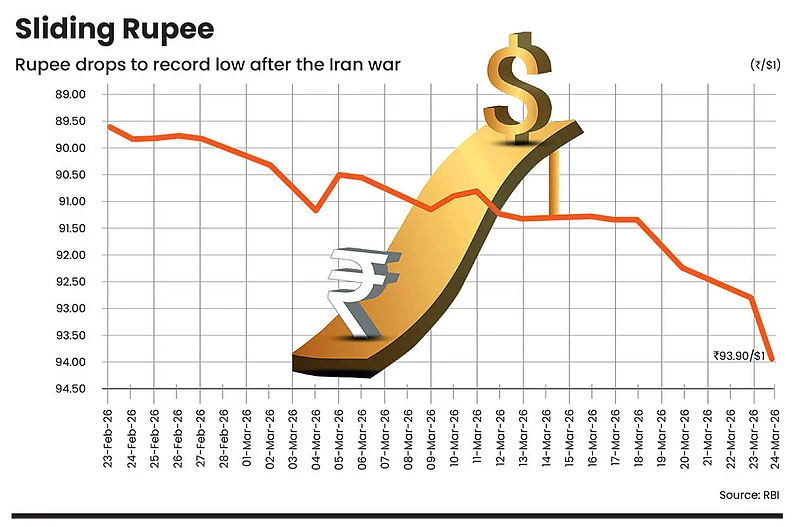

The war involving the US, Israel and Iran in the Middle East, which may be moving towards a ceasefire with the US and Iran negotiating a deal till the filing of this report, triggered one of the most severe geopolitical shocks in recent years for global markets and economies. Oil prices soared, currencies tumbled, and equity markets went into a tizzy. The benchmark index tumbled 9 per cent, crude oil jumped over $100 per barrel, and the rupee touched an all-time low of Rs 93.90 against the US dollar, as on March 24, 2026.

High crude prices have set off a chain reaction across asset classes. For a country like India, which imports around 85 per cent of its crude oil requirement, the ripple effects are immediate and deep. Families and small businesses are struggling to access LPG cylinders, while heightened market volatility and eroding portfolios have left investors in a state of panic and indecision.

The benchmark indices are swinging sharply. What lifts the market one day is countered by deep selling the next, causing uncertainty. For instance, when US President Donald Trump issued a 48-hour ultimatum to Iran on March 23 to clear the key global shipping route, the Strait of Hormuz, markets reacted sharply. The announcement heightened fears of further escalation and disruption in global oil supplies, and the markets reacted negatively to the news. The benchmark indices across the globe witnessed a steep fall as investor sentiment turned risk averse. The Nifty index closed around 2.60 per cent lower on that day. But on the very next day, March 24, markets rebounded after Trump claimed he had productive talks with Iran and announced a five-day pause on military strikes.

1 July 2026

Get the latest issue of Outlook Money

In such a scenario, the billion-dollar questions in the minds of market investors is how long will this volatility continue and what they should do. But first let’s understand the crux of the problem.

Crude Reality

At the heart of the economic disruption is oil. As on March 24, the brent crude price was hovering in the range of $100-105 per barrel in the international market. However, the actual price for India is much higher, considering transportation and other logistics cost. According to Petroleum Planning and Analysis Cell data, the International prices for crude oil (Indian Basket) is $123.15 per barrel in March, almost double compared to the $69.01 per barrel in February 2026.

Higher crude oil prices have a direct and widespread impact on India’s economy. Since India imports around 85 per cent of its oil, any price rise increases the country’s import bill, weakens the rupee, and fuels inflation. This raises the costs for transport, and manufacturing, which eventually makes everyday goods more expensive.

India imports 85% of its crude oil needs, and the ripple effects of high prices have been deep

At a macro level, it widens the current account deficit and pressures government finances, while impacting corporate margins and stock market sentiment.

A Morgan Stanley report released on March 11, 2026, says: “A sustained rise in oil prices could push Asia’s energy burden above its 10-year average. However, beyond higher prices, the greater concern is the risk of supply disruptions—particularly in liquefied natural gas (LNG), where volumes could be curtailed. India, Thailand, South Korea, and Taiwan are among the most exposed economies on this front.”

According to various reports, around 55-65 per cent of India’s LNG imports transit through the Strait of Hormuz, with Qatar (which is in the line of fire) alone accounting for nearly 40 per cent of the country’s LNG supplies. There are limited short-term alternatives, as sourcing LNG from the US, Australia, or Africa involves longer shipping times and constrained spot availability.

The strain is already visible on the ground. Gas shortages are affecting industrial consumers, as the government is prioritising supplies for essential sectors, such as households, hospitals, and fertilisers. Even within these priority segments, delays in LPG cylinder deliveries have been widely reported due to tight supply conditions.

