Choosing between domestic and international investments is often compared to choosing between a fancy car brand like Ferrari and the trusted homegrown Maruti. Both can serve the purpose and deliver value, but the decision appears to be about preference, for those who can afford both.

Investing, however, is not about brand appeal or preference. It is about risk management, diversification, and long-term wealth creation. So, when it comes to global and domestic investments, it’s not an either-or situation. Global investing is not about replacing your domestic investments. It is about complementing your portfolio with global exposure to different sectors, currencies, and economic cycles. Says Swarup Anand Mohanty, vice chairman and chief executive officer (CEO), Mirae Asset Investment Managers (India): “For Indian investors today, some international exposure is no longer just tactical, it is sensible diversification.”

We earn our income in India either through our jobs or businesses. We, typically, own our house or other properties in our home country. Most of our investments are also tied to Indian markets. Most individuals hardly have any global exposure, and with growing confidence in the Indian markets, many don’t even see the need for it.

1 July 2026

Get the latest issue of Outlook Money

But the real question is not whether Indian markets are good enough. “Adding global assets is not about doubting India’s growth story; it’s about reducing concentration risk,” says Mohanty. The real question is: in an interconnected world, does it make sense to limit yourself to one geography?

Why You Should Go Global

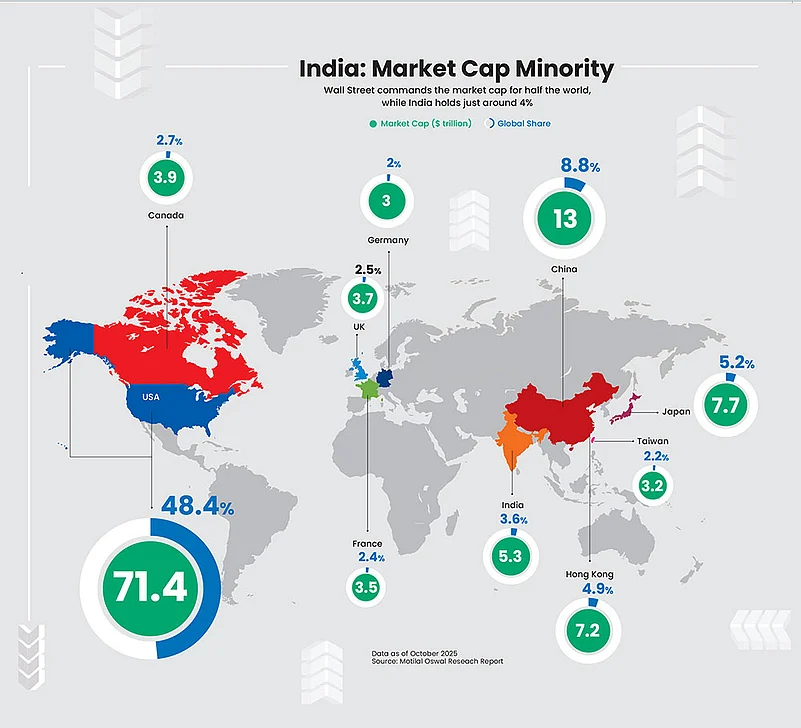

Undoubtedly, India is among the fastest growing economies in the world, yet it has its own limitations. “India accounts for around 4 per cent of global market capitalisation and gross domestic product (GDP), making international diversification essential for a well-balanced portfolio,” says Abhishek Tiwari, CEO, PGIM India Mutual Fund. Out of the top 500 companies globally, based on revenue, only nine are from India, he adds.

