After five years of continuous coverage, Abhishek Shukla, 29, a Mumbai-based finance professional, ported his family floater health insurance policy in September 2024 as he was dissatisfied with the offerings. At the time of porting, he was assured that the waiting period benefit he had accumulated in the previous policy for certain diseases would continue in the new policy as well. However, earlier this year, when he raised a hospitalisation claim for his mother, Kusum, 52, the new insurer rejected his claim of Rs 56,156, citing the waiting period exclusion related to an intervertebral disc disorder.

Usually, health insurance policies do not cover certain pre-existing diseases and related treatments for a fixed number of years. That is known as the waiting period. However, once that period is over, the disease gets covered. Health policy is renewable annually and is considered continuous if renewed regularly.

Says Abhishek: “After years of continuous coverage and clear portability assurances, my mother’s hospitalisation claim was denied, citing ‘misrepresentation’, a vague term. The medical clarifications I had submitted (including the doctor’s note saying that the medical records were accurate) were ignored. Health insurance should protect families. This claim needs a fair, transparent, and urgent review.”

1 August 2026

Get the latest issue of Outlook Money

Under the Insurance Regulatory and Development Authority of India (Irdai) rules, waiting periods are not reset when you port a health insurance policy, but are carried forward with specific conditions. The new insurer had initially rejected the claim due to the waiting period issue. Later, when Abhishek called the insurer again, it said that was not a concern, and the reason for rejection was the alleged misrepresentation of documents, but gave no further clarification.

Exclusions are conditions or diseases that an insurance policy does not cover, and one should be aware of these

Such disputes highlight a broader issue many policyholders face: understanding what insurance policies actually cover. While health, life, and motor insurance are meant to provide financial protection, exclusions, waiting periods, and policy conditions often determine what is covered and whether a claim is paid or rejected.

Exclusions refer to conditions or diseases that an insurance policy does not cover. For consumers, these fine-print clauses can make a critical difference at the time of need.

Says Amarnath Saxena, chief technical officer–commercial, Bajaj General Insurance: “Insurance is ultimately a contract of trust, and exclusions are not barriers, but boundaries that define the scope of protection. For consumers, clarity around these boundaries is critical to align insurance with their broader personal finance goals.”

According to grievance patterns observed by Insurance Samadhan, a platform that helps policyholders resolve insurance disputes, in 60 per cent of the cases, the policyholder either lacks information on policy coverages or doesn't understand the requirement of disclosing pre-existing diseases or lifestyle habits at the time of purchase.

Not being aware of these can create problems at a stage when you really need financial support. We take a look at common exclusions in health, life and auto insurance you should know about to ensure you are not taken by surprise in times of need, and your protection is robust.

