If you are in the habit of saving and investing mindfully, accumulating a corpus for retirement should not be difficult for you. But that’s only half the battle won. The other half is about the decumulation phase, where you need to divide your corpus into regular cash flow after retirement.

For decades, the retirement story under the National Pension System (NPS) followed the accumulation script for the most part: work hard, save regularly, and withdraw 60 per cent lump sum upon retirement. The remaining 40 per cent had to be compulsorily invested in an annuity or pension product, mostly available with insurance companies as of now. Recently, the lump sum option was increased to 80 per cent of the corpus.

On May 15, 2026, the Pension Fund Regulatory and Development Authority (PFRDA) gave subscribers the option to annuitise the 80 per cent lump sum through a new scheme under NPS. It’s called the Retirement Income Scheme (RIS) Steady with two drawdown or withdrawal options.

1 July 2026

Get the latest issue of Outlook Money

The idea is to provide regular income even as the corpus remains invested and keeps earning interest. The PFRDA circular says: “The primary objective is to optimise periodic payouts for subscribers during the decumulation (payout) phase through drawdown options through the specific life cycle fund for decumulation under NPS. It aims to enhance cash flow predictability and corpus longevity through continued support to corpus appreciation, thus minimising the risk of early exhaustion of the corpus before the end of the drawdown period.”

Note that there is an existing drawdown scheme, called the systematic lump sum withdrawal (SLW). Under this, you can get the corpus in instalments, which can be determined based on the age (up to 85 years) or the amount you select (as long as the corpus lasts as per the amount). It works like a steady monthly income. The remaining money stays invested in NPS as per your asset allocation.

RIS works differently. It aims to counter inflation while providing a defined equity tapering structure.

What Is RIS Steady?

It is similar to the life-cycle fund at the time of accumulation, where the equity portion reduces as age progresses. It will start with a 35 per cent equity exposure at the age of 60, which will taper down to 10 per cent by the time one hits 75 and will remain so till age 85. The remaining funds will be invested in other asset classes, including corporate bonds and government securities (G-secs).

RIS is similar to the life-cycle fund at the time of accumulation where the equity portion reduces as age progresses, from 35 per cent to 10 per cent

This defined asset allocation mix will ensure that the capital remains protected, with a growth kicker to the corpus through equity exposure.

Within this scheme, there are two drawdown or withdrawal options: Systematic Payout Rate (SPR) and Systematic Unit Redemption (SUR).

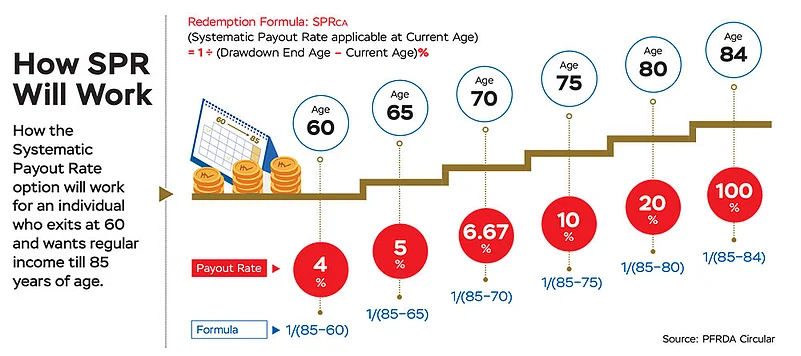

Systematic Payout Rate: SPR is the default option. Under this, the withdrawable amount will be calculated based on the subscriber’s current age and the remaining drawdown years. The payout will be a percentage of the total current corpus.

The formula to calculate SPR is: SPRCA (SPR applicable at Current Age) = 1 ÷ (Drawdown End Age – Current Age) %. For instance, if you exit NPS at age 60, with 25 years left till 85, the initial payout rate will be 4 per cent. Using the formula, the payout (SPR) will increase with each passing year (see How SPR Will Work).

Under this method, the payout rate will be determined every year on the subscriber’s birthday based on the prevailing market value of the corpus.

