Two months ago, in the December 2014 edition of this magazine, we had mentioned that more and more people are moving towards planning their taxes early in the year. Yet, many of us delay our tax planning savings and investment till the last date of the financial year.

With just a little under two months to go before the tax savings clock stops ticking, for the salaried, the accounts department would be breathing down their necks to get all the necessary proof on tax savings. For regular taxpayers though, the entire process of ensuring that their tax plan is on course is not a first-time experience.

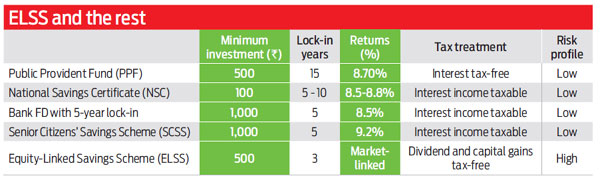

Regular readers of this magazine would know that this year, the mandatory tax saving limit under Section 80C of the Income Tax Act, 1961 has gone up by Rs.50, 000 to Rs.1.5 lakh, which means they can either claim additional sums in their existing tax plan or look for new avenues to deploy the shortfall. No doubt, the usual instruments to save and invest money to save tax exist (See: Save and invest to save tax), but one can look for avenues to dovetail tax savings and any other financial goals.

Regular readers of this magazine would know that this year, the mandatory tax saving limit under Section 80C of the Income Tax Act, 1961 has gone up by Rs.50, 000 to Rs.1.5 lakh, which means they can either claim additional sums in their existing tax plan or look for new avenues to deploy the shortfall. No doubt, the usual instruments to save and invest money to save tax exist (See: Save and invest to save tax), but one can look for avenues to dovetail tax savings and any other financial goals.

Says Swami Saran Sharma, chartered accountant, S S Sharma and Associates: “One should not be waiting till the last moment to exhaust his or her tax saving avenues. But if you are still left with some money to deploy, do so in a way which is in line with your existing financial plans.” This approach is not only convenient; it also ensures that you do not have to take any drastic step in the name of tax saving.

Ways to plot tax plans

The additional window of Rs.50, 000 under Section 80C allows the salaried to extend the benefits of their existing contributions. Says Suresh Sadagopan, founder and financial planner, Ladder7 Financial Advisories, “Most of my clients are already contributing a higher sum towards PF contribution, so this increase in the sum comes as a welcome relief.” The view is the same for those servicing home loans as well, because the payment towards the principal component is something where they can claim additional relief.

The additional window of Rs.50, 000 under Section 80C allows the salaried to extend the benefits of their existing contributions. Says Suresh Sadagopan, founder and financial planner, Ladder7 Financial Advisories, “Most of my clients are already contributing a higher sum towards PF contribution, so this increase in the sum comes as a welcome relief.” The view is the same for those servicing home loans as well, because the payment towards the principal component is something where they can claim additional relief.

But what about a new taxpayer or someone who has to utilise the additional sum which otherwise will attract tax? The way out for them is to consider their tolerance to risk appetite and their risk-taking capacity. “For someone aged 30 years, if the risk-taking capacity exists, he should look at ELSS as an option. But, if he has no risk appetite and is willing to stay locked-in for a long time, PPF (Public Provident Fund) may be a better bet,” says Sadagopan. Basically, the taxpayer should look for investment products with which he can synchronise his existing financial plans rather than attempt anything dramatic.

So, if you are a salaried taxpayer, first find out your contribution towards Employees’ Provident Fund (EPF) and add up all your existing contributions towards tax savings instruments, such as life insurance premiums, ELSS, PPF and any other. If this sum adds up to more than Rs.1.5 lakh, you have already crossed the Section 80C threshold. But, if there is a shortfall, you would know how much more you need to save and invest to max the Section 80C benefits. A simple way—if you are left with money to deploy—would be to evaluate your finances with issues, such as risk appetite, liquidity and your age, among others.

So, if you are young with little financial commitments, using the tax savings in equity-linked products would augur well.

Says Sadagopan, “A youngster would not only save tax from ELSS, he will also get a taste of equities, which can help him in fulfilling his future financial goals.” But, if you are in your mid 30s with financial commitments of a home loan and children’s education to consider, you would be better off claiming the actual sums that you pay towards tax savings.

The common refrain for delays to finish tax planning exercise is more to do with poor planning and allocation of funds. Ideally, one should be done with their tax planning for the financial year as early in the year as possible. There are many benefits to doing this and we shall explore this as we enter the new financial year two months later. With tax structures getting simpler and compliance on the rise, it would be in your best interest to ensure that you are one up on tax planning from next year. It would be worthwhile to have control over how you save and invest to reduce your tax outgo than be dependent on a last minute action which can be detrimental to your finances.