Gold jewelry's IRR is 10.3 per cent, trailing gold's 12.5 per cent CAGR (FY11-1HFY26), due to high, non-recoverable making charges and depreciating precious stones.

Gold prices must rise 25-30 per cent for jewellery owners to simply break even. This makes it an inefficient asset as per the report.

Demand is shifting away from jewellery toward Gold ETFs and other investment instruments, signaling a more financially astute approach by Indian investors.

Worth Its Weight In Gold? Kotak Equities Flags Risk of Low Returns In Gaining Exposure To The Yellow Metal Via Jewellery

New research from Kotak Institutional Equities reveals that gold jewelry delivers significantly lower returns than pure gold assets, with an IRR of 10.3 per cent compared to the metal's 12.5 per cent CAGR

Summary

Advertisement

Gold prices have climbed to fresh highs in 2025. Ahead of the Federal Open Market Committee meeting which is set to commence on December 9, gold prices witnessed an uptick again. While this rise in gold prices may appear as good news for those who own gold or gold based assets, the actual rate of returns might not be the same for all investors. A report by Kotak Institutional Equities titled "Have Indian households been overpaying for their gold?" has shown that despite a rise in gold prices, investors who have exposure to the yellow metal vis-a-vis gold jewellery are likely to get significantly lower returns compared to investors who hold other gold-assets.

Relatively Low IRR For Gold Jewellery

Kotak Institutional Equities mentioned in its report that the returns from jewellery purchases lag far behind the gains of gold itself. The report stated that the Internal Rate of Return (IRR) for gold jewellery is around 10.3 per cent for investments made between FY2011 and the first half of the current fiscal. However, during the same time gold prices have grown with a compounded annual growth rate of 12.5 per cent.

Advertisement

This becomes significant as the value of Indian households’ gold holdings has continued to rise in recent years, as per the report the value grew to $2113 billion at the end of FY2025-26.

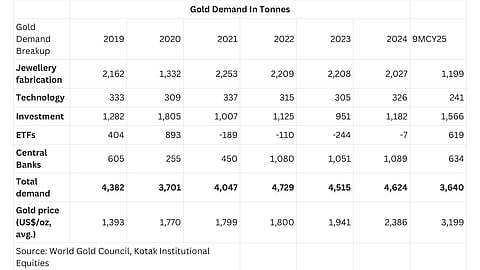

Additionally the demand for gold has been driven by jewellery fabrication in the period between 2019 and 2025. For the nine-month period ended September 30, 2025 the volume of demand for gold jewellery moderated to 1,199 tonnes compared to 2027 tonnes in the previous year. However, gold jewellery continued to drive demand as demand from other segments such as technology, investment, Exchange Traded Funds and Central Banks continued to remain relatively lower.

Furthermore, households with a yearly income below Rs 5,00,000 held almost 70 per cent of the household stock of gold, according to the India Gold Policy Centre (IGPC) PRICE Survey, making them more prone to bear the lower returns. Thus it becomes important to understand why gold jewellery delivers lower returns compared to gold.

Advertisement

Why Do Returns From Gold Jewellery Lag Behind Gold’s Price Rise

The main reason for the relatively poor performance of gold jewellery has to do with the price which Indian households pay to buy the jewellery. The price paid for purchasing gold jewellery consists of additional costs while the money paid for the gold content is only 60-70 per cent of the total price.

The remaining costs typically comprise hefty making charges, design premiums, and precious stones. Kotak also stated in its report that the addition of precious stones like diamonds adds to the total price, this in turn poses another issue. The value of these stones doesn’t tend to appreciate over time and undergoes "steady price corrections". Additionally, upon liquidation of the jewellery, the seller is only paid for the pure gold content.

Kotak mentioned in the report that even breaking-even on an investment in gold jewelry is difficult. The report projected that for an investment in gold jewellery to break-even, the price of gold would need to rally by 25-30 per cent, assuming the prices of precious stones embedded in the jewelry would remain stable.

Advertisement

“In our view, gold jewelry as an investment product makes limited sense, given that gold prices would need to rise 25-30 per cent for households to break even on their purchases (assuming stable prices of precious stones, which may be an optimistic assumption),” Kotak Institutional Equities said in the report.

Aksha Kamboj, Vice President, India Bullion & Jewellers Association (IBJA) told Outlook Money cautioned investors that they may have to hold onto their jewellery for as much as five to seven years just to get break-even returns.

"Jewellery buyers tend to pay approximately 25-30 per cent in additional fees for jewellery that includes making costs and GST. This leads experts to estimate that, after finding the approximate timeframes to regain costs and begin profiting from increased value due to rising gold prices, any buyer of a piece of jewellery should hold on to it for around five to seven years after purchasing it before either breaking even or being in a profitable position," Kamboj said.

Advertisement

In India households often hold gold as a hedge or "insurance against exigencies" or gift the yellow metal during key life events like weddings. However as per the findings of the report, using jewelry for these purposes is inefficient and gives lower returns.

Kamboj added that the liquidity of gold jewellery often comes at discounted rates and may not be helpful in an emergency.

"Many homes consider their jewellery to be an emergency source of “insurance,” but actual cash availability for these items comes very slowly and typically at discounted rates. One needs to locate a buyer, verify the item’s purity before selling it, and then accept a resale price that is lower than retail. On the other hand, one can sell Gold ETFs virtually any time of day and have the cash available almost immediately after trading," Kamboj said.

Advertisement

A Shift Towards Digital Gold

While gold jewellery is a major driver of demand, there has been a significant shift in the nine month period of 2025. In the nine month period, the demand for gold for ETFs and for other investment purposes surged to 619 tonnes and 1,566 tonnes respectively. On the other hand demand for gold for crafting jewellery witnessed a significant decline. This suggests that amid the rally in gold prices Indian investors are adopting a more financially astute approach to gold ownership.

"Long-term-oriented retail investors in Gold ETFs get an excellent blend of liquidity and costs, ease of ownership, and are not locked into any tenure period. If an investor is comfortable holding for over five years, SGBs offer the benefit of fixed interest payments and potentially tax-advantaged status upon redemption at maturity, making them appealing for preserving wealth," Kamboj said.

Show comments

Published At: