The new financial year rarely announces itself with fanfare, but for salaried individuals and taxpayers, April 1 quietly marks one of the most important checkpoints of the year. It is the time to reset, reassess, and realign finances before the demands of the year ahead takes over.

Financial year 2026-27 (FY27), however, acquires special significance with the new Income-tax Act, 2025, coming into effect, and the new tax regime (NTR) pulling its weight over the old one (OTR).

For decades Indians have been investing in products that offer tax deductions. The NTR has changed that with the income tax slab rates tipping the scales in its favour for most salary brackets. It may be noted that the NTR has done away with popular deductions available under OTR under Section 80C, 80D and others that helped individuals save tax. Apart from standard deduction, there are only a few others that are relevant to all under the NTR.

1 July 2026

Get the latest issue of Outlook Money

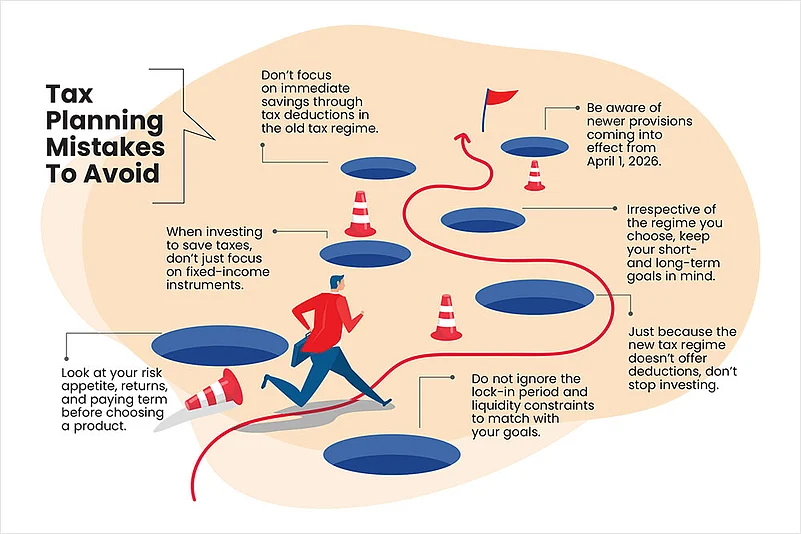

One positive that has emerged though is that individuals need to align their investments not just to reduce their tax outgo, but to holistic financial planning, involving their own goals and risk appetite. So what should your strategy be this year?

Planning Matters

Reviewing income streams, reassessing goals, and making an informed choice of the tax regime at the outset can help strike the right balance between tax efficiency and wealth creation.

Says Aarti Raote, partner, Deloitte India: “It is always advisable for taxpayers to plan their taxes well in advance rather than resort to last-minute decisions. The first step in this process is choosing the right tax regime. This requires estimating, with reasonable accuracy, expected income streams, expenses, and investment commitments for the year, and then comparing the tax outgo under both the regimes.”