Common Exclusions

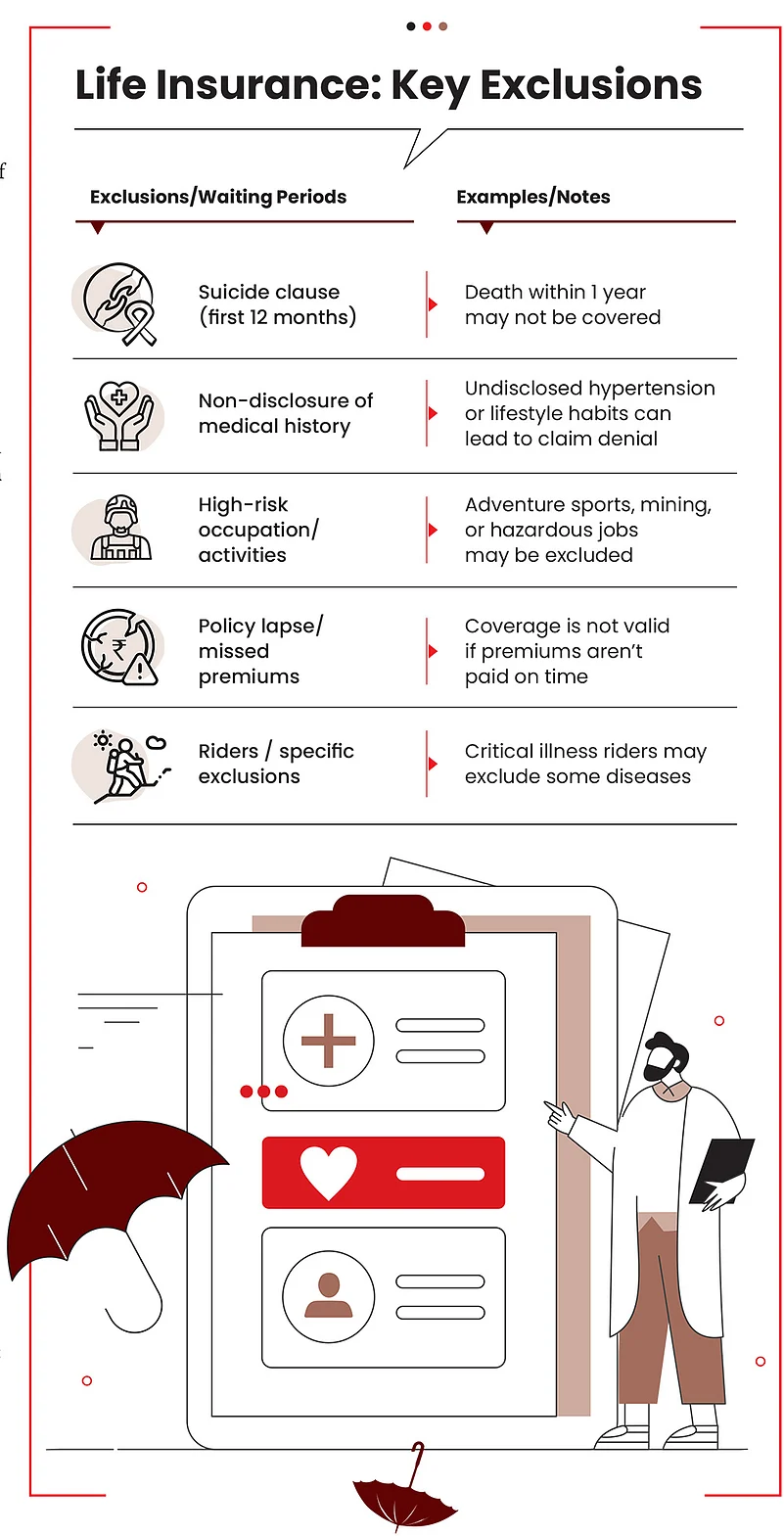

Life Insurance: Life insurance policies often exclude coverage for death occurring under specific circumstances. This may include death by suicide or non-disclosure of specific medical history or lifestyle habits, such as smoking or alcohol consumption not disclosed earlier.

Also, certain occupations and activities are classified as high risk by insurers and death due to these may not be covered. When such details are not clearly understood or disclosed, it can lead to exclusions. Hazardous activity includes aviation (other than as a passenger), deep-sea diving, mountaineering, mining, or working at extreme heights. These could lead to complications during claim settlement if not specified at the time of purchase. For instance, if a policyholder regularly engages in professional rock climbing but does not disclose it at the time of proposal, and death occurs during such an activity, the insurer may reject the claim on grounds of non-disclosure or invoke a specific exclusion clause related to hazardous pursuits.

On the contrary, disclosing them upfront may get you a cover, though at a slightly higher premium, depending on individual circumstances. Insurers typically assess risk on a case-by-case basis, and transparent disclosure improves the chances of securing valid coverage and smoother claim settlement.

Many life insurance policies come with riders that cover specific cases. It is also important to look at exclusions in these policies. For instance, a critical illness (CI) rider may include heart ailment, but exclude cancer. Or it may specify that the said CI should meet specific medical definitions. If that happens, the claim may not go through. Such exclusions, if not clearly understood at the time of purchase, can lead to disputes during claim settlement.