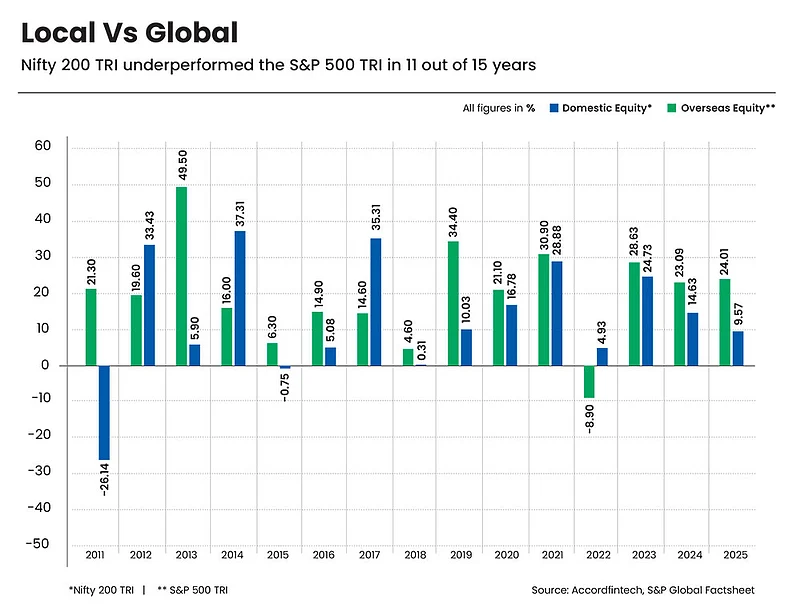

Performance: While emerging markets are typically associated with higher growth potential, this has not consistently translated into superior equity returns. To challenge the widely considered belief that emerging markets consistently deliver superior returns, we analysed the performance of two broad-based benchmark indices over the past 15 calendar years (2011-2025). For domestic equities, we considered the Nifty 200 TRI, and for global equities, the S&P 500 TRI.

Over 2011-2025, data reveals a clear trend: the Nifty 200 TRI underperformed the S&P 500 TRI in 11 out of 15 years, often by a wide margin. For instance, Nifty 200 TRI delivered strong outperformance in select bull phases, notably in 2014 (37.31 per cent), 2017 (35.31 per cent), 2012 (33.43 per cent), and 2021 (28.88 per cent). On the other hand, S&P 500 TRI significantly outperformed in years other than these, including in 2013 (49.50 per cent versus 5.90 per cent from Nifty 200 TRI), 2019 (34.40 per cent vs 10.03 per cent), and 2011 when the overseas markets gained 21.30 per cent while domestic markets fell sharply by 26.14 per cent (see Local Vs Global).

Government policy, geopolitical situation, sector composition, corporate profitability, currency movements, and valuation cycles play a key role in market returns. This finding suggests that relying solely on the “higher growth equals higher returns” narrative may be over simplistic as economic growth and stock market returns do not always move in tandem.

Access to Global Leaders and Innovation: Many of the world’s most transformative companies operate outside India. Given this, one of the strongest arguments for global investing is access to companies that dominate industries worldwide and have no comparable equivalents in our domestic market.

For instance, Apple Inc. and Microsoft Corp. have transformed consumer technology and enterprise software globally. NVIDIA Corp. has become central to the artificial intelligence revolution, powering data centres and advanced computing worldwide. In e-commerce and cloud infrastructure, Amazon.com. Inc. dominates global markets, while Alphabet Inc. leads in digital advertising, search, and artificial intelligence (AI) research.

Healthcare innovation is similarly global. Companies like Johnson & Johnson and Novo Nordisk are leaders in pharmaceuticals and biotechnology, driving breakthroughs in diabetes care and obesity treatments. Many of these sectors, such as advanced semiconductors, hyperscale cloud computing, global social media platforms such as Meta, LinkedIn and X (earlier Twitter) have no representation in Indian indices.

“The US remains the hub for innovation, particularly in technology, healthcare, and consumer sectors, and is quickly advancing in AI and that continues to be the reason to remain positive on opportunities,” says Tiwari.

Global diversification, therefore, is not merely geographic, it is also about access to industries and innovation ecosystems that may not exist locally.

Advantage of Rupee Depreciation: The biggest risk that global funds carry is currency risk. The movement of the rupee versus the dollar or the currency of the particular country where the fund invests in affects its performance. However, this works in your favour if the rupee depreciates.

“The weakening rupee against the US dollar can have a positive impact on the returns of Indian investors in US-focused funds. Since these funds invest in US equities, their underlying assets are denominated in dollars. When the rupee depreciates, the value of these dollar-denominated investments increases in rupee terms, boosting overall returns for Indian investors. Currency depreciation adds 2-3 per cent to the portfolio returns,” says Tiwari.

