Here is something most investors discover too late. The strategy that made money last year is rarely the one that makes money this year. Momentum runs hot in a bull market, then stumbles. Value sits ignored for years, then suddenly everyone wants it. Quality gets overlooked when greed takes over, then becomes the only safe harbour when things go wrong.

This rotation is not random. It is predictable in hindsight, and almost impossible to time in real life. Which is exactly why betting on a single factor is a risk most investors do not realise they are taking.

Factors and their characteristics

1 June 2026

Get the latest issue of Outlook Money

There are four factors that drive equity returns over time, each with its own logic and its own season.

Value seeks out stocks the market has priced too cheap relative to what they are actually worth. Tools like PE, price-to-book, dividend yield and EV/EBITDA ratios help separate genuine bargains from value traps. This factor tends to reward patience during recoveries. It can test that patience during prolonged downturns.

Quality is about owning well-run businesses. Companies with low debt, high return on equity, strong return on capital employed and consistent earnings growth. In rough markets, quality tends to fall less. In raging bull markets, it can lag behind flashier picks.

Low volatility targets stocks with steadier price movements, usually filtered by standard deviation over the past 12 months. Investors here are not chasing the biggest returns. They are protecting what they have built, especially when markets correct sharply.

Momentum does exactly what it sounds like. It backs what is already working, based on six and 12-month price performance. In a trending market, few strategies outperform momentum. When the trend breaks, losses can come just as fast.

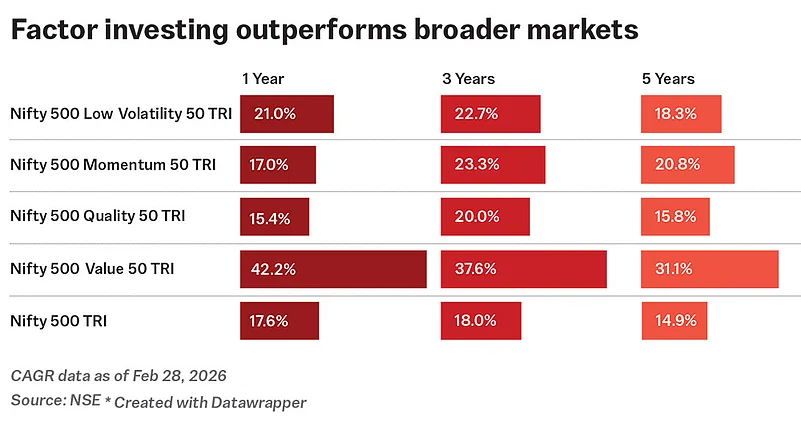

Outperforming broader markets

Between 2010 and 2025, the annual top performer kept changing. Momentum led in seven of those 16 years. Value topped in four. Low volatility in three. Quality in two.

Yet despite the rotation, all four factor indices consistently beat the broader market. Over three years, the outperformance over Nifty 500 TRI ranged from 2 to nearly 20 percentage points. Over five years, from 1 to 16 percentage points.

No one factor owns the podium for long. But together, blended through a rigorous quant model with defined rules for sector and stock allocation, they create something more durable than any single style can offer. Add AI and machine learning for continuous refinement, and the portfolio becomes genuinely adaptive.

For retail investors, this is accessible through factor and quant-based mutual funds. No prediction required. Just process, patience and the discipline to let all four factors do their work.

Disclaimer: This article is written by Shivam Kaura of The Alpha Capitalist. The views expressed are their own. This is partner content and not an Outlook Money editorial feature. Outlook Money does not provide investment advice or endorse any products or services mentioned.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

Disclaimer: The Views are Personal and not a part of the Outlook Money Editorial Feature