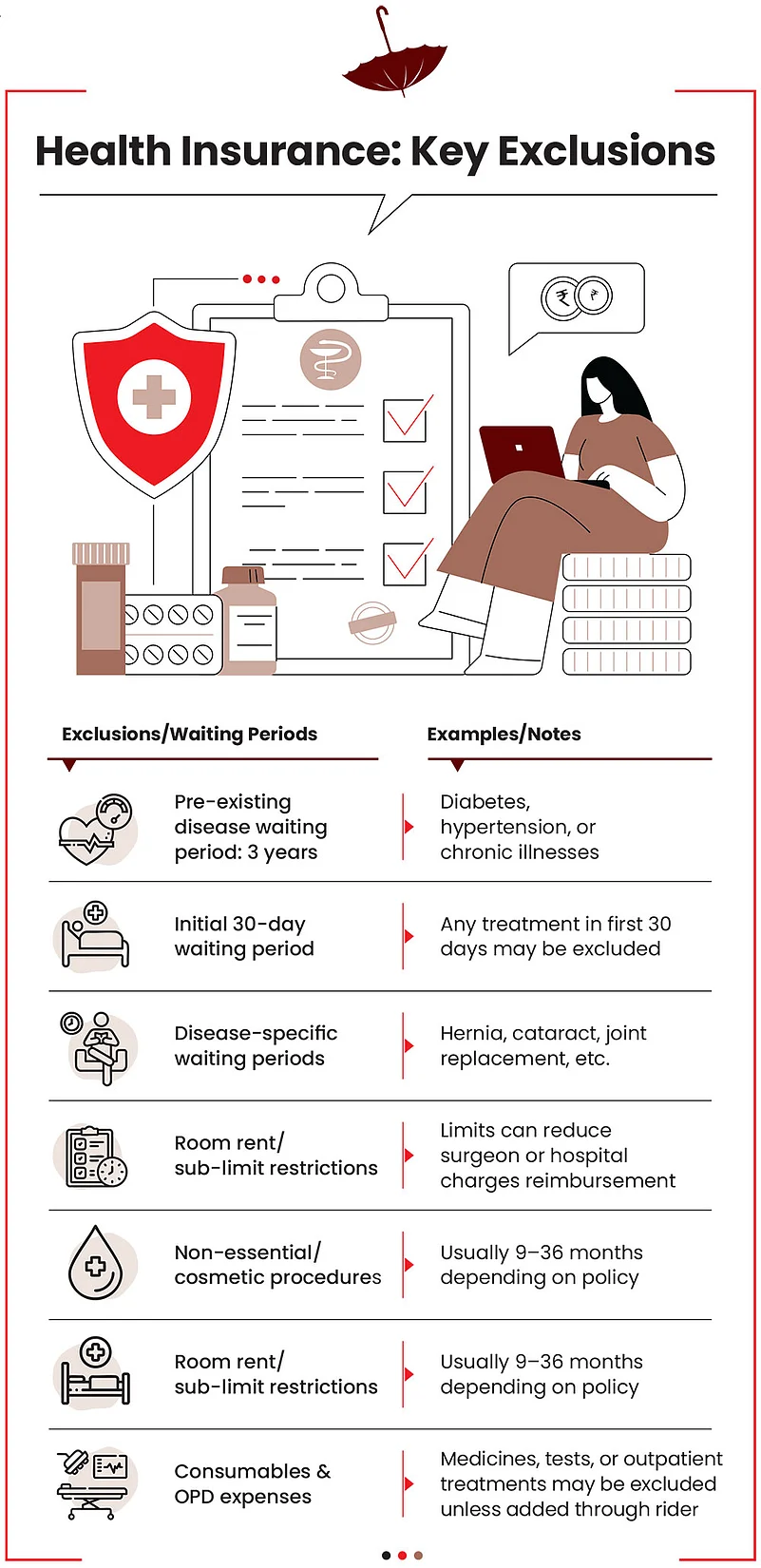

Health Insurance: In health insurance, the most common exclusions include the initial waiting period of 30 days for any coverage; and waiting periods on pre-existing diseases (typically 2-4 years), on specific ailments such as hernia, cataract, joint replacement and so on, and on maternity expenses. For instance, typically, the waiting period or the period after which a policy covers maternity expenses is 2-4 years after the purchase. Also, expenses on consumables or non-medical items such as gloves and masks are excluded from the coverage.

One commonly misunderstood exclusion is room rent sub-limit or restriction. Irrespective of the total sum insured, if the room rent is limited to, say, Rs 2,000, the coverage will be restricted to that amount if the room costs more. What confuses consumers is the fact that usually, the cost of surgery and other associated costs are linked to the room rent. So, a room that costs Rs 5,000 will have a higher bill compared to a room that costs Rs 2,000. If your limit is Rs 2,000 but you take a room that costs, say, Rs 5,000, you will have to foot the extra bill proportionately.

“Many customers assume that any hospitalisation will be fully reimbursed, which is not always true because of these restrictions,” says Shilpa Arora, co-founder and chief operating officer (COO), Insurance Samadhan.

That’s perhaps why there are not just complaints about health insurance claims getting rejected altogether, but also about partial payment of claims.

