For the Indian middle class, a global degree has long been a crown jewel on the path to social and professional mobility. However, in 2026, the cost of that dream is being redrawn by two diverging forces: the Centre easing the tax friction in sending money abroad, and a global economy that is making the dollar more expensive than ever.

First, the good news. The Union Budget 2026 provided relief to parents by slashing tax collected at source (TCS) on education-linked remittances from 5 per cent to 2 per cent. But the bad news is that for a family targeting their children’s admission abroad in 2026 or 2027, the rupee’s steady decline against the US dollar is offsetting this benefit. With the exchange rate at Rs 93.26 per dollar, as on March 19, 2026, a simple send-money-when-needed approach is no longer optimal. To plan cash flow, tax credits and exchange risk, parents need to recalibrate their strategy.

The Liquidity Shift

1 July 2026

Get the latest issue of Outlook Money

Previously, outward remittances up to Rs 7 lakh in a financial year for education purposes did not attract TCS, and any remittance beyond that was subject to 5 per cent TCS. Now, this limit has been enhanced to Rs 10 lakh in a financial year and TCS has been pared to 2 per cent.

For a family remitting Rs 25 lakh from personal savings, the math changes significantly. Aritra Ghosal, CEO and founder of OneStep Global, a market entry firm specialised in the higher education sector, breaks down the immediate impact: “If a family remits Rs 25 lakh in a financial year, the first Rs 10 lakh will not attract TCS. On the balance Rs 15 lakh, they will have to pay TCS at 2 per cent, which comes to Rs 30,000. Previously, they would have to pay 5 per cent TCS on Rs 18 lakh, which would be Rs 90,000. The difference in cash outgo is Rs 60,000.”

But it is important to track the annual threshold and plan the timing of transfers carefully to calculate the benefit. Dishit Parekh, chartered accountant (CA), certified financial planner (CFP), and founder of Foresight Financial Advisory, a mutual fund distributing firm based in Ahmedabad, says, “If tuition and living expenses are close to Rs 10 lakh, families may consider splitting remittances across financial years where timelines allow, in order to reduce exposure to TCS.”

He adds that currently remittances funded through an education loan from a recognised financial institution generally attract nil TCS under Section 80E of the Income-tax Act, 1961. Before April 2025, it was 0.5 per cent on sums above Rs 7 lakh.

Now, outward remittances up to Rs 10 lakh in a financial year for education purposes will not attract TCS. Any amount beyond that will have a TCS of 2 per cent

Though TCS is reimbursable at the time of filing income tax returns (ITRs), if no or less tax is applicable, the liquidity benefit is immediate. That’s a positive, says Ashish Niraj, CA, partner at ASN & Company, a CA firm: “Rule 220 of the Draft Income Tax Rules, 2026, has continued the rule 37BB, whereby no form 15CA/15CB (Now Form 145/146), is required for travel for education (including fees, hostel expenses etc).” Under this rule, parents do not need a CA’s certificate or formal tax declarations (Forms 15CA/15CB, now 145/146) for education-related transfers. This exemption for tuition and hostel fees removes red tape, making it faster and cheaper to send money abroad.

Ghoshal adds: “Families are managing tuition and hostel deposits, visa documentation, and forex movement simultaneously. So, any reduction in upfront outflow improves liquidity at a critical stage.”

Rupee Vs Dollar: Cost Driver

While TCS cut is a tactical benefit as you get the money back as tax refund, currency depreciation leads to permanent loss of capital. Even if the tuition fee does not rise, rupee depreciation escalates the total cost.

Arijit Sen, a Securities and Exchange Board of India-registered investment advisor (Sebi RIA) from Kolkata says that focusing only on tax can be a trap. “The Budget 2026 tweak that sets TCS at 2 per cent above Rs 10 lakh is a tactical change, not a strategic game‑changer. The lower TCS reduces cash drag on large transfers, but doesn’t remove currency risk, or bank spreads.”

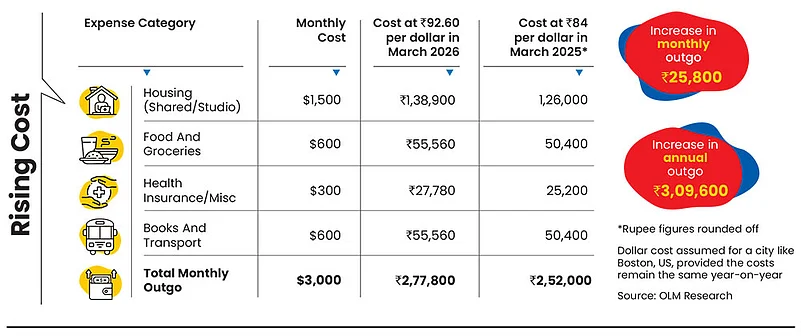

To understand the impact, let us look at the monthly remittance spike for a student in a high-cost city like Boston, where living expenses (rent, utilities, food, and local transport) average $2,000-4,000 per month. For our example, let’s take the total monthly outgo as $3,000. In March 2025, when the rupee was at Rs 84 per dollar, the monthly outgo would have been around Rs 2.52 lakh, which would be around Rs 2.77 lakh in March 2026 when the rupee was Rs 92.60 per dollar.