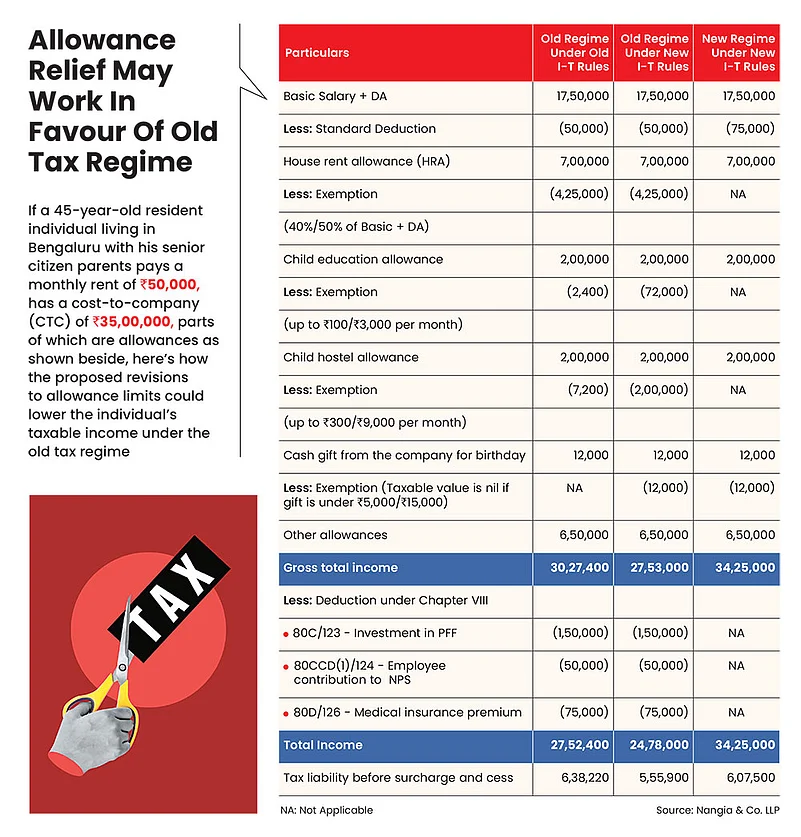

Taxpayers should also factor in potential future decisions, such as the purchase of residential property, investments in insurance, or allocations to long-term financial instruments. Additionally, changes in income tax rules, such as revisions in perquisite taxation effective April 1, 2026, and the availability of exemptions should be carefully evaluated (see Allowance Relief May Work In Favour Of Old Tax Regime).

Old Tax Regime: For taxpayers who continue with OTR, Section 80C remains one of the most valuable tools for reducing taxable income and building wealth.

Apart from providing deductions on instruments, such as the Employees’ Provident Fund (EPF) and post office schemes, it also encourages equity investing through equity-linked savings schemes (ELSS), which are also eligible for a deduction up to Rs 1.50 lakh. Among tax-saving investment options, ELSS offers the shortest lock-in period of three years and has the potential to provide maximum growth.

Review income streams, reassess goals and choose the tax regime at the outset to strike the right balance between tax efficiency and wealth creation

Says Santosh Joseph, CEO, Germinate Investor Services, a boutique financial services outfit based in Bengaluru: “For those who remain in OTR, investing in equity-oriented mutual funds, such as ELSS is a meaningful way to make use of the Section 80C benefit. It provides tax advantage, while also giving investors an opportunity to participate in long-term wealth creation.”

Also, don’t ignore your overall financial plan while doing this. Adds Raote: “Effective tax planning isn’t just about where you invest, it’s about understanding the nature of the investment itself. This includes evaluating the level of risk, expected returns, the tenure involved, and whether the investment requires regular contributions over time. Each of these factors plays a crucial role in determining whether an instrument truly fits into your financial plan.”

Another common oversight is ignoring the lock-in period and liquidity constraints. “Investments made in a hurry to save tax often come with restrictions on withdrawal, which can affect liquidity in the years ahead. Similarly, taxpayers may underestimate how long they need to stay invested or whether they can sustain recurring commitments,” says Raote.

New Tax Regime: For a large number of taxpayers, the NTR has become the default choice because of its simplicity and ease of compliance. With fewer deductions to track and less paperwork to manage, it streamlines the tax process.

But this convenience begs a subtle shift in how individuals need to think about their money.

The NTR, with its limited scope for deductions, brings a sharper focus to financial decision-making. Nikunj Saraf, CEO, Choice Wealth, a wealth and financial services provider, points out that as more individuals move to the new tax regime, investing is slowly becoming what it was always meant to be, a tool for wealth creation.

Says Joseph: “Your investment decisions should focus on ensuring that your money beats inflation and grows meaningfully over time. A common misconception is that because the NTR does not offer traditional deductions, investing becomes less important. In reality, irrespective of the tax regime, investing in growth-oriented and inflation-beating assets remains essential for sound financial planning.”

Equities, in this context, take on a central role. “They are not without risk, as short-term volatility and market swings are part of the journey, but over longer time horizons, equities have consistently demonstrated their ability to create substantial wealth,” says Joseph. “Equity mutual funds, especially index and flexi-cap funds, should form the core for most investors, supported by some allocation to debt for stability and gold for diversification.”

What really makes the difference in wealth creation is time. For instance, if you are aiming to build a Rs 5 crore retirement corpus by the age of 60, the starting point can significantly shape the journey. At 30, you have the luxury of compounding working quietly in your favour. Even a monthly investment of Rs 15,000, growing at 12 per cent, can do the job, with an aggressive tilt towards equities. By 40, the window begins to narrow. “With about 20 years left, the required investment rises to roughly Rs 50,000-55,000 per month. The portfolio should still aim for growth, but with slightly more balance and risk management,” says Saraf.