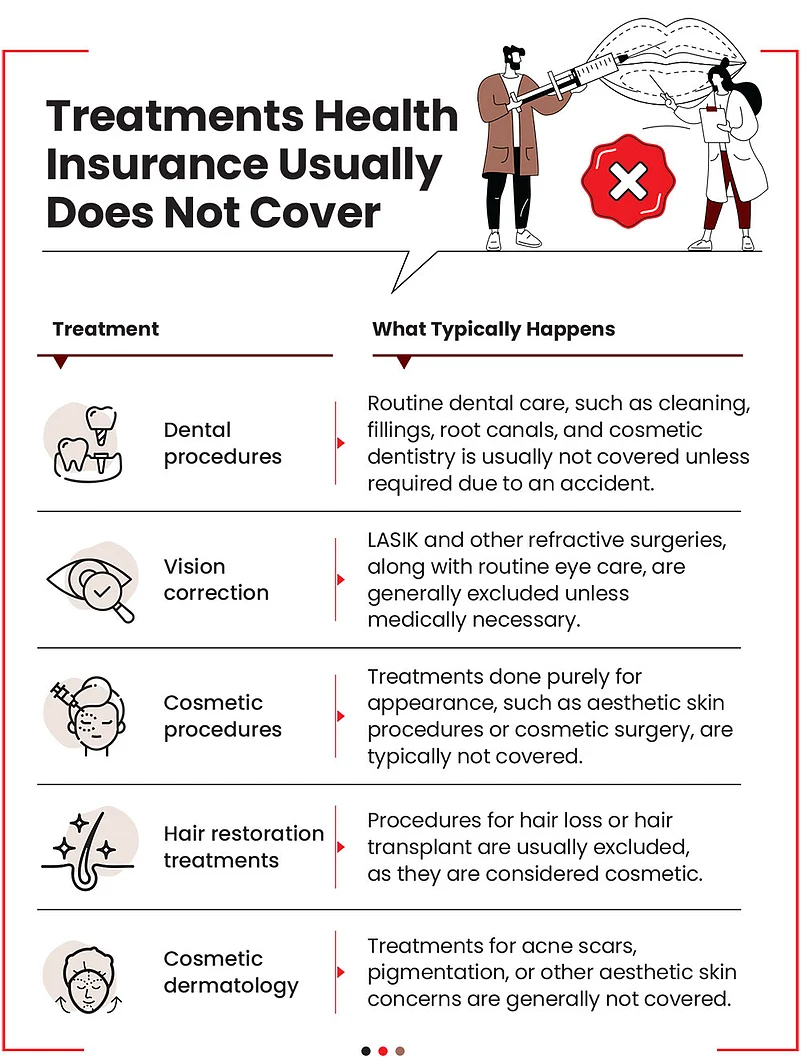

Cosmetic and non-medical procedures are also excluded. Accordingly, most health plans exclude dental treatments and eye care procedures, which are typically not covered unless required due to an accident or hospitalisation.

Routine dental work or vision correction, such as spectacles, is also excluded. However, full disclosure of risks may help secure coverage, though at a higher premium or with specific conditions. For instance, expensive dental procedures, such as root canal treatment, are not covered by standard health insurance policies, but you can pay extra premium to get it covered to an extent. For example, there may be a limit of, say, Rs 25,000, beyond which you will need to pay out of your own pocket.

Routine eye check-ups, spectacles, contact lenses, and vision correction procedures, such as Laser-Assisted In Situ Keratomileusis (LASIK) are commonly excluded. For correction, usually anything beyond 7.5 diopters (the unit for measuring a lens’s optical power) is considered medically necessary, and LASIK surgery is approved for such cases. Below 7.5 is considered cosmetic eye treatment and not covered.

Notably, modern technology-based treatments are generally not excluded. According to Irdai guidelines, insurers are required to cover many “modern treatments”, such as robotic surgeries, laser procedures, and oral chemotherapy. However, coverage is subject to policy terms, including sub-limits, medical necessity, and approved conditions. Treatments considered experimental, unproven, or purely cosmetic may still be excluded. In short, while modern treatments are largely covered today, the extent of coverage depends on the insurer’s terms and conditions.