Effect On Equities

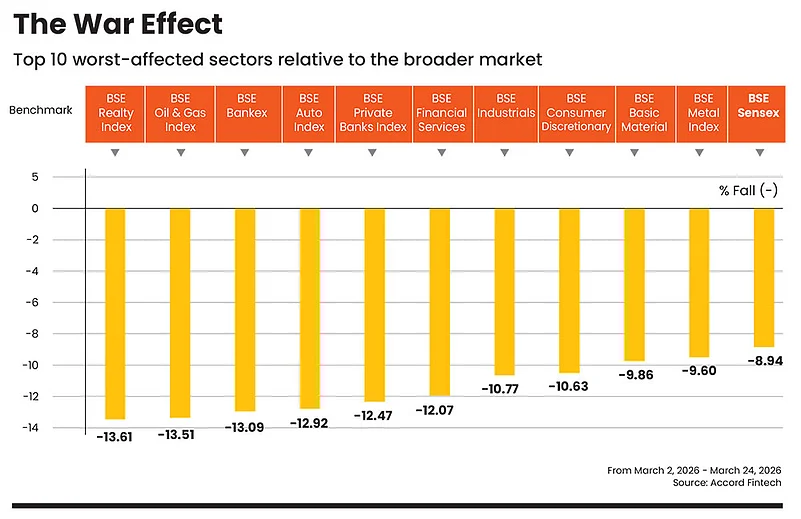

The ongoing geopolitical conflict has triggered a sharp and broad-based correction across sectors, with cyclical and rate-sensitive sectors bearing the brunt of the sell-off. Data shows that key indices such as the BSE Auto (-12.92 per cent), Bankex (-13.09 per cent), and Oil & Gas (-13.51 per cent) have fallen more than the broader market BSE Sensex, which fell nearly 9 per cent.

Broad-Based Fall: A closer look at market data suggests that the sell-off is not limited to oil-linked sectors alone; but far more broad-based. When we analysed the Nifty 500 index, we found that weakness was widespread. More than 195 stocks have corrected over 30 per cent from their 52-week high; around 141 stocks have declined 20-30 per cent; and 150 in the range of 5-20 per cent, month-to-date as on March 24, 2026.

Experts say that this fall is a result of negative sentiments and is not a fundamental problem.

Key indices, such as BSE Auto, Bankex and Oil & Gas, have fallen more than 12%, while the Sensex fell 9%

Says Shreyash Devalkar, head equity, Axis Mutual Fund: “Wars and geopolitical conflicts typically trigger short-term market turbulence. History shows that oil shocks alone have not derailed Indian equities unless they persist long enough to hurt growth and monetary stability. During the Russia-Ukraine war in 2022, for instance, Brent crude surged above $100 per barrel. Yet, after an initial sell-off, the Nifty 50 ended the year in the positive territory.”

Banking Sector: The sharp fall in banking and financial services indices are due to fears of margin compression and potential stress on credit growth in a high-inflation environment.

The Gulf region contributes more than one-third of total remittance inflows. Says Pankaj Pandey, head-research, ICICI Securities: “A prolonged conflict that slows economic activity in the Gulf could weaken these inflows, impacting system-wide liquidity and banks with high dependence on non-resident Indian (NRI) deposits.”

Some banks may face challenges in terms of increased volatility in NRI inflows which can result in repricing of liabilities amid liquidity challenge on the domestic front, he adds. For families with children studying abroad, the depreciating rupee is playing spoilsport (see Time To Recalibrate Remittance Strategy For Kids Abroad).

Export-Oriented Sectors: On the other side, export-oriented sectors are likely to drag down the asset quality of banks if the conflict continues for long. Banks and non-banking financial companies (NBFCs), with exposure to borrowers in the gems and jewellery, engineering, and agri-product sectors remain vulnerable in terms of asset quality. Six Gulf Cooperation Council (GCC) countries—Saudi Arabia, the UAE, Qatar, Kuwait, Oman and Bahrain—account for around 17 per cent of India’s total merchandise export.