At 50, time becomes the biggest constraint. To reach the same goal in 10-12 years, one may need to invest Rs 1.60 lakh-2.20 lakh per month, or rely partly on an existing corpus. At this stage, preserving capital becomes as important as generating returns.

Know The Changes

While the reforms under the new Income-tax Act, 2025, do not fundamentally alter how much tax one pays, they introduce a wide range of changes that will affect how one can claim exemptions, report income and interact with the tax system.

As such, one shouldn’t ignore the changes rolling in from April 1, 2026. “Making the most of these benefits requires staying updated on the changes in the income tax rules effective from April 1. Being aware of them and planning accordingly can help taxpayers fully utilise the reliefs available under the law,” she says.

For salaried taxpayers, the new framework could mean modest relief through updated exemption limits, but also greater scrutiny through improved data matching and documentation requirements.

Says Vishwas Panjiar, founder, SVAS Business Advisors LLP, a tax, M&A, regulatory, compliance and outsourcing, HR and CSR advisory firm. “The old rules had been patched and amended so many times over the decades that they had become genuinely difficult to navigate. The new rules attempt to present the same requirements in a structure that is logical and consistent with the layout of the new Act.”

The new Income-tax Act, 2025, does not alter how much tax one pays, but introduces changes that will affect how one can claim exemptions and report income

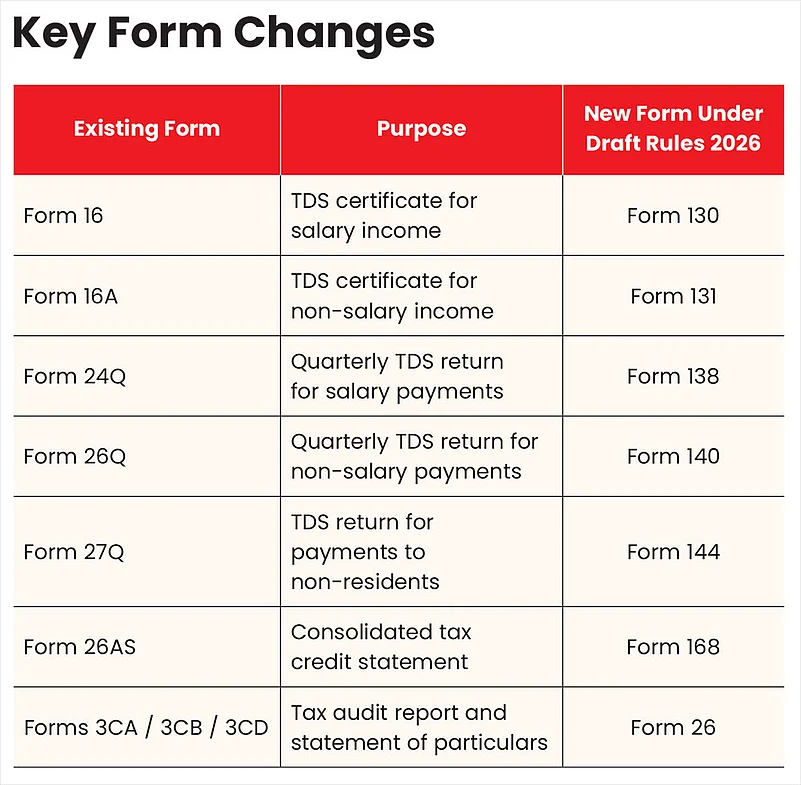

Disclosure Form Changes: The change that will probably catch people off guard first is the renumbering of familiar forms. For instance, the Form 16 you receive every year from your employer—the tax deducted at source (TDS) certificate—has been renamed Form 130. Form 16A, which covers TDS on interest, professional fees and similar non-salary income, is now Form 131. Form 26AS that taxpayers routinely download before filing returns will now appear as Form 168 (see Key Form Changes).

None of these changes how your salary is calculated or how your tax liability is arrived at. But since these forms sit at the heart of return filing, expect some initial confusion.

Says Panjiar: “The bottom line is straightforward: the form numbers will change, some procedures will be better organised, and the underlying machinery will be more digital. But if you are a salaried taxpayer who files honestly and on time, your annual experience of dealing with taxes is unlikely to feel dramatically different.”

New HRA Rules: The higher 50 per cent house rent allowance (HRA) exemption has historically been available only for the four original metro cities—Delhi, Mumbai, Kolkata and Chennai. But anyone living in the tech hubs of Bengaluru, Hyderabad, Pune and Ahmedabad would swear that the rental markets in these cities do not have “non-metro” rates anymore. For instance, in Bengaluru’s Whitefield area, rents can be upwards of Rs 40,000 per month for a two-bedroom flat. The draft rules propose to extend the 50 per cent limit to these four cities, a relief for many salaried professionals.

