In a cafe in Kolkata, 24-year-old Arpan (name changed) looks at his new mirrorless camera. To his peers online, the Rs 85,000 device is a sign of a thriving creative career. To Arpan, it is a daily reminder of something that holds his financial profile hostage. Earning an entry-level salary of Rs 32,000 a month, Arpan could not afford the upfront cost. But a two-minute, zero-downpayment checkout via an e-commerce platform’s digital lending partner made the decision seamless. The equated monthly instalment (EMI) was Rs 7,500. “It didn’t feel like borrowing at the time,” Arpan says, “It felt like an extension of my monthly pay cheque.”

Arpan’s situation reflects a bigger pattern in how young adults interact with money.

According to Deloitte’s Global Gen Z and Millennial Survey (2026), 47 per cent of Gen Z and Millennials, globally, live pay cheque to pay cheque, with 34 per cent struggling to cover basic monthly living expenses. The cost of living remains their primary concern, cited by 38 per cent of Gen Z, ahead of unemployment and climate change. Financial anxiety acts as a driver of daily stress for 44 per cent of this demographic. Then why are the Gen Z giving in to debt?

1 June 2026

Get the latest issue of Outlook Money

Drivers Of Debt...

Online Identity: The fear of missing out (FOMO) and the urge to be part of every social media trend is met by digital platforms designed to reduce transaction friction.

“The pattern we see is no longer about need; it’s about identity,” says Saurabh Bansal, a Securities and Exchange Board of India registered investment advisor (Sebi RIA) and founder of Finatwork Investment Advisor. “This generation is not borrowing because they can’t afford things, they’re borrowing because they don’t want to feel left behind.”

Data from the Redseer report, Gen Z: Defining Trends, Influencing Spends (March 2026), projects that Gen Z’s spending power will reach $1.3 trillion by 2030, making up 27 per cent of the population.

Borrowing is now driven by lifestyle needs rather than emergencies or commitments. Credit is now being used as a lifestyle funding mechanism

This capital is flowing into lifestyle and aesthetic categories. The beauty and personal care (BPC) market is set to reach $19 billion by 2030, with one in two Gen Z women spending over 20 per cent of their disposable income on BPC products. Online searches for “men’s skincare routine” increased by 850 per cent over five years. Gen Z is also on track to drive half of the fashion e-commerce market by 2030.

Bansal says this trend connects to an online presence. “When so much of your life is online, what you own starts becoming part of how people see you,” he says. “A new phone, a Goa trip, a branded watch or expensive sneakers are no longer just purchases, they become a way of showing success and fitting in.”

The purpose of borrowing is now lifestyle rather than an emergency or commitment. A study by Home Credit, How India Borrows (2024), shows that personal loans—taken specifically to fund premium consumer electronics and high-tech gadgets—grew from 1 per cent in 2020 to 37 per cent in 2024. At the same time, loans taken for medical emergencies declined from 7 per cent in 2020 to 3 per cent in 2024. This shows that credit is now being used as a lifestyle funding mechanism rather than an emergency safety net.

Instant Credit: Buy Now, Pay Later (BNPL) services and instant non-banking financial company (NBFC) plug-ins at checkout lower the immediate financial impact of a purchase.

According to TransUnion CIBIL reports spanning 2025-2026, the Gen Z are entering the formal credit system at a rapid pace, comprising 41 per cent of all New-to-Credit (NTC) first-time borrowers in India. Within the segment, 40 per cent choose consumption-led products, such as credit cards, personal loans, and consumer durable loans, as their initial entry point.

Another report, by CRIF High Mark, titled Bridging The Gap (2026), shows that NTC borrowers entering India’s formal system grew from 3.6 crore in 2022 to 4.4 crore as of February 2026. NBFCs and fintech platforms support over 60 per cent of these NTC accounts.

“The need for credit has always existed, but what has changed is the ease and immediacy of access,” says Sachin Seth, regional managing director for CRIF India and South Asia. “Small-ticket, unsecured loans were not viable under traditional lending models, but digital platforms have made them scalable and widely accessible.”