Effect On Gold

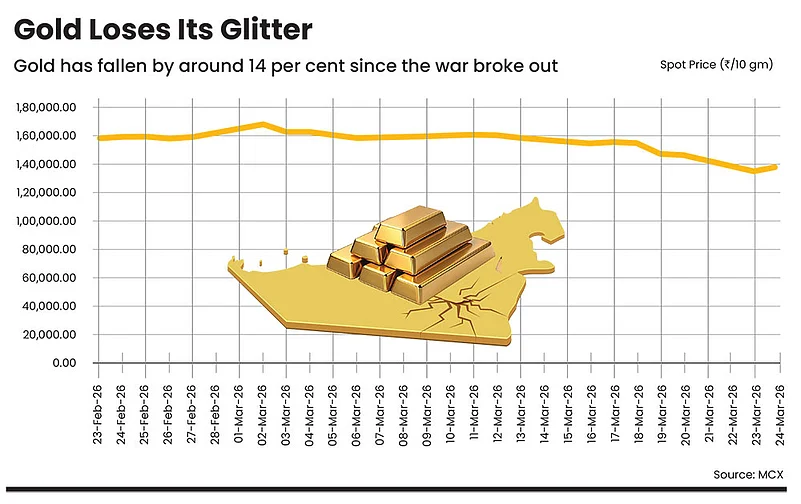

The recent fall in gold, which is traditionally seen as a safe haven asset, is a striking market paradox. Typically, the current situation—a full-blown geopolitical shock, tensions around Iran, risks to the Strait of Hormuz, oil around $100 per barrel, and equities under pressure—would favour gold, yet the metal has dropped sharply. Gold has tumbled around 14 per cent since the start of the war.

Right now, gold is caught in a rare convergence of forced selling, tighter monetary expectations, a firm dollar, and weak physical demand.

One of the explanations lies in the collision between fear and liquidity. Says Chirag Mehta, chief investment officer, Quantum Mutual Fund: “In risk-off phases, investors don’t sell what they want, they sell what they can. Gold, being highly liquid becomes the first source of cash. Margin calls and leveraged positions have triggered forced selling, turning gold into a funding tool rather than a refuge,” he adds.

Markets that were expecting rate cuts are now bracing for a tighter policy. Typically, higher bond yields and a stronger dollar create pressure on gold. Says Mehta: “Physical demand from key markets such as India, the Middle East and China has softened due to high prices and economic uncertainty, removing a key support base. At the same time, crowded positioning after last year’s rally has led to sharper unwinding as investors liquidate profitable holdings to cover losses elsewhere.”

Another factor that hit gold prices is the fading de-dollarisation narrative that was one of the drivers of its rally through 2024-25. Central bank diversification and reserve accumulation have not disappeared, but they have taken a backseat amid elevated gold prices, combined with a firmer dollar, which had made the metal relatively inexpensive. “The dollar’s strength is being driven by a mix of demand, elevated oil prices, and rising inflation expectations, factors that are reinforcing a hawkish stance from the US Federal Reserve,” says Mehta.

Will Volatility Continue?

No market expert has a clear answer to that question. In the current environment, uncertainty remains the only constant. Markets are reacting to every headline, often swinging sharply on news flow rather than fundamentals. At the start of the war, Trump indicated it could last 3-4 weeks. Now in the fourth week, uncertainty continues with no clear timeline in sight.

Says Sunil Singhania, founder of Abakkus Asset Manager: “It’s a complex situation. There is hope that no country can afford a prolonged conflict of this scale. The impact is not limited to one region, but is being felt across the world. That is why several European and other global economies have already called for an urgent de-escalation. I am hopeful we will start to see some de-escalation very soon.” We hope that if de-escalation happens, the bounceback will be pretty sharp, he adds.

Singhania believes that investors should expect the direction of the market to be positive on account of fairly decent earnings momentum expected from corporate India.

What Should You Do?

A war situation triggers a classic risk-off environment. Equity markets become volatile, currencies weaken (especially in emerging markets like India), and commodities—particularly oil and gold—see sharp moves. In such phases, investors globally tend to shift money into perceived safe haven assets. This leads to strengthening of the US dollar, more pressure on equities, and heightened fluctuations across asset classes.

War-driven volatility often creates both risk and opportunity, depending on how portfolios are positioned

However, not all sectors or instruments react the same way. War-driven volatility often creates both risk and opportunity, depending on how portfolios are positioned.

For investors, the instinct to react quickly is natural, but history shows that a disciplined strategy beats emotional decisions during wartime market turbulence.

Avoid Panic Selling: The first rule of investing during a war is simple: do not panic. Market corrections during geopolitical crises are often sharp, but temporary. Historical events from the Gulf War to more recent conflicts have shown that markets tend to stabilise once uncertainty begins to fade.

Selling in panic locks in losses, which often results in the investors missing the recovery rally. “If the market is in a bad shape and you also become scared, then it is a lethal combination. The situation will get worse,” says Raamdeo Agrawal, chairman and co-founder of Motilal Oswal Financial Services. When markets are fearful, you have to be greedy; even if you can’t buy, you should not lose your patience, he adds.

