Aarti (name changed), a freelance designer based in Delhi, is forced to turn down projects one month because she has too much on her plate. The next month, she could be refreshing her inbox, waiting for a client to confirm an assignment or payment that has already been delayed twice.

In another metro, Rohit (name changed), a start-up employee, had a different, but somewhat similar experience. In August 2025, when his salary got delayed by a few days, he thought it was a one-off for a company trying to find its feet. The delays soon stretched into weeks and months down the line, the company announced layoffs. Thankfully, his name was not on the list.

Rohit and Aarti represent a quiet but sweeping shift in how Indians earn and live. For a growing number of people, and not just freelancers, the old financial playbook built around a predictable monthly pay cheque now feels outdated.

1 July 2026

Get the latest issue of Outlook Money

India’s workforce is becoming more flexible, more entrepreneurial, and in many ways, more opportunity-driven than ever before. But it is also becoming more exposed to income volatility. The challenge now isn’t just about earning more. It’s also about learning to navigate the unpredictability, thanks to the advent of technology, rise of contractual roles, global instability, and other factors.

The numbers confirm the story. According to NITI Aayog and the Economic Survey 2025-26, India’s gig and platform economy employed about 7.70 million workers in FY21, which increased to about 12 million workers in FY25; that number is expected to surge to 23.50 million by 2029-30.

But beneath that growth lies a fragile reality. Multiple surveys suggest that a majority of gig workers struggle to manage household expenses due to erratic incomes.

For around 40 per cent, according to the Economic Survey 2025-26, take-home earning is below Rs 15,000 a month.

The irony is difficult to ignore. At a time when income certainty is fading, the need for financial security is becoming more urgent. Without the cushion of a steady salary, individuals are more exposed to economic shocks, making disciplined saving and investing not just important, but indispensable. The question, therefore, is not whether to invest, but how to build a strategy that adapts to fluctuating income without compromising on future goals.

The Problem

The reality is that earnings may fluctuate wildly for an average worker in India, but the expenses don’t. The adjustment then shows up in quieter and more personal ways.

When income becomes unpredictable, financial behaviour changes almost instinctively. Budgeting turns from a structured plan into a rough guess. You hesitate making a big purchase even after a good month and hope nothing unexpected comes up to disturb the balance. Or worse, you overspend in the good months, and struggle to make ends meet in the bad ones.

Almost always, saving becomes the first casualty during dry spells, as investing starts to feel like something that can be postponed. So you end up missing that systematic investment plan (SIP) instalment, hoping you will make up for it later when you have extra.

Without the cushion of a steady salary, budgeting turns into a rough guess and savings become the first casualty during dry spells of no income

But that can become an endless loop. Over time, this quiet shift can have loud consequences. Retirement planning gets pushed further away. Wealth creation slows down.

The only way then is to nip it in the bud. For Rohit, the layoff announcement was a wake-up call. “For the first time, I looked at how many months would my savings last if my income were to stop completely,” he says.

Says Sanjiv Bajaj, joint chairman and managing director, Bajaj Capital, an investment services group, “For those with irregular income, the first mistake is waiting for income to stabilise; it rarely happens. The second is forcing salaried employee strategies on themselves. Both create stress instead of wealth. Irregular income requires flexible systems, not rigid rules.”

The Solution

Personalise Your Budget: Financial planners recommend a shift in mindset, prioritising personalisation. Uneven income means high-income phases need to be optimised for future use.

“Individuals with irregular income should think in terms of ‘income cycles’ rather than months,” says Col. Sanjeev Govila (retd), CFP, and CEO, Hum Fauji Initiatives, a financial advisory firm.

