Summary of this article

Insurance is a contract. The cover may be available, but there are certain steps that need to be followed for the claim to move smoothly.

In health insurance, emergency hospitalisation typically requires the insurer to be informed within a specified time window. In motor insurance, accidents and vehicle damage should also be reported promptly.

Reimbursement claims require policyholders to pay first, collect documents, submit claims, and wait for settlement. That process naturally takes longer.

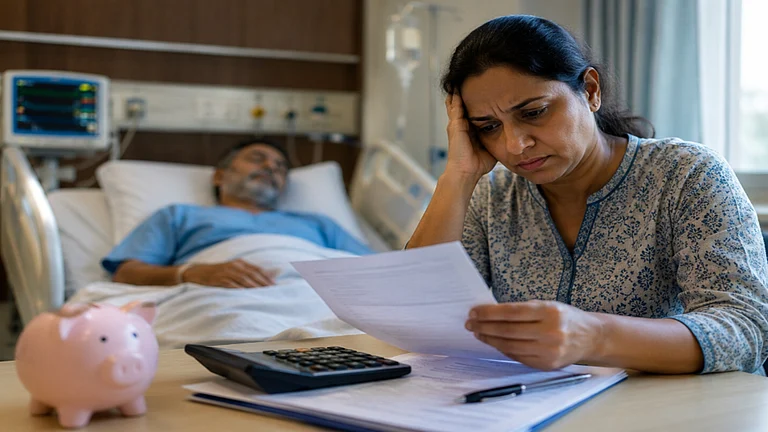

Most people think buying insurance is the tough part. In reality, the real test comes when you need to make a claim.

Mohan discovered this after a routine appendix surgery. His health insurance policy was active, the treatment was covered, and all premiums had been paid on time. Yet his claim took nearly three months to settle. The reason wasn’t a rejection. It wasn’t even a dispute.

It was paperwork, timelines, and process.

“Many customers assume that once they buy a policy, the claims process is automatic. But insurance is a contract. The cover may be available, but there are certain steps that need to be followed for the claim to move smoothly,” says Venkatesh Naidu, CEO, Bajaj Capital Insurance Broking.

Incidentally, that’s where many policyholders unknowingly make mistakes.

The Most Common Reason Claims Get Stuck

According to industry experts, most claim delays are not caused by insurers refusing to pay. They are caused by missing information, delayed intimation, incomplete documents, or procedural gaps. Something as simple as informing the insurer late can slow down a claim. In health insurance, emergency hospitalisation typically requires the insurer to be informed within a specified time window. In motor insurance, accidents and vehicle damage should also be reported promptly.

“The sooner the insurer is informed, the smoother the process becomes. Delays in intimation often create additional verification requirements that could have been avoided,” says Naidu.

The same applies to documentation. Mismatching names, missing hospital records, incomplete bills or wrong bank details can lead to rounds of clarifications, stretching timelines by miles.

Why Cashless Matters More Than People Realise

One of the biggest mistakes policyholders make is not checking whether their preferred hospital or garage (in case of car insurance) is part of the insurer’s network. Cashless claims are designed to simplify the process. The insurer settles approved expenses directly with the hospital or garage, reducing paperwork and out-of-pocket costs.

“When customers use network hospitals or network garages, the claim journey is generally much smoother. The ecosystem is already integrated, which reduces delays and administrative friction,” adds Naidu.

Reimbursement claims, on the other hand, require policyholders to pay first, collect the documents, submit claims, and wait for settlement. That process naturally takes longer.

Motor Insurance Has Its Own Set of Rules

Motor claims often get delayed because vehicle owners rush to repair damage before completing the insurer’s inspection process. After an accident, insurers typically appoint a surveyor to assess the damage before repairs begin.

“Many customers act with good intentions and immediately send the vehicle for repairs. But if the inspection process is not completed first, complications can arise during claim settlement,” says Naidu.

The photographs of the car after the accident, claim intimation, surveyor assessment and proper documentation play an important role in ensuring a smooth claim experience.

The Real Gap Is Awareness

The insurance industry has become significantly digitized over the last few years. Buying a policy today takes minutes. Understanding how to use it often takes much longer.

“People spend time comparing premiums, but very little time understanding the claims process. The irony is that the claimed experience is ultimately what determines whether the policy delivers value,” says Naidu.

This is particularly important because a claim usually arrives during a stressful moment – an accident, a hospitalisation, or an unexpected emergency.

That is not the ideal time to start reading policy documents.

A Few Minutes Today Can Save Weeks Later

Policyholders review a few basics long before they need to make a claim:

To start with, save the insurer’s helpline number as well as the broker’s number. The broker is usually the first point of contact. Check whether your preferred hospital or garage is part of the network. Understand claim intimation timelines. Keep policy documents accessible, and lastly, review key exclusions and waiting periods.

“Insurance works best when customers understand the process before they need to use it. A small amount of preparation can prevent a great deal of frustration later,” says Naidu.

That’s because in insurance, the difference between a smooth claim and a delayed one is often not the policy itself, but in knowing what to do when the moment arrives.

FAQs

1. What are the most common reasons for delays in insurance claims processing?

Failure to inform the insurer on time, not having all supporting documents ready, missing records, and providing inaccurate information to the insurer are some of the common reasons for delays in insurance claims processing.

2. Why are cashless claims settled at a faster pace than claims reimbursed directly to policyholders?

Cashless claims are processed by hospitals or garages that are a part of insurer’s panel. Hence, the settlement is made directly by them, with minimum paperwork from your end.

3. What are some steps policyholders can take for a hassle-free claims experience?

Intimating the insurer at the earliest, storing all necessary documents, understanding the claim process and timelines, checking network of hospitals/garages are some of the steps you can take.