Summary of this article

Indians today are renting for longer periods not just because purchasing property has become costlier but because they see value in renting as it provides them with the flexibility and lifestyle they seek.

Approximately 1.3 lakh crore is completely kept away from active personal investments, stock markets, and retail consumer spending of a tenant.

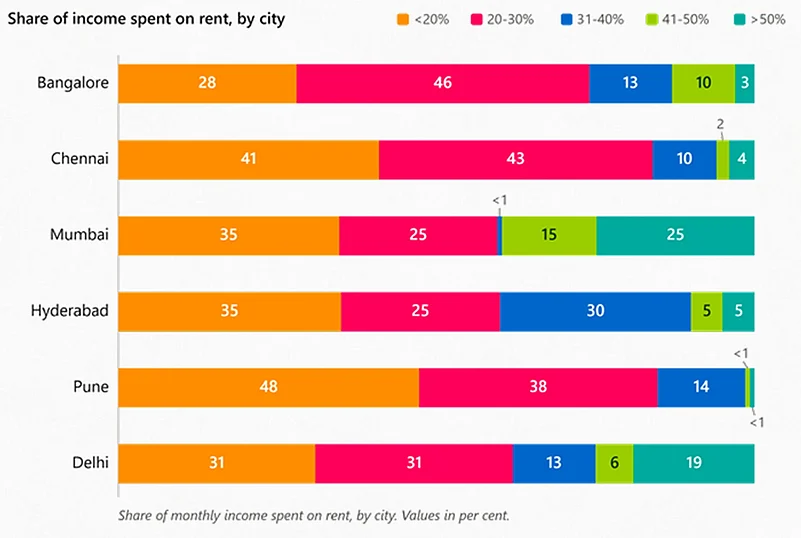

Rent is the single largest line item in most urban tenants' monthly budgets, and for nearly half of them it consumes more than 30 per cent of their monthly income.

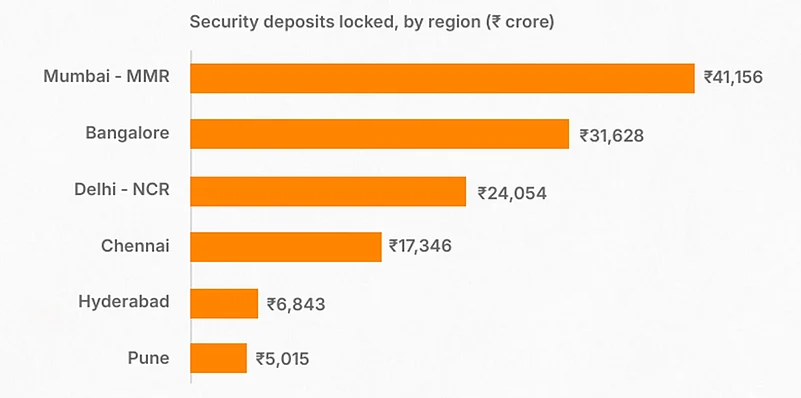

India’s rental market is evolving in interesting ways. For many urban Indians, renting has long ceased to be just a stepping stone before buying their own home and has emerged as a long-term housing option because of high property prices and ever-increasing gaps between home loan EMIs and monthly rents. However, high security deposits are also eating into tenant wallets. Together, tenants across India’s six major metros now hold over Rs 1.26 lakh crore of security deposits, NoBroker’s Rent Report 2026 reveals. This clearly shows affordability concerns don’t stop at looking at rents alone.

Saurabh Garg, co-founder & chief business officer, NoBroker, says, “Renting has changed quite drastically over the last few years. On one hand, technology has simplified the entire experience of searching, shortlisting and moving into your dream home. But on the other hand, the market has seen a much larger, fundamental change.”

“Indians today are renting for longer periods not just because purchasing property has become costlier but because they see value in renting as it provides them with the flexibility and lifestyle they seek. Additionally, renting has become more of a need than a choice for a large population with home loan EMIs and monthly rents diverging further apart,” he adds.

India’s Great Security Deposit Squeeze

The Rs 1.3 Lakh Crore Deadweight: While monthly rent gets all the attention in personal finance conversations, the upfront financial bandwidth required just to secure a house is creating a massive liquidity vacuum. Indian tenants currently have a staggering Rs 1,26,042 crore locked up with property owners in security deposits across top 6 metros. To put that into perspective, this trapped capital is larger than the annual infrastructure budgets of several Indian states.

Approximately 1.3 lakh crore is completely kept away from active personal investments, stock markets, and retail consumer spending of a tenant. The country's premier commercial and tech hubs command the top share of this locked wealth. The Mumbai Metropolitan Region (MMR) occupies the top position because of the high rentals and Bangalore due to high upfront customary deposit.