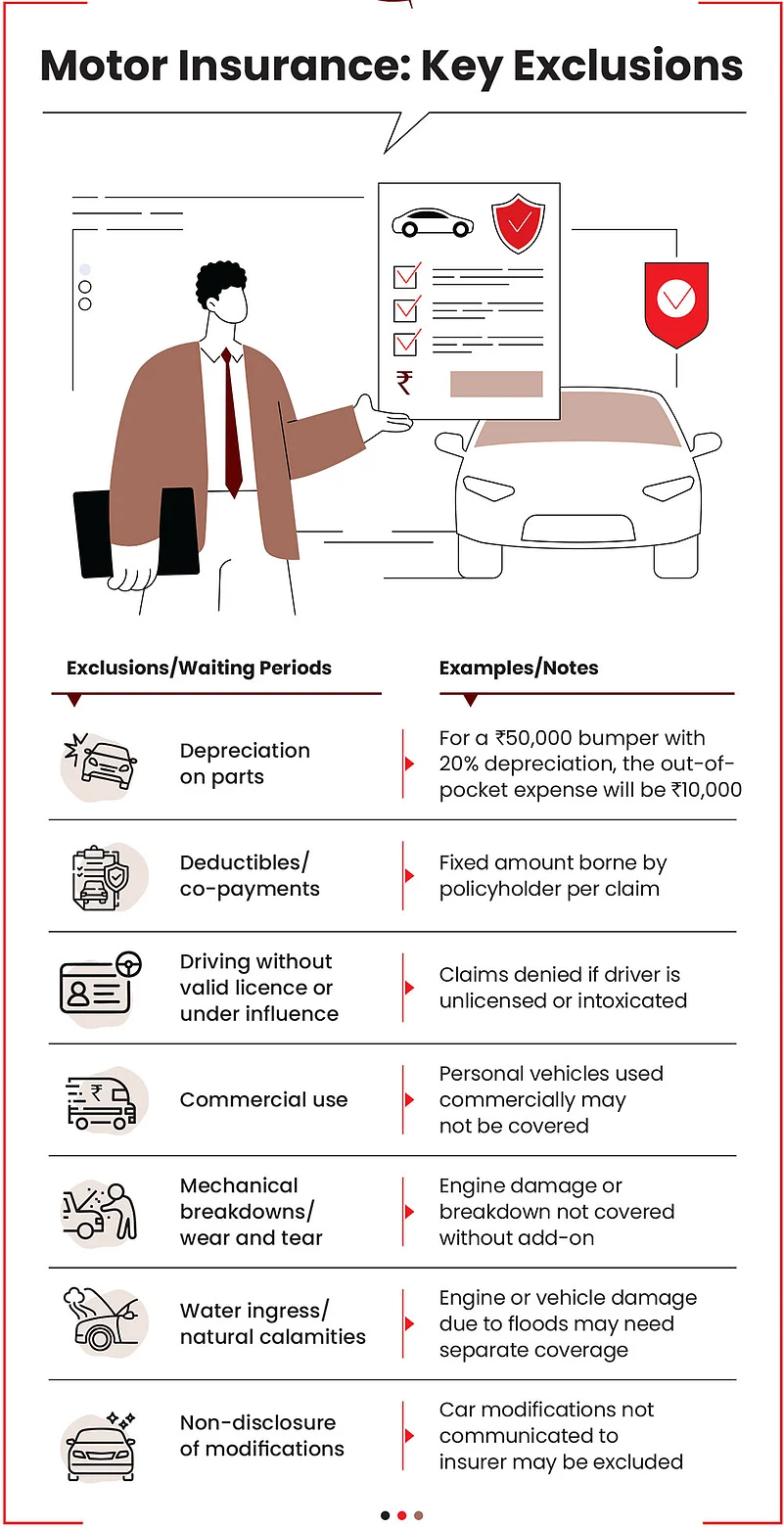

Motor Insurance: The basic mandatory policy that you need to drive your car out of the showroom is the third-party liability cover. It covers damages incurred to another person or property. The basic policy does not include personal accident (PA) cover by default. However, Irdai has made owner-driver PA cover compulsory as an add-on from September 1, 2018, with a minimum sum insured of Rs 15 lakh. The PA cover provides compensation in case of accidental death or permanent disability of the owner-driver. So, legally, both are required.

However, what a lot of people do not know is that to ensure comprehensive protection, they also need to include the own-damage cover, which pays for damages and repairs due to accident, fire, theft or others.

Also, add-ons, such as nil depreciation, engine protection, return-to-invoice, consumables cover, and roadside assistance are highly recommended for enhanced coverage. “Many insurers now offer bundled add-ons that combine multiple benefits in a cost-effective package,” says Saxena.

Without such comprehensive protection, the insurer will not fully cover losses in certain scenarios, leaving policyholders to bear significant out-of-pocket expenses in case of accidents, mechanical failures, or other damages.

The Information Gap

In India, people usually avoid reading the fine print and blindly believe what the distributor tells them. And that’s where the problem starts.