The draft rules also introduce greater transparency in rent reporting. Says Panjiar: “Taxpayers will now need to disclose their relationship with the landlord where annual rent exceeds Rs 1 lakh. This requirement is intended to bring more visibility to arrangements where rent is paid to parents or other family members. Such arrangements are perfectly legitimate, but they have often attracted scrutiny from the tax officials. The disclosure requirement makes it easier for the system to reconcile HRA claims with the rental income reported by the landlord.”

Documentation expectations are tightening too. The existing declaration format is proposed to be replaced with a revised disclosure form, which means rent agreements, payment records and bank transfers should be kept in order.

The tax system today matches information across filings more aggressively than most taxpayers realise. Says Panjiar: “If your rental arrangement is genuine and your paperwork is clean, this shouldn’t trouble you. If it isn’t, the new rules are a reasonable warning to sort that out before the system does it for you.”

Sumeet Hemkar, partner, Deloitte India, adds: “Going forward, the employer must obtain and verify HRA as part of their due diligence responsibilities before allowing the exemption. It is also essential to note that the HRA exemption remains exclusive to taxpayers opting for the old tax regime.”

Allowance Limits: The limits for many allowances and perquisites have been significantly increased. For instance, the children’s education allowance is proposed to increase from Rs 100 per month to Rs 3,000 per month per child, while the hostel allowance may increase from Rs 300 to Rs 9,000 per month per child. Similarly, valuation limits for employer-provided benefits, such as free meals and gifts have been enhanced from Rs 50 per meal to Rs 200 per meal, and from Rs 5,000 to Rs 15,000, respectively.

“The draft rules also revise thresholds for certain perquisites, including those relating to employer-provided motor cars and interest-free or concessional loans. These revisions seek to better align the valuation of such benefits with current economic realities, as many of these limits had remained unchanged for decades and had lost their practical relevance,” says Neeraj Agarwala, senior partner, Nangia & Co LLP, a CA firm.

The existing declaration format will be replaced with a revised disclosure form, which means rent agreements and payment records have to be kept in order

This could make the old regime more attractive (see Allowance Relief May Work In Favour Of Old Tax Regime). “Exemptions in respect of these allowances would be available only where such components form part of the cost-to-company (CTC) structure, so employees may need to engage with their employers to restructure their salary components,” says Agarwala.

PAN Card Requirements: The draft rules expand the situations in which taxpayers will need to quote their Permanent Account Number (PAN) for financial transactions. The goal is not subtle: the tax administration wants to ensure that high-value transactions across the economy can be reliably traced back to a real person.

Says Panjiar: “Banking is one area where the change will become concrete. PAN will be required where cash deposits or withdrawals across bank accounts aggregate to Rs 10 lakh or more in a financial year. For amounts of Rs 20 lakh or more, banks may also be required to electronically verify PAN, partly because incorrect or borrowed PAN numbers have historically been a way to obscure the origin of large cash flows.”

Real estate, predictably, remains a focus. PAN must be quoted for property transactions—purchase, sale, gift or development arrangements—where the value exceeds Rs 20 lakh.

Motor vehicle purchases will get pulled in too. PAN will be required where the transaction value exceeds Rs 5 lakh, bringing a much larger slice of vehicle sales into the reporting net.

On the hospitality and events side, cash payments exceeding Rs 1 lakh to hotels, restaurants, banquet halls or event managers will require PAN.

In insurance, the change is more structural. PAN will now be required at the time of buying a policy, and not just when premiums cross a certain figure. It is a small shift in timing, but a meaningful one in terms of when identity gets locked into the system.

The common thread is simple enough. “Whether you are depositing cash, buying a flat, upgrading your car or taking out an insurance policy, the system wants to know it is you. For most salaried taxpayers this is just paperwork, but for those who have relied on loose documentation for large transactions, the rules are making that difficult,” says Panjiar.

Changes In ITR Reporting: The draft rules do not really change how much tax you pay, but how closely the system expects you to explain and support what you report.

The distinction between the previous year and the assessment year has puzzled taxpayers for years; both have now been replaced with a single nomenclature, the “tax year”.