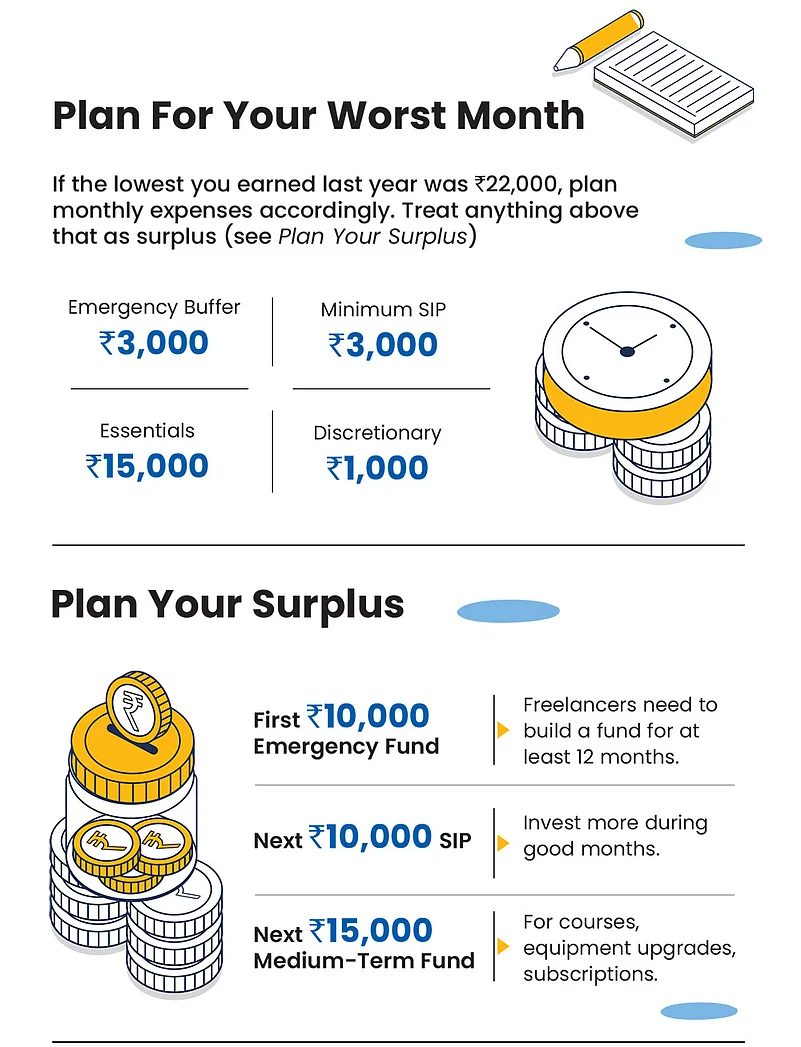

Shweta Rajani, mutual fund head at Anand Rathi Wealth, says financial decisions cannot follow a one-size-fits-all template for those with fluctuating incomes. The starting point, she says, is to establish a baseline by calculating the minimum monthly expenses, such as rent, equated monthly instalments (EMIs), groceries, insurance premiums, and any other recurring bills. Investments and discretionary spends should follow in that order.

She explains through an example. “If a freelance graphic designer’s monthly income is between `30,000 and `1.50 lakh, they should plan according to their lowest consistent monthly figure, say `40,000, and treat everything above that as surplus. From their monthly income, they should allocate funds to essentials first, then top up their emergency funds, and then proceed with their investments.”

