In October 2017, the Securities and Exchange Board of India (Sebi), defined the products that mutual funds can offer to investors. Recently, on February 26, 2026, Sebi issued another circular that brought about certain changes in the fund categories, including the creation of the life cycle fund category.

Earlier, there was a broad category, called solution-oriented schemes, which has now been discontinued. Within this, there were two categories—retirement fund and children’s fund. Retirement fund was defined as a scheme with a lock-in of at least five years or till retirement age, whichever is earlier. Likewise, children’s fund was defined as a scheme having a lock-in for at least five years or till the child attains majority, whichever is earlier.

If you were saving and investing for retirement, there was nothing in particular about retirement funds apart from the lock-in feature. You could do it through any fund—large-cap, small-cap, or corporate bond fund. If you were to stay disciplined, you would stay invested for a long period, that could be perhaps 20 years or until your retirement. Similarly, if you were investing for your children, you could do it through any category you prefer. In that sense, these two funds were misnomers.

1 July 2026

Get the latest issue of Outlook Money

That has been corrected now. Among the many options one can use for building one’s retirement kitty or other time-defined goals are life cycle funds.

The Change

The recent circular by Sebi said that the existing schemes in the solution-oriented schemes category shall stop receiving subscriptions with immediate effect. These schemes shall be merged with other schemes having similar asset allocation and risk profile, with prior approval from Sebi.

The new category of life cycle funds has been defined as a scheme following “glide path strategy-based investing” across various asset classes, namely equity, debt, infrastructure investment trusts (InvITs), exchange-traded commodity derivatives (ETCDs), and gold and silver exchange-traded funds (ETFs).

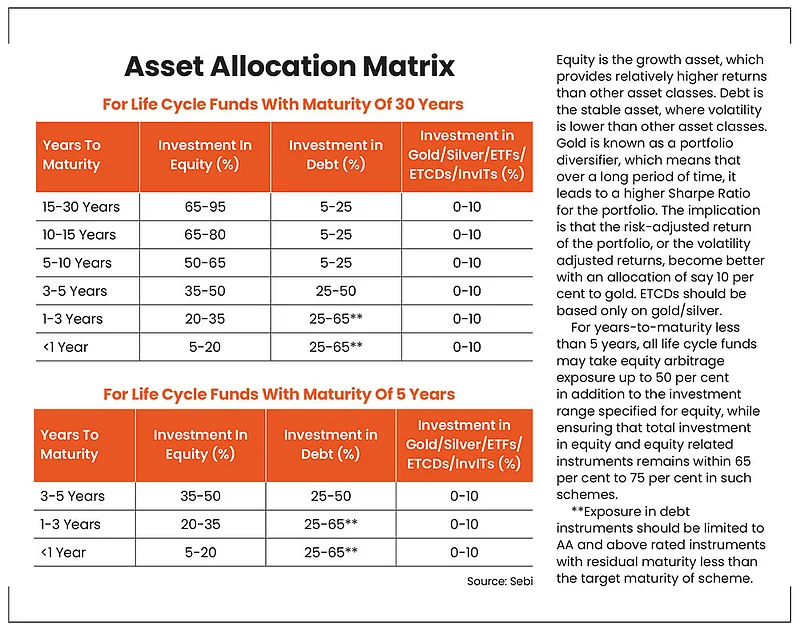

The contours of life cycle fund category allow mutual funds to launch them with a minimum five years tenure and maximum 30 years

The contours of this category are that mutual funds may launch life cycle funds with a minimum tenure of 5 years and a maximum tenure of 30 years. Such funds may also be launched for tenures in multiples of 5 years, and a maximum of six funds by a mutual fund can be active for subscription at any given point in time.

Additionally, as each fund reaches less than one year to maturity, such fund may be merged with a nearest maturity life cycle fund with the consent of the unitholders. Moreover, to inculcate financial discipline among investors in life cycle funds, an exit load of 3 per cent, 2 per cent and 1 per cent would be chargeable on any exit within one, two, and three years of investment, respectively.

Sebi has provided six matrices for asset allocation for different maturities between 5 and 30 years (See Asset Allocation Matrix for examples of asset allocation in funds with 5 and 30 years of maturity).

Essence Of Life Cycle Funds

Along with passage of time, as you near your financial goal, you need to de-risk your portfolio. These funds do that by reducing equity exposure and increasing debt exposure. The objective is that on maturity of the product you should take home something around the amount you expected. If the exposure to market volatility is on the lower side, which means exposure to equity is on the lower side, the purpose is served.

In the earlier years of the product, you take the benefit of the growth asset. The fund manager has some flexibility within the discipline. Therefore, exposure to equity, debt and gold has been given as a range and not a finite number. In case, you have some more investment horizon left from the maturity of the product, and if the asset management company (AMC) is merging the fund with another life cycle fund with limited residual maturity, you can opt for that.

How Can You Utilise It?

There are a plethora of products or avenues available for investment. There are 13 equity fund categories, 17 debt fund categories and seven hybrid fund categories in mutual funds. Then there are ‘n’ number or ETFs or index funds, and fund of funds (FoFs). You can buy equity stocks and bonds yourself. There are also portfolio management services (PMSs) and alternative investment funds (AIFs). You are spoilt for choice. If you want to settle for something that is straight-jacketed and disciplined, you may choose life cycle funds.

With six maturity horizons available, ranging from 5-30 years, you can use a laddered approach, that is, classify your financial goals from 5-30 years and invest money accordingly. While it is possible to do it yourself through other funds by changing the allocation as you reach closer to your goal, you need to be mindful that sometimes discipline takes a back seat and there are tax implications.

By Joydeep Sen, Corporate Trainer and Author