Summary of this article

Financial planners recommend SCSS as one of the safest investment options after retirement.

SCSS interest rates are currently at 8.2 per cent, guaranteed by the government to help you earn a decent return on your savings to meet your daily expenses.

SCSS is not going to make you rich after retirement. But what it can do is allow you to sleep peacefully at night without your investments being affected by the stock market cycles.

Welcome to retirement. The investing playbook changes when you enter the pension phase. Building wealth aggressively is no longer the goal. Now, it’s about capital preservation and investing for a regular payout. If you want that to happen for your retirement funds, consider the Senior Citizens Savings Scheme or SCSS.

SCSS is an investment scheme backed by the government. You can invest your savings in this secure investment scheme which offers fixed returns and regular pay-outs. Financial planners recommend SCSS as one of the safest investment options after retirement due to these features. Additionally, SCSS interest rates are currently at 8.2 per cent, guaranteed by the government to help you earn a decent return on your savings to meet your daily expenses.

Who’s Eligible To Invest?

If you fall under any of the below categories, you can invest in SCSS:

Less than 55 years: No.

60 years or older: Yes.

Age between 55 and 60 years: Only if you retired on superannuation

Note: NRIs and Hindu Undivided Families (HUFs) cannot invest in SCSS.

Key Features

Minimum Investment: Rs 1,000

Investment cap: Rs 30 lakh in all SCSS accounts opened by an individual.

Interest rate: Currently at 8.2 per cent per annum

Tenure: Initially for 5 years which can be further extended by another 3 years.

Interest payout: Quarterly

Can be opened at post offices, and authorised banks

Transferable to any part of India.

Why SCSS For Retirees?

When investing after retirement, every investor’s concern is safety of capital and steady returns. SCSS scores high on safety as it is backed by the government, virtually eliminating investment risk. Let’s look at other benefits.

Predictable returns: Investors receive quarterly interest payouts from their SCSS account. Consider it as your pay-cheque replacement.

Tax-saver: Investment in SCSS is eligible for tax deduction of up to Rs 1.5 lakh under section 80C of the Income Tax Act.

Deposit for life: Since SCSS is refundable after 5 years (extending up to 8 years), you can continue investing it for as long as you want. You can transfer your SCSS account to any other part of India too.

Other Rules

Investment begins once you open the account. It matures in five years from the date of the first deposit. Prior to maturity, the scheme cannot be withdrawn, but can be extended by a further three years on applying before the maturity date.

Nomination: One family member can be nominated at the time of account opening or at a later date. Accounts can be held individually or jointly with your spouse.

Multiple accounts allowed: One person can open multiple SCSS accounts in their name or together with their spouse

Premature withdrawals are permitted one year after account opening. Penalty for premature withdrawal is 1.5 per cent if the account is closed after one year, but before two years. If closed after two years, the penalty is 1 per cent.

The Senior Citizens Savings Scheme is open for Indians aged 60 plus, 55 plus for VRS retirees, and 50 plus for defence personnel. One can invest up to Rs 30 lakh per individual whereas couples can invest Rs 30 lakh each separately. Currently, the annual simple interest provided under this scheme is 8.2 per cent which is paid quarterly.

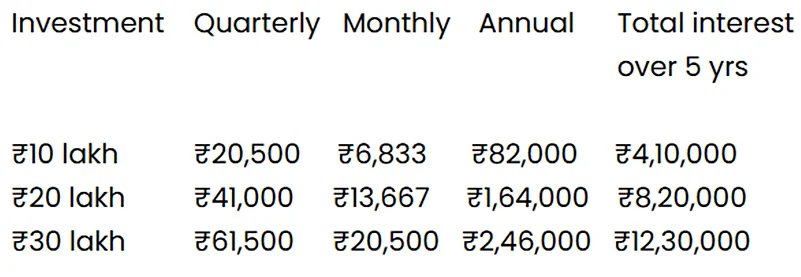

Thus, at an interest rate of 8.2 per cent under the Senior Citizens Savings Scheme:

Rs 10 lakh investment earns about Rs 6,833 per month (indicative), Rs 20,500 every quarter, Rs 82,000 annually, and Rs 4.1 lakh over 5 years.

Rs 20 lakh investment earns about Rs 13,667 per month (indicative), Rs 41,000 every quarter, Rs 1.64 lakh annually, and Rs 8.2 lakh over 5 years.

Rs 30 lakh investment earns about Rs 20,500 per month (indicative), Rs 61,500 every quarter, Rs 2.46 lakh annually, and Rs 12.3 lakh over 5 years.

At maturity, one would get the full principal back. So, for example, Rs 30 lakh invested will return Rs 42.3 lakh total after 5 years.

“However, the interest is fully taxable at one’s tax slab. So, in the 30 per cent bracket, the effective return drops to roughly 5.7 per cent. So, a couple can together park Rs 60 lakh (Rs 30 lakh each) and get Rs 41,000 per month combined,” says Abhishek Kumar, Founder of SahajMoney.

Also, if one needs a monthly payout, they can pair SCSS with the Post Office Monthly Income Scheme, which currently offers 7.4 per cent annual interest, credited monthly.

Final Thoughts

SCSS is not going to make you rich after retirement. But what it can do is allow you to sleep peacefully at night without your investments being affected by the stock market cycles. If you want to know where your money is going every quarter and not worry about your investment losing money, SCSS should be your top post-retirement investment option.