The instant credit infrastructure has clearly added to altered consumer attitudes. “It has subtly shifted behaviour; credit is increasingly seen as a tool for convenience and flexibility, rather than a long-term financial commitment,” says Seth.

Uncertainty: According to a report titled GenZ-eitgeist (2026), by Edelman Gen Z Lab, a specialised advisory unit and data hub within the PR and marketing firm, 60 per cent Gen Z believe a standard 9-to-5 career will not grant them financial independence, eroding confidence in traditional wealth accumulation and contributing to immediate consumption decisions.

Due to this lack of confidence, they seem to be altering milestones that defined previous generations. The Deloitte data indicates that 55 per cent Gen Z have postponed marriage, starting families, launching businesses, or pursuing higher education due to financial strain. Further, 51 per cent said they cannot afford to buy a home.

…Can Create A Debt Trap

The Edelman report says that 40 per cent of the Gen Z in the US use BNPL services one or more times a week. Within that regular user base, 25 per cent have missed at least one payment, and 31 per cent do not even know how much total outstanding debt they have.

What they might now realise is that the seemingly harmless situation can deteriorate into a debt trap. Amit Suri, CFP, founder and CEO of AUM Wealth, a wealth management firm based in New Delhi, warns that minor outflows can quickly create a major drag on monthly earnings. “One EMI may appear manageable, but several subscriptions, BNPL commitments, credit card dues, gadget loans, and travel EMIs can quietly consume a significant portion of monthly income.” he says.

That’s what happened with 23-year-old Mehak Malhotra (name changed). Behind the frantic pace of life in Delhi, the true math of small-ticket digital loans played out a little later for Mehak, who earns Rs 42,000 a month.

Like Arpan, she used digital credit for immediate flexibility. She financed a smartphone on a no-cost EMI plan and later used a travel BNPL service for a weekend trip.

“The checkout process is integrated so smoothly that it does not feel like spending real money,” says Mehak. “But when you combine a Rs 3,000 phone EMI, a Rs 4,000 travel EMI, and multiple smaller BNPL bills, more than half my salary is gone the same day it is credited.”

Within a year, Mehak was managing repayment obligations across six digital lending platforms. To manage repayments, she used credit lines from one fintech app to cover the minimum due on another. Her total outstanding debt eventually reached Rs 2,40,000, requiring a monthly EMI outflow of Rs 26,000, which consumed over 60 per cent of her earnings.

Borrowing for depreciating assets does not make a borrower riskier; missing payments do. This may happen when you borrow beyond what you can repay

“The biggest blind spot is focusing only on the EMI rather than the total repayment amount,” says Amit. “The second blind spot is underestimating how multiple small loans accumulate.”

Data from CRIF High Mark and the Digital Lenders Association of India (DLAI) has indicated that by late 2025, nearly 26 per cent of digital borrowers under the age of 30 were delinquent on small-ticket personal loans, capped under Rs 50,000.

The Reserve Bank of India’s (RBI’s) Financial Stability Report (FSR), released on December 31, 2025, mentioned that over 70 per cent of fintech loan portfolios consist of unsecured credit. Unsecured retail loan defaults account for 76 per cent of all loan slippages in private sector banks and their technology partnerships, compared to 15.9 per cent for public sector banks.

…And Affect Your Future

When Mehak wanted to apply for a standard credit card, she found her credit score had declined to 585 due to delinquencies on small-ticket loans.

Says Suri: “Many young borrowers fail to appreciate the impact on future borrowing capacity. A weak credit profile can affect eligibility and pricing for important future goals.”

Borrowing for depreciating assets or lifestyle does not make a borrower riskier; missing payments do. And that may happen when you borrow more than you can afford to repay. Explains Seth: “Risk profile is primarily determined by a borrower’s repayment track record and a balanced liability portfolio. Credit scores play a central role in lending decisions. Defaults, can have a disproportionate long-term impact, affecting not only the ability to access credit later but also the terms at which it is available.”

