Muthoot Finance is 12 months and the same can be done through various means such as EMIs, paying interest per month or part payment.”

So, based on your expected inflow, you can plan your loan’s repayment.

All you got to ensure is that you pay on time

Though as a valuable asset gold helps you get easy access to credit, the shorter tenure of gold loans poses a challenge in the form of quick repayments. Says Rego: “It is advised that while taking a gold loan, one should ensure that the money borrowed is for urgent need. The borrower should make enough provisions to repay the amount of loan or else he may lose his asset (gold).” Auction is often the last resort for the lender. “We send out three notices to our customers after the due date of repayment. First, when the due date for complete payment has been passed. The second is sent after six months, and the third, after a year,” says Muthoot.

What are the choices I have for gold loans?

Gold loan non-banking financial companies (NBFCs), due to their sole focus on asset, provide faster processing and better customer experience but banks with greater public trust as custodians of wealth are best bets with their lower interest rates. Says Surendran: “Our strength includes lower interest rate, higher per gram loan amount, minimum processing, higher security and recovery process.”

If you are in an urgent need for funds and you are ready to pay a relatively higher interest rate, then gold loan NBFCs should work.

But if you want to keep your interest costs low, it is advisable to opt for a gold loan from a commercial bank. Your elders may chide you for using the ‘last resort’, but a gold loan definitely works when you are hardpressed for cash.