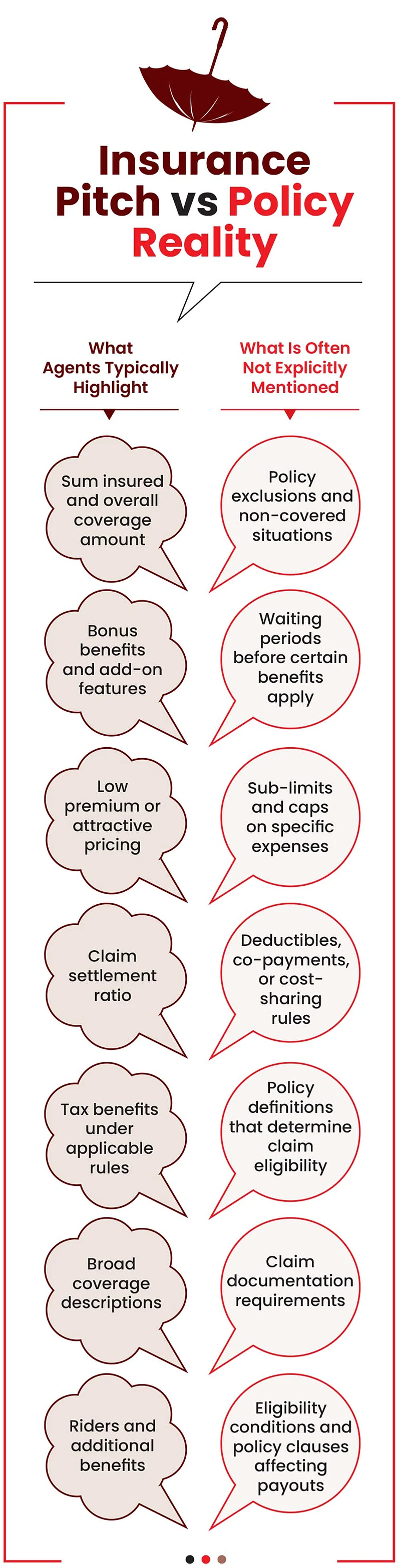

Previously, most agents and distributors were either neighbours or friends, who didn’t understand complex conditions themselves. Selling insurance was often a second gig for them. New age distributors are seemingly more focused on meeting their sales targets, driven by commissions. As a result, when selling a policy, they usually emphasise the benefits, and not the exclusions. Even now, some do not have full clarity on exclusions, and typically get back to the head office for clarity.

Says Aayush Dubey, co-founder and head of research, Beshak.org, an independent insurance advisory platform: “We have conducted test audits of life and health insurance sales conversations, and the results are quite revealing. In life plans, we rarely see agents proactively explain exclusions of the base policy or riders. In health plans, some agents do explain broad categories, such as permanent exclusions or waiting periods, but the full list of exclusions is rarely discussed in detail.”

Most sales conversations focus on benefits, coverages, and attractive features because those are easier to communicate and align with what buyers want to hear.

They rarely explain complex clauses, leaving policyholders unprepared, leading to claim rejections, partial settlements, or delays. Says Arora: “A frequent pattern seen in complaints is that customers often report that during the sales process, agents typically highlight the sum insured, low premiums, claim settlement ratio, and tax benefits. However, policy exclusions, waiting periods, sub-limits and caps, deductibles, and claim documentation requirements are often not clarified.”

On the buyer side, few care to read the details before buying a policy. So while the information exists in the policy documents, most buyers don’t fully understand the conditions and exclusions in a policy.

Skipping details about exclusions, sub-limits and other conditions, however, leads to incomplete knowledge about the coverage.

The Claims Problem

Being unaware of exclusions leads to the biggest problem of all: hitting a dead-end when you really need the money.

Life Insurance: Life insurance is often the most important financial safety net for dependents in middle-income families. It can save a family from financial ruin in case of the breadwinner's unexpected demise.

Says Sarita Joshi, head of health and life insurance, Probus, an insurance broker, “If policyholders do not properly understand the exclusion clauses in their life insurance policy, claims may be rejected or disputed when their dependents need it the most.”

According to the Irdai annual report 2024-25 for the life insurance industry, the individual death claim settlement ratio reached 98.71 per cent in 2024-25, a slight increase from 98.54 per cent the previous year. For the total 1.12 million death claims reported, insurers paid a total of Rs 31,439 crore. A vast majority of claims were honoured, while the total number of grievances were 33,280 for the year.

However, Irdai now mandates compulsory claim payment after a life insurance policy has been in force for at least three years, and insurers cannot reject claims for non-disclosure or mis-statements, except in cases of proven fraud.

Health Insurance: Health insurance contributes the highest number of claim disputes, mostly related to exclusions, waiting periods, or conditions. Irdai’s annual report shows that complaints about health insurance rose 41 per cent to 137,361 in FY25, mostly over claims, delays, and incomplete settlements.

According to a survey by LocalCircles, a community platform and citizens’ pulse aggregator, released in March 2026, around four in 10 respondents said their health insurance claims were either rejected or only partly settled. Some said they were not given clear explanations when insurers reduced or declined their claims.

Says Dubey: “Exclusions typically become apparent when a claim in filed. That’s why it’s important to understand clauses around waiting periods, sub-limits, policy definitions, documentation or eligibility conditions.”

Rohitasyo Chatterjee, a 45-year-old Kolkata-based policyholder, faced a troubling situation when his 72-year-old father was recently diagnosed with aortic stenosis, a serious heart condition requiring urgent treatment. His health insurance claim with a leading insurer was rejected twice, on contradictory grounds.

The first rejection cited the condition as a pre-existing disease under permanent exclusion, allegedly pointed out at the time of underwriting. Rohitasyo disputes this, stating the ailment was neither diagnosed nor known when the policy was purchased. A second rejection letter shifted the basis to non-disclosure of material facts, even listing asthma as a pre-existing condition, something he denies.