Key Trends and Overview:

Half Their Paycheck to Rent: The Forced Tenants of the Big Metros

Rent is the single largest line item in most urban tenants' monthly budgets, and for nearly half of them it consumes more than 30 per cent of their monthly income. The weight of that burden, however, is distributed very unevenly across cities.

Mumbai and Delhi stand out as the places where tenants carry the heaviest load. In Mumbai, a striking 25 per cent of tenants carry the heaviest load and spend more than half their income on rent, with another 15 per cent in the 41–50 per cent band, meaning roughly four in ten Mumbai tenants direct over 40 per cent of their earnings toward housing.

Coming next is the National Capital Region (NCR) with 19 per cent spending more than 50 per cent and another 25 per cent spending more than 40 per cent. Bangalore looks significantly healthier. The highest chunk of Bangalore tenants – 46 per cent - spend between the somewhat reasonable bracket of 20-30 per cent. Only 13 per cent spend over 40 per cent. Despite being called an expensive metro, Bangalore isn’t making citizens spend as high a percentage of their incomes on rent as Mumbai and Delhi are.

Tenant by Choice: When Renting Becomes a Decision, Not a Compromise

Running alongside the forced tenant is a very different and fast-growing group: people who can comfortably afford to buy and are deliberately choosing not to. For them, flexibility, mobility, and lifestyle freedom now outweigh the traditional pull of ownership. Homeownership has long been treated as the definitive signal of stability, but a meaningful segment of today's tenants is rejecting that assumption outright, and 46 per cent of tenants now say they prefer to rent over the long term.

The pattern is clearest among working-age professionals. It peaks in the 25 to 34 band, where 53 per cent prefer to rent long term, and stays high at 48 per cent among those aged 35 to 44. From there the preference falls away steadily with age, easing to 33 per cent in the 45 to 54 band and to just 24 per cent among tenants aged 55 and above, where the conventional aspiration toward ownership still holds firmest. The takeaway for the market is clear: a large share of renting demand is now durable and intentional, not a waiting room for eventual purchase.

Gen Z Churns 1.5x Faster

Tenant behaviour is changing as fast as tenant demographics. Gen Z tenants switch homes roughly 1.5 times more often than older cohorts, compressing the rental cycle in a way that landlords are still adjusting to. Among tenants aged 18–24, 30 per cent move every six to twelve months, against around 10 per cent of those aged 35 and above. As tenants get older, stability returns: the majority of those over 55 stay put for more than three years at a stretch.

The City That Ate Its Own Middle Class

Nowhere is the affordability squeeze more visible than in the Mumbai city. Asking rents in the island city have hardened well beyond middle-class reach, with South Mumbai average near Rs 90,000, Powai around Rs 63,000, and Andheri West close to Rs 50,000, even as these pockets add almost no new stock; Powai's supply has grown barely 4 per cent a year.

The affordable volume has decisively shifted to the edges. Thane West is now the single largest rental market in the region and sits among the fastest-growing in supply, alongside Kalyan (both at 26 per cent), Virar at 24 per cent, Taloja at 23 per cent, and Dombivli at 19 per cent year on year, with average rents between Rs 14,000 and Rs 35,000. Navi Mumbai tells the same story, with Airoli and Kharghar as the top micro-markets with the supply of each of these rising 17 per cent annually. The result is a core that grows ever more expensive and static, ringed by a periphery absorbing every household priced out of it. The gap between core and edge rents for a 2BHK has widened from about Rs 28,000 a month in 2017 to Rs 58,000 today. Mumbai's middle class was quietly pushed out to Thane, Navi Mumbai, and Vasai.

Priced Out:

The Steep Rent Curve of India

The physical distance between home and the office for an Indian tech worker is entirely dictated by the local rent curve. And right now, that curve is steeper than ever. In cities like Bengaluru and Hyderabad, the distribution of affordable housing has fundamentally broken. The areas immediately surrounding the major tech parks, places like Bellandur or Gachibowli, have seen unprecedented rent inflation, transforming into high-end residential hubs. Meanwhile, the entry-level salaries for most freshers working in those exact tech parks have remained more or less frozen for over a decade. The result is a massive rent disparity that dictates where talent can survive. Because the rent in localities closer to tech/business parks is mathematically impossible for a fresher to afford, they are forced to chase the rent curve outward until prices drop.

Smaller Units, Bigger Yields

Investor economics in the rental market are tilting decisively toward compact formats. At the same building and society level, 1BHKs and studios quietly deliver higher rental yields than larger configurations in every city measured. Bangalore at 4.8 per cent and Hyderabad at 4.6 per cent, while the yield curve falls steadily as unit size grows, dropping below 3 per cent for most 4BHKs. The logic is straightforward: smaller units command proportionally higher rent per square foot. For investors weighing where to deploy capital in the rental market, the message is clear. The smallest homes are increasingly the most efficient, and the premium ones attached to size no longer translate into superior returns.