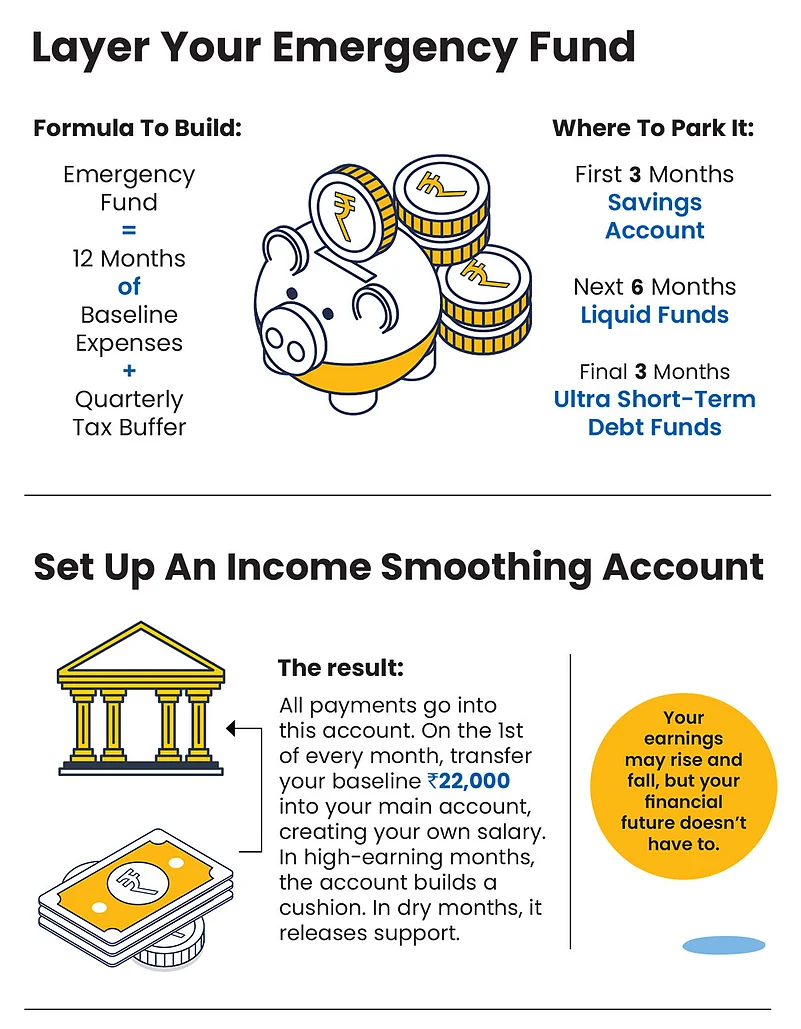

Focus On Stability: Experts agree that focusing on protection can build stability, which should be the first priority. “Maintaining a liquid account with 9-12 months of essential expenses acts as a buffer, providing stability and liquidity in case of any emergency,” says Rajani.

Emergency funds should remain in highly liquid instruments, such as liquid funds, short-duration debt funds, or bank fixed deposits, which can be accessed quickly when income flows become uneven.

Govila suggests a tiered approach. He says: “Keep three months (of expenses) in savings account, six months (of expenses) in liquid funds, and additional money in low-risk debt instruments. Importantly, calibrate it to income volatility and not just expenses. Highly cyclical professions may require buffers closer to as much as 18 months.” This approach helps convert uneven earnings into a more stable, quasi-regular investing capacity, he adds.

A strong emergency fund also prevents the need to dip into long-term investments during tough periods and helps keep financial goals on track.

Plan For Goals: For the medium-term basket, one can consider building a growth-with-stability-based portfolio with 70:30 ratio across equity and debt, says Rajani. Once the liquidity buffer and medium-term bucket are created, you can start allocating the remaining capital towards long-term growth assets, such as equity.

Says Rajani: “Investing in diversified active equity mutual funds such as market cap-based funds, and strategy-based funds such as contra, value, and focused funds, helps get exposure across categories, segments, and sectors, reducing concentration risk, while improving portfolio stability and liquidity, thus helping ride across market cycles.” She suggests arbitrage funds for individuals in the higher tax brackets for parking short-term surplus funds or the debt portion of the portfolio.

One can create a portfolio in 70:30 ratio in equity and debt for the medium-term, and allocate the rest for the long term

Focus On Flexible Products: It’s important to prioritise modular portfolios that have assets that can be scaled up or paused without penalty. Index funds, liquid funds, and target maturity debt funds fit this tag well.

Says Govila: “Avoid illiquid commitments, such as traditional insurance-heavy products. Also, maintain a tactical allocation mindset by deploying aggressively during income spikes, but protect downside through high-quality debt during uncertain phases.”

Adapt And Innovate: For those with irregular income, investment discipline is less about fixed commitments and more about building a system that can adapt.

One way is to set a modest “minimum SIP”, an amount you can invest even during lean months. For instance, a steady SIP of `5,000 is far more effective than a `25,000 plan that gets paused whenever income dips. This ensures continuity, keeps compounding intact, and avoids the stop-start cycle.

“During high-income phases, surplus funds can be deployed as lump sum investments to accelerate wealth creation. Over time, this balance between consistency and flexibility helps smooth out income volatility,” says Rajani.

Govila suggests another approach: a ‘self-funded SIP’, where all income inflows are first parked in a liquid fund, and a steady, conservative SIP is then automated from that pool.

He says: “This structure helps maintain investment discipline without being tied to the timing of income. It also creates room for smarter allocation. During market corrections, investors can deploy opportunistic lump sums, similar to the ‘bullet investing’ strategy often used with funds set aside for systematic transfer plans (STPs).

This allows them to take advantage of dips, an opportunity that rigid SIP-only strategies may miss.”

The real edge lies in creating a financial plan that absorbs shocks, adjusts to income cycles, and still moves steadily towards long-term goals. In the end, it’s this blend of flexibility and resilience that will keep you on track, no matter how uneven the journey.

sanjeev.sinha@outlookindia.com