Following multiple appeals, the insurer offered to reconsider the claim, but only if Rohitasyo agreed to a permanent exclusion for “valvular heart disease and related complications”, a move that could impact future coverage.

Says Rohitasyo: “I have requested the insurer to process the claim as per the policy terms. I am also seeking guidance from consumer rights experts and trust that Irdai will safeguard policyholder interests. We need greater transparency, accountability, and consumer protection in health insurance.”

Motor Insurance: Mismatch of expectations is the main problem in motor insurance policies. Says Arora: “Motor insurance disputes generally occur when customers assume that all damages are covered, which is not the case.”

Issues also arise because a motor vehicle is a depreciating asset and policies have clear information on deductibles, depreciation rules, and coverage conditions.

Also, there are certain clauses for which motor insurance claims are rejected. Motor insurance complaints fell from 26.18 per cent in FY 2023-24 to 24.80 per cent in FY 2024-25, according to the latest Irdai annual report. There has been a slight improvement in motor insurance claims.

Says Arora: “Claims may also be rejected if a private vehicle is used for commercial purposes. In addition, insurers may deny claims for engine damage caused by water ingestion, and policyholders may have to bear the depreciation cost of parts if a zero-depreciation cover has not been purchased.”

What You Should Do

Fill The Form Yourself: Claim disputes often arise due to issues such as non-disclosure of medical history, incorrect or misreported information in the proposal form, or being unaware of exclusions.

Letting distributors fill the forms without reading them can lead to misreporting of medical and other conditions. You may even miss filling out important details.

Says Arora: “In many cases, policyholders rely on agents to fill out application forms, and important disclosures may be overlooked. These omissions can later create complications during claim assessment and may lead to claim rejection.”

In both life and health insurance, hiding key medical history can have disastrous results. “It is important to understand the situations in which claims may be rejected, including non-disclosure of medical history or treatment exclusions,” says Yadav.

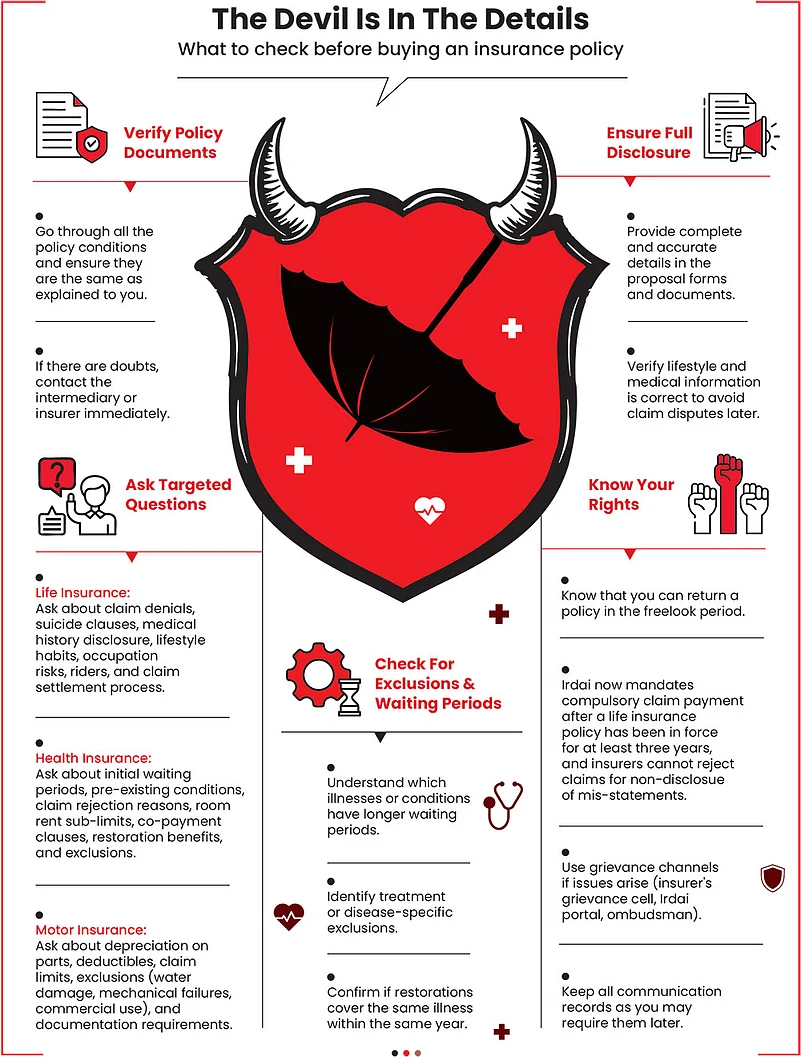

Therefore, policybuyers must ensure they provide complete disclosure of all material facts and information requested by the insurer in the proposal form and other related documents before the insurer can evaluate a potential risk for underwriting. “Further, they should carefully read and verify any lifestyle and medical information provided to the insurer in the proposal form to determine that it is complete and accurate,” says Puri.