The rupee has historically depreciated against the dollar. Since April 2022, the rupee has depreciated over 16 per cent. For instance, in the last one year, the rupee has depreciated around 4.29 per cent. In this case, if you had invested in dollar-denominated equity, the currency depreciation itself would have added 4.29 per cent return to your portfolio.

This may, however, go against you if the domestic currency appreciates.

How Do You Go Global?

Gaining exposure to global equities is no longer complicated. Indian investors can participate through international mutual funds, India-listed global exchange-traded funds (ETFs), direct overseas investing under the Reserve Bank of India’s (RBI’s) Liberalised Remittance Scheme (LRS) through foreign brokers, or Global Access Providers through GIFT City. Each differs in terms of currency exposure, cost, and operational complexity. You need to decide based on your comfort level, investment knowledge, ticket size, and long-term asset allocation strategy.

Through Mutual Funds: The most convenient and cost-effective way for investors to access global equities is through mutual funds (MFs), which offer multiple options to participate in international markets.

Some domestically-oriented equity schemes also provide limited overseas exposure. For instance, in the flexi-cap space, Parag Parikh Flexi Cap Fund is mandated to invest up to 35 per cent of its corpus in international equities. Similarly, multi-asset allocation funds (MAAFs) such as Nippon MAAF, Invesco MAAF, DSP MAAF, and Mirae Asset MAAF alllocate a portion of their portfolio overseas.

Another category is international funds that invest their entire corpus internationally. They are feeder funds that invest in an underlying global fund or ETF. They can invest in international schemes run by their foreign parents who would further invest in international markets. These include Birla Sun Life International Equity Fund and DSP BR World Gold Fund.

Unlike domestic equities, which qualify for LTCG tax after a holding period of 12 months, for foreign equities, the holding period is 24 months

Then there are those that directly buy ETFs or stocks listed in overseas market. Also, you could choose to invest in funds that focus on specific countries or those that invest across different geographies. For instance, Mirae Asset China Advantage Fund primarily focuses on China, while ICICI Pru Global Stable Equity Fund of Fund invests across geographies. Such funds offer broader diversification across geographies.

Through Gift City: Under RBI’s LRS, resident Indians can remit up to $250,000 per financial year for overseas investments. This allows investors to directly invest in outbound MFs, global stocks, such as Apple, Microsoft, or ETFs listed in the US. This route provides you the flexibility to invest in specific companies of your choice, but involves currency remittance, and brokerage accounts with global access such as INDmoney, Vested Finance and so on.

When you invest in foreign securities, the first step is transferring money to an overseas broker.

Technically, this qualifies as a foreign remittance, and it attracts tax collected at source (TCS). Under current regulations, TCS applies only after the threshold of Rs 10 lakh is crossed in a financial year. This means you can remit up to Rs 10 lakh abroad in a year without any TCS deduction. If your total foreign remittances exceed this amount, TCS is applicable only on the portion above Rs 10 lakh, and not on the entire remittance. TCS is adjustable against your final income tax liability when you file your income tax return.

Through Foreign Brokers: The other way of investing in overseas equity is through a foreign broker. It allows you to directly own global stocks, ETFs, and other securities listed overseas. The process, typically, involves opening an international trading account, completing know-your-customer (KYC) formalities, and remitting funds under LRS. This route is a bit complicated as it requires a lot of paperwork.

What Should You Do?

Once you pass the first level of diversification (investments within India) across sectors and scrips, either directly or through the mutual fund route you can go for international equity.

“India can remain the core, but global diversification adds balance and resilience,” says Mohanty. However, he cautions against making aggressive country-specific bets, unless you have a strong view and the ability to stay invested through volatility.

“For most investors, a globally diversified fund makes more sense as it provides exposure to global innovation and multiple economies without forcing them to time a single market,” says Mohanty. Global investing is also about longer horizons, so don’t get swayed by near-term positive returns, he adds.

Also, consider taxation. Unlike domestic equities, which qualify for long-term capital gains (LTCG) tax after a holding period of 12 months, foreign equities are treated differently for taxation purposes. In the case of foreign equity investments, the holding period required to qualify as long-term is 24 months, not 12 months.

kundan@outlookindia.com