Life insurance claim rejection after Rs 25 lakh policy non-disclosure of illness

NCDRC ruling stresses disclosure of pre-existing disease in life insurance

Medical records showed cancer diagnosis before policy purchase stage

Accurate proposal form disclosure prevents future life insurance claim disputes

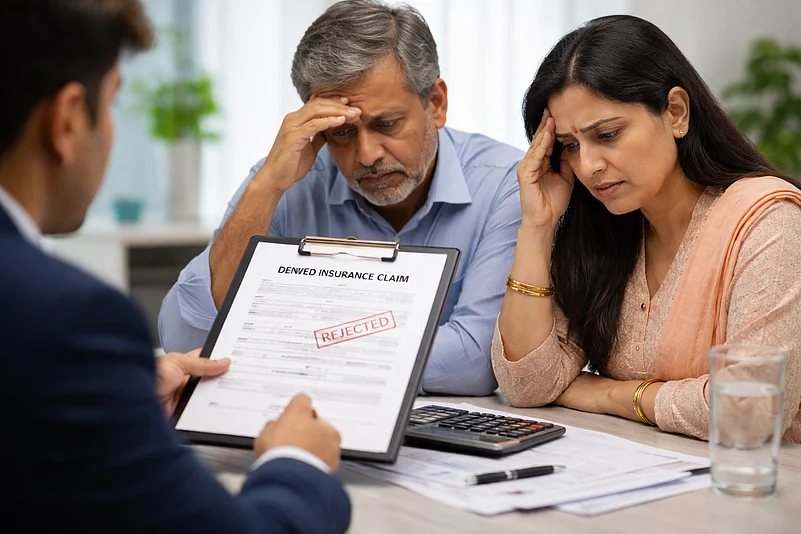

A life insurance claim worth Rs 25 lakh has been rejected after the National Consumer Disputes Redressal Commission (NCDRC) found that the policyholder had not disclosed a serious illness at the time of purchase, according to a recent report by The Indian Express. The commission set aside an earlier consumer forum order that had asked the insurer to pay the insured amount, stressing that concealment of major health conditions can invalidate an insurance contract.

The case emerged after the death of a policyholder whose nominee sought payment under a life insurance cover of Rs 25 lakh. The insurer declined the claim, citing suppression of a pre-existing disease at the proposal stage. The nominee challenged the rejection before a consumer commission and initially received a favourable ruling, but the insurer appealed, leading to a fresh examination of the facts by the national commission.

1 June 2026

Get the latest issue of Outlook Money

Why Disclosure Matters In Insurance Policies

Insurance largely runs on what the applicant states at the time of buying a policy. When a person applies for life insurance, the proposal form becomes the insurer’s main reference point. Details about past illnesses, treatments, or any ongoing health concerns usually shape the decision on whether the policy will be issued and at what cost.

In this case, medical records indicated that the insured had already been diagnosed with a serious cancer condition before buying the policy, but that diagnosis was not reflected in the information provided in the proposal form

The commission treated this as a significant omission rather than a minor lapse.

The order underlined that insurers base underwriting decisions on the information available at the outset. If important health details are left out, insurers may later refuse a claim on the grounds that the policy was issued without a full understanding of the risk involved.

Appeal Changed Earlier Consumer Forum Decision

At first, a consumer forum had asked the insurer to settle the claim, including the insured amount, interest, and a small compensation component. For the nominee, that order offered some immediate relief before the matter moved further in appeal.

However, the insurer contested the order, placing medical documents before the NCDRC to show that the illness existed prior to policy purchase. After reviewing the records, the national commission concluded that the omission was significant enough to affect the validity of the policy. It therefore overturned the earlier award and dismissed the complaint.

The commission also clarified that the cause of death is not the only factor in such disputes. What matters equally is whether relevant health information was truthfully shared when the policy was taken.

Key Takeaways For Policyholders

The order is a reminder for anyone planning to buy insurance: fill the proposal form carefully and disclose health details as clearly as possible, whether it’s an illness, treatment, test, or hospital visit. Something that feels minor today can turn into a sticking point later if it hasn’t been mentioned.

Many advisers say it’s wiser to disclose more rather than less. Sharing details clearly at the start can reduce the chances of disagreements later, especially when a claim is filed, and families are already coping with emotional and financial strain.

Insurance, after all, depends on both sides being upfront, the insurer in offering terms and the policyholder in stating facts accurately. Getting those basics right from the beginning can go a long way in ensuring claims don’t run into trouble later.