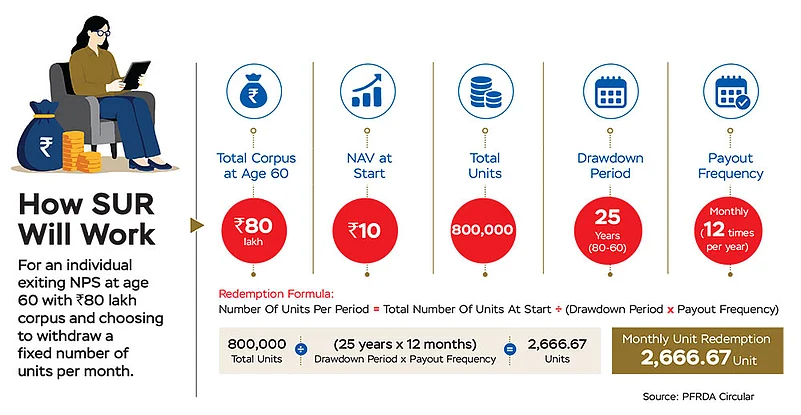

Systematic Unit Redemption: This is not a default option, so you would need to specifically choose it if you find it more suitable.

Under this, you will get to withdraw a fixed number of units, which will be decided at the start of the drawdown phase based on the chosen payout frequency (monthly, quarterly, or annually). The number of units will be liquidated at the chosen intervals. While the number of units will remain the same, the actual cash flow may vary depending on the market value of the units on the day of withdrawal.

The formula to calculate SUR is: Number Of Units Per Period = Total Number Of Units At Start ÷ (Drawdown Period x Payout Frequency). Let’s take the example of a retiree exiting the workforce at the age of 60 with a corpus of Rs 80 lakh. If the retiree chooses monthly withdrawal till age 85, he will get the current value of 2,666.67 units per month (see How SUR Will Work).

Will It Work For You?

Guarantee Vs Risk: Though SLW offers a fixed amount withdrawal, it may come at the cost of growth and may be unable to counter inflation.

Says Anuj Kesarwani, certified financial planner (CFP), chartered trust and estate planner, and founder of Zenith Finserve, a financial advisory firm: “Guaranteed cash flow has its own downside. The capital is invested in fixed-income securities that may not be able to counter inflation, so the capital may start depleting over time.”

While equity exposure under RIS provides growth, it also comes with risks. Notably, the PFRDA circular explicitly mentions that there’s “no guarantee or assurance clause in respect of periodic payouts” and “the payouts are subject to market risks”.

So is RIS suitable for you? Says Sriram Iyer, managing director and chief executive officer, HDFC Pension Management: “RIS is suitable for those who prefer a blended approach: one portion can provide guaranteed income through annuity, while the balance can remain invested under RIS and participate in market-linked growth. Subscribers seeking defined and guaranteed post-retirement cash flows may be better served by an annuity. Even after RIS is introduced, they may still choose to allocate more than the mandatory 20 or 40 per cent of the corpus to annuity if they prefer lower market exposure.”

RIS allows exit mid-way. The balance corpus can either be withdrawn or added to the annuity. In traditional annuities, that is not possible

The NPS drawdown options are also not without its caveats. Kesarwani says, “It can be considered as an addition to the currently available options. The biggest risk in NPS or most government schemes is the regulatory risk. The rules can change at any time. So, using the entire fund is not suggested.”

Also, even if equity exposure is limited to 10 per cent of the corpus after 75 years of age, if the market goes through a prolonged bear phase, the corpus value could decrease because SPR is reset every year.

Says Iyer, “One needs to plan before choosing the instrument for deploying the commuted portion of the corpus. This should be done keeping in mind the urgent or delayed need for cash flow. RIS offers a structured option to retain a portion of the corpus within NPS while also enabling phased withdrawals. The portion retained follows a reducing equity trajectory with advancing age, which helps lower risk over time.”

For many retirees, taking exposure to equity separately and keeping track of it may be difficult, but these are built into RIS, which will be managed by professional fund managers.

Flexibility: RIS allows exiting mid-way. The balance corpus can either be withdrawn or added to annuity option. In traditional annuities, the principal cannot be withdrawn once the product is bought.

Rajesh Khandagale, senior vice president - NPS, KFintech, a central recordkeeping agency (CRA), says, “A subscriber can opt out of RIS at any point and withdraw the balance as a lump sum. This option is not available for the annuity portion of the corpus.”

This option is suitable for someone who wants to keep control over their money, wants to keep it simple, has decent capital, and has a very long-term horizon, says Kesarwani.

While the decumulation scheme and withdrawal options have been announced, these will take effect only after operational infrastructure is in place. Meanwhile, subscribers can explore its suitability for them.