During 2020, when markets corrected sharply amid the Covid-19 outbreak, many investors panicked and exited equities, fearing deeper losses. However, this reaction proved costly. As unprecedented global stimulus and liquidity measures kicked in, markets rebounded much faster than expected. Those who stayed invested—or used the correction to accumulate—benefited from one of the strongest rallies in recent history. In contrast, investors who exited during the fall missed the recovery and struggled to re-enter at higher levels.

Selling in panic locks in losses, and investors miss the recovery rally, which was seen in 2020

Stay Invested: Don’t sell or discontinue your systematic investment plans (SIPs), especially if you are investing for long-term goals. If you discontinue your financial journey mid-way, either you will have to push your goal further or will have to compromise. SIPs enable rupee-cost averaging, so they work best in volatile market conditions as you accumulate more number of units at lower net asset value (NAV) when the market is low, and fewer units when the market is high.

Over the past 26 years, the average market correction has been around 18.37 per cent, with the steepest fall of 59.86 per cent witnessed during the 2008 financial crisis. Despite these sharp drawdowns, equities have delivered an average return of 12.64 per cent over the same period. Volatility and corrections are part of the journey, but those who stay invested through cycles are more likely to benefit from the compounding potential of equities.

Use Gold as a Strategic Hedge: Experts believe gold may remain under pressure in the near term as markets expect interest rates to stay higher for longer. Besides, factors such as persistent inflation, high energy prices, and strong dollar are likely to keep prices subdued. The recent weakness is largely driven by liquidity conditions and does not change gold’s long-term appeal.

Structural drivers, such as rising fiscal spending and increasing geopolitical tensions continue to support the metal. The key shift is in valuation—gold is now available at more attractive levels. Instead of trying to time the market, experts suggest a staggered investment approach, particularly through gold exchange-traded funds (ETFs).

Despite short-term volatility, gold continues to act as a portfolio stabiliser during uncertain times. Says Mehta: “Waiting for perfect clarity may mean missing the opportunity, while gradual accumulation remains the more prudent strategy.”

Don’t Wait For The Bottom, Stagger Investments: Agrawal cautions investors against waiting for the absolute bottom, as timing the market is nearly impossible, even in a well-corrected phase.

In times of heightened market volatility, a staggered investment approach can help investors ride volatility with greater discipline. Instead of deploying a lump sum at one go, you should spread investments over a period of time. This strategy becomes particularly relevant when markets are swinging sharply due to geopolitical tensions. This way your purchase cost gets averaged out across market cycles.

Gold may remain under pressure in the near term as markets expect interest rates to stay high for longer

Singhania suggests investors to deploy 20-30 per cent of investible surplus now and the rest according to the market conditions.

Scout For Value Opportunities: Certain pockets in the market have corrected significantly in the last few months and offer good investment opportunities.

Singhania gives the example of small- and mid-cap stocks, which are down 20-30 per cent from their all-time highs. “Their valuations have become more reasonable, providing an opportune entry point,” he says.

Also, in the stock market, price and value are often mistaken as the same, but they are fundamentally different. Price is what the market is willing to pay for a stock at any given moment, driven by sentiment, news, and short-term factors. Value, on the other hand, is the intrinsic worth of a company based on its earnings, growth potential, and fundamentals.

Agrawal explains this through the example of the Nifty 50. Just a few months ago, the index was hovering around 26,000, and has since corrected to around 23,000. However, this decline does not necessarily imply a proportional erosion in underlying business value. “The key question for investors is whether prices have now moved closer to intrinsic value. If a stock worth `100 is now trading near or below that level, it may present an opportunity,” he adds.

For long-term investors, the most reliable strategy is to stay invested, diversify, and add during correction

Look Beyond Boundaries: One of the most immediate impact of a war is strengthening of the US dollar and weakening of the rupee. A weaker rupee can be a double-edged sword. On one hand, export-oriented sectors, such as IT and pharmaceuticals tend to benefit, as their dollar earnings translate into higher revenues in rupee terms. On the other hand, import-heavy sectors, such as oil, aviation, and chemicals face rising input costs. This puts pressure on the margins.

Allocating a portion of the portfolio in to international funds can act as a natural hedge against currency volatility. It not only provides exposure to global growth opportunities, but also helps cushion the impact of a weakening rupee.

In an interconnected world, looking beyond boundaries is no longer optional, it is essential.

Says Devalkar: “The current conflict is a serious geopolitical development, but not unprecedented for Indian investors. Over the past 15 years, nearly every major conflict has tested the market sentiment, yet Indian equities have repeatedly demonstrated resilience. Markets may correct, currencies may weaken, and oil prices may spike, but fundamentals tend to reassert themselves over time.”

For long-term investors, the most reliable strategy remains unchanged: stay invested, diversify prudently, and use periods of correction to gradually add to existing investments.

kundan@outlookindia.com