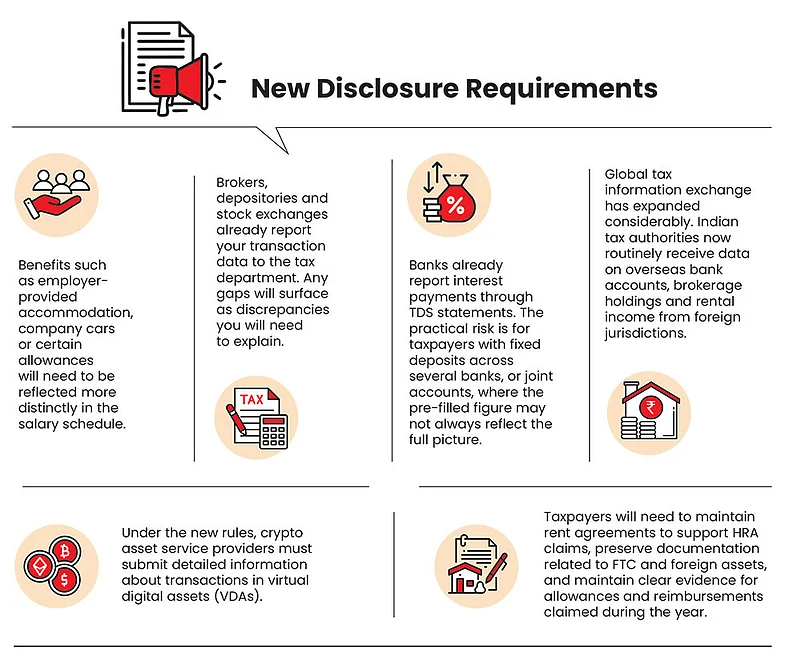

A more significant shift lies in how ITRs will be populated and checked. Says Panjiar: “Banks, brokerages, mutual funds and other financial intermediaries will be required to report more structured information directly to the tax authorities. As a result, an increasing portion of what appears in your return—interest income, securities transactions and certain investments—will show up pre-filled from third-party data. We have anyway progressively been moving in this direction over the past 4-5 years.”

Hemkar points out that the draft rules introduce notable refinements to the eligibility criteria for filing simplified return forms. A key proposal is the relaxation of conditions for filing ITR 1, which may soon be available to individuals owning up to two house properties against one previously, subject to prescribed conditions.

Individuals claiming deductions against income assessable under Income from Other Sources (for example, interest or dividend income) will no longer be eligible to file ITR 4, except where the deduction pertains to family pension.

Says Hemkar: “In order to claim a credit of taxes withheld in foreign jurisdictions (FTC), currently taxpayers are required to furnish a specified form. However, the draft rules require the FTC claim forms to be verified by an accountant inter alia, in cases where the foreign tax paid outside India by the individual is Rs 1 lakh or more during the tax year.”

The draft rules also place greater emphasis on complete and accurate filings. Says Panjiar: “The framework is becoming more structured and less tolerant of incomplete disclosures. In that sense, the role of ITR is slowly evolving. It will no longer be just a self-declaration of income. Like goods and services tax (GST), it would increasingly be a reconciliation exercise between what the taxpayer reports and what various financial institutions have already reported to the system.”

The ITR, in short, is becoming more of a document you reconcile against what the system already knows (see New Disclosure Requirements).

Conclusion

The new tax rules signal less of a dramatic tax reform and more of a structural modernisation of India’s personal tax administration. While most taxpayers are unlikely to see a major shift in how much tax they pay, they will notice changes in how income, exemptions and financial transactions are reported and verified.

With greater reliance on digital reporting, pre-filled returns, and third-party data matching, the new framework aims to make routine compliance easier while leaving less room for inconsistencies. Says Richa Sawhney, tax partner, Grant Thornton Bharat LLP: “These changes will reduce the need for manual data entry, minimise errors, and save time. For many salaried taxpayers, the return filing process may eventually involve reviewing and confirming the pre-populated information, enabling quicker filing of ITRs and potentially leading to fewer disputes.”

For salaried taxpayers with straightforward finances, the transition could ultimately simplify return filing, but for those with more complex financial arrangements, the new system will demand greater documentation, accuracy and awareness of the evolving compliance landscape.

Taxpayers should also note that the government now has access to data from multiple sources. With the increasing use of data analytics tools and AI, any non-disclosure can easily bring them under the tax department’s scanner.

sanjeev.sinha@outlookindia.com