Study The Contract Carefully: The insurance document specifies all conditions and exclusions. Consumers must go beyond brochures and read the policy document, which is the legally binding text that lists all exclusions.

Says Ashish Yadav, senior vice president, business operations, ManipalCigna Health Insurance: “Irdai mandates that this is published on every insurer’s website and provided at the time of purchase. There is proper due diligence one needs to do when buying any kind of insurance policy, especially when you are buying it from an agent.”

In fact, Irdai has mandated that all insurers must provide a Customer Information Sheet (CIS) that outlines all important aspects of assets for the insured person. “It includes details about coverage, exclusions, and claims procedures to assist the insured person to better understand the policy,” says Dr. Santosh Puri, head, retail underwriting, Tata AIG General Insurance.

Customers should also acknowledge receipt by providing a signed acknowledgement confirming that they have reviewed and understood the contents of the document.

Ask The Right Questions: In case you find all that too tedious and difficult to understand, ask the right questions before buying the policy. Ask specific questions rather than relying on a general product pitch.

Find out the circumstances under which a claim may be denied. For instance, in life insurance, policybuyers should understand the time frame of suicide clauses, the importance of disclosing their health history and lifestyle habits (such as smoking or alcohol consumption), and whether their job or activities are considered high risk, which could lead to exclusions.

“Buyers should also ask about policy limits, riders attached to the policy, and the claim settlement process. Requesting for written clarification or examples of potential claim scenarios can help buyers better understand the policy terms and avoid surprises at the time of claim settlement,” says Joshi.

When purchasing a health insurance policy, clarify how long the initial waiting period is, and identify which illnesses may have longer, separate waiting periods. Other key questions include details about pre-existing conditions, their definition, and if and when they are finally fully covered. In health insurance, it is important to find out how the room rent sub-limit will affect other claim components, such as surgeon’s fees.

Check for co-payment clauses and situations they apply. Many policies now come with a restoration benefit, which entails automatic reinstatement of the sum insured after it is exhausted in a policy year. However, it is important to find out if it covers the same illness twice a year, and for different family members if it is a floater policy.

For motor insurance, it’s important to ask targeted questions and keep certain factors in mind.

Start with depreciation on car parts. Dubey suggests the following question: “If my car parts are replaced during a claim, how much depreciation will apply, and how much will I have to pay from my pocket?”

As mentioned earlier, if you do not have a zero depreciation add-on, then the insurance will not cover your claim. For instance, if your car’s bumper costs Rs 50,000 to replace and the insurer applies 20 per cent depreciation, you would have to pay Rs 10,000 yourself. If you had a zero depreciation add-on, the insurer would cover the full Rs 50,000.

When buying health insurance, ask about the waiting period, illnesses which have separate waiting periods, and pre-existing conditions that are not covered

Ask about deductibles, claim limits, and exclusions (for instance, damage from water, mechanical breakdowns, or commercial use), so that you are aware of what’s not covered. Also, check documentation requirements, waiting periods, and the claim process.

Do Your Due Diligence: Consumers should always validate the agents' verbal explanations against the information provided under the prospectus, sales brochure, customer information sheet, and written policy documentation received from the insurer.

Says Pradeep Funde, senior vice president, Anand Rathi Insurance Brokers: “Irdai explicitly advises policyholders to verify that the policy document matches what was explained at the time of the sale. Go through all the policy conditions and ensure they are the same as explained to you. If you have doubts, contact the intermediary or insurance company immediately.”

Conclusion

Irdai has been actively pushing for reforms in the insurance sector to simplify policies and products for its consumers.

Says Saxena: “Irdai constituted a committee to work on simplifying insurance policies. It is encouraging insurers to adopt standardised exclusions, ensuring that customers clearly understand what is not covered under their policies. At the same time, Irdai is driving the move towards simplified product structures to make offerings easier to compare, more transparent, and more accessible for policyholders.”

However, it’s still a long road as insurance products can be complex.

Insurance is meant to be a safety net, but its strength lies in the details. Keeping these factors in mind will ensure your policy aligns with your financial protection goals and there are no disputes later.

Also, it will save you from out-of-pocket expenses. “Asking these questions in advance will help policybuyers understand potential out-of-pocket costs and avoid financial surprises at the time of a claim,” says Yadav.

Exclusions, waiting periods, and conditions define what protection actually looks like when a crisis strikes. For consumers, reading beyond the sales pitch and understanding the fine print can be the difference between financial security and an unexpected claim shock.

meghna@outlookindia.com