That’s an additional Rs 25,800 per month, or Rs 3,09,600 annually (see Rising Cost). For a four-year undergraduate degree, that will add more than Rs 12 lakh to the total cost.

Saurabh Bansal, founder of Finatwork Investment Advisor, calls it a “hidden fee hike”. “A $50,000 annual cost that seemed manageable at, say, Rs 83 per dollar becomes significantly more expensive at Rs 91, creating an unplanned gap of nearly Rs 4 lakh per year. Since most education loans are rupee-denominated, this mismatch often forces families to either dip into savings or take additional debt.”

For example, if a parent takes a loan of Rs 75 lakh when the exchange rate is Rs 85, they are effectively borrowing $88,235. But, if the rupee falls to Rs 92.60 by the time the final year’s tuition is due, the same Rs 75 lakh buys $80,993, a shortfall of Rs 6.60 lakh.

Further, as the student requires more rupees to buy the same amount of dollars for monthly living expenses, the interest burden on the loan compounds faster as the principal increases earlier in the loan tenure.

What Should You Do?

Invest Strategically: The rupee has historically depreciated against the dollar. According to Foreign Exchange Dealers’ Association of India, in early 2021, the rupee was Rs 73 against the dollar, while the yearly average for the same year was Rs 72. According to data cited in the Reserve Bank of India (RBI) Handbook of Statistics, the rupee depreciated by approximately 4 per cent annually since 2021, breaching Rs 90 per dollar by December 2025.

As a result, it’s advisable to plan for this extra cost in advance by investing in dollars instead of investing in rupees. By holding assets in the currency of the future expenditure, parents can create a natural hedge.

One way is to create a liquid corpus in foreign currency. Under the RBI’s Liberalized Remittance Scheme (LRS), each resident individual can remit up to $250,000 per financial year.

Says Prashant Mishra, CEO of Agnam Advisor, a Sebi-registered fee-only investment advisory firm: “Parents can use this limit of 2-3 years before the child leaves for university to build a dollar-denominated corpus. For families funding overseas education over 2-3 years, even a 5-7 per cent depreciation can significantly increase the total costs, adding several lakhs to the total expense.”

Another way is to invest globally. Says Mishra: “Investors who already hold international funds or global exchange-traded funds (ETFs) may benefit when the rupee weakens. This is because the value of dollar-based investments rises when converted into rupees. These gains come purely from currency movement and can add to the overall returns over time.”

Bansal adds: “Allocating 10-20 per cent of the portfolio to international assets through global mutual funds, ETFs, or overseas fixed income can provide balance and reduce concentration risk.”

“At the same time, it is important to recognise that global investments introduce their own dynamics, such as market fluctuations, differences in economic cycles, and timing considerations,” says Dante De Gori, CEO, Financial Planning Standards Board (FPSB) International.

He adds: “The value of these investments may not always move in line with currency changes or align precisely with when funds are required. In practice, many investors view global exposure as part of a broader portfolio rather than a standalone solution. A structured approach, grounded in long-term planning and aligned to specific financial goals, can help families navigate both currency and market-related uncertainties more effectively.”

However, financial planners do not advise investing globally only, as currency movements depend on many factors, such as inflation, trade balance, capital flows, and central bank policies. Predicting them consistently is difficult. They suggest that the better way to think about international investing is diversification; in this case, holding investments in different currencies can make portfolios more stable.

Use Loans Wisely: Previously, a lot of families took a loan because a part of their savings could get blocked because of high TCS. Says Saurabh Arora, founder and CEO of University Living, a global student housing marketplace: “With the move from 5 per cent to 2 per cent, that cash block becomes smaller. Many will go back to a simpler structure: use savings for the first tranche, use a loan if it helps with affordability, repayment planning, or currency timing.” That strategy can also help fund the gap.

Get The Paperwork Right: In the rush to secure seats, paperwork accuracy often becomes secondary, but even minor classification errors can delay refunds and create liquidity issues. One such nomenclature is Purpose Code S0305, which is designated by banks to record education-related outward remittances. “A clerical error misclassifying an education transfer as a gift or general remittance can trigger a 20 per cent TCS rate,” says Arora.

The key, according to experts, is to focus on active currency management and disciplined global diversification to be able to fund your child’s future abroad without destabilising your own long-term goals.

priyanka.debnath@outlookindia.com