Getting burdened with too much debt early on can affect long-term wealth creation. “Every EMI reduces the amount available for investing in assets such as equities, businesses, or property,” says Bansal. “In many cases, young earners are mortgaging their future financial freedom to finance present consumption.”

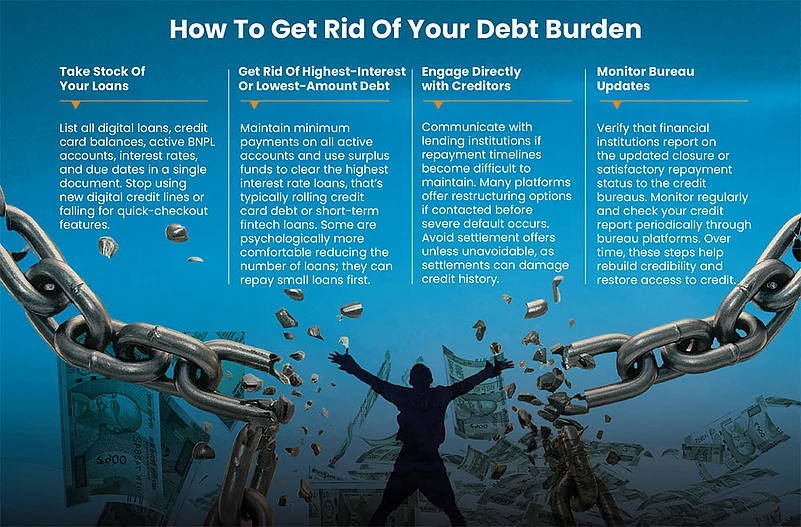

Back On Course

Clean Up Your Debt: The first step in your priority list should be to get rid of debt. Experts recommend a structured approach (see How To Get Rid Of Your Debt Burden).

Identify The Problem: It’s very important to narrow down on the factors that got you in such a situation. “One should review their last six months of bank and credit card statements and classify every borrowing instance as a need, a convenience, or an impulse,” advises Suri. “If most debt has funded lifestyle upgrades instead of essential needs or income-generating opportunities, the issue is not budgeting, but a mismatch between aspirations and cash flow.”

Build A Liquidity Cushion: Create an emergency fund equivalent to at least one month of basic living expenses, which can be increased eventually to about six months of expenses. Also, get insurance coverage before you start any other goal-based investing. These financial fundamentals form a buffer and will reduce reliance on digital loans for unexpected expenditures.

Choose An Expert Who Understands You: It’s important to align investments with the new consumer psychology. “Younger investors see near-term, faster-gratification goals a lot more clearly than long-term, conventionally ‘boring’ objectives like retirement planning,” says Mohini Mahadevia, CFP and founder of SOLUFIN, a financial services and consultancy firm in Mumbai. “There is a very clear weightage given to goals that older investors may deem ‘frivolous’.” Having an advisor who can strike the right balance can make a huge difference.

Have Smaller Goals: Tie savings to your goals, even smaller ones. Mahadevia suggests, “List your goals, as many as there are, have a separate SIP for each, set your targets and start saving for them. Imagine having enough money saved for that expensive ticket to a concert or that new phone you want to buy. So much better than mindlessly swiping credit cards and taking on debt through no-cost EMIs.”

Goal-directed investing offers an alternative to credit checkouts.

Build Wealth: Once you inculcate investing discipline, think of building long-term wealth. Increasing systematic savings alongside income growth can substantially alter long-term wealth outcomes. For instance, investing of Rs 10,000 per month starting at age 25 until age 60 can yield a corpus of Rs 5.51 crore, assuming a 12 per cent annual return. If you implement a step-up strategy by just 5 per cent annually, the projected corpus at 60 increases to Rs 8.62 crore.

The RBI has implemented a series of measures to decrease loan push, besides banning illegal loan apps. The key is to strike a balance between how you want to live your life and what you want your future to look like.

priyanka.debnath@outlookindia.com