India's lower middle class is showing resilience and optimism, although saving is declining and borrowing to meet necessities remains a worry. Spending in 2025 is being shaped by evolving priorities, modest income growth, and growing reliance on digital platforms, according to the latest report by Home Credit India, titled The Great Indian Wallet 2025.

Building on an 18-to-55 consumer survey of 17 cities—metros to small towns—the report takes close-up shots at how these families are spending, borrowing, and thinking about the future.

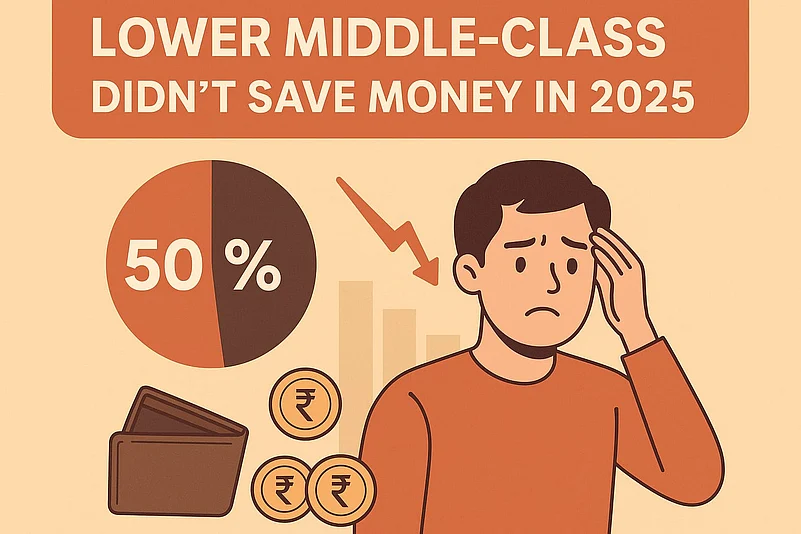

Income Is Up, But Savings Have Dropped

Around 57 per cent of respondents reported an increase in income this year, up from 52 per cent in 2024. The average monthly income among the lower middle class now stands at Rs 33,000, while essential monthly expenses hover around Rs 20,000.

Although there is rise in income, 50 per cent of families didn't save this year—a decrease from 60 per cent in the past year. It's still difficult to cover basic costs for some families: 12 per cent mentioned they had to borrow to cover basic costs.

Education Spending On The Rise

While food is still the largest monthly expenditure category (29 per cent), education spending has surged—34 per cent more in the last year and representing 19 per cent of family spending. This added spending on education tells much about how families are prioritising kids.

Of Gen X adults surveyed, as much as 22 per cent of monthly spending goes for schooling children.

Financial Conduct Is Being Transformed by Online Instruments

Online instruments have impacted the way families plan their budgets. Roughly 63 per cent of consumers believe that websites have made it easier to achieve their financial goals. This is very common in cities like Jaipur, Pune, and Kolkata.

Retail spending via online medium now represents 51 per cent of overall spending, up from 42 per cent in 2024. Online loan applications have reached equilibrium with offline, standing at 50 per cent each, reflecting greater trust in digital lending.

The usage of Unified Payments Interface (UPI) is on the rise, with 80 per cent citing its use in day-to-day transactions. However, there are concerns—nearly half said they'd abandon UPI if they are charged for the transactions.

Spending Is Getting More Reflective

The report advocates a shift in wiser spending habits. While 39 per cent continue to shop for clothing and accessories, this has fallen by 20 points from previous years. Inland holidays are now more popular than ever, with 31 per cent holidaying at nearby locations each month. Gen Z is responsible for 44 per cent of these inland travellers.

OTC and gym, and OTT subscriptions are increasing but are still a modest percentage of expenditure—7 per cent and 6 per cent respectively.

Savings Are Still Cash-Weighted

Cash remains the preferred means of saving for 38 per cent of the interviewees. Other savings instruments are bank savings (24 per cent), life insurance (8 per cent), property (7 per cent), and gold (4 per cent). This means that even with digital development, most households still prefer liquidity and unorganised saving practices.

Concerns Still Remain, but Hope Inspires Action

Despite financial hardship, optimism abounds. 73 per cent of those questioned are optimistic that they can achieve their financial goals within five years' time. 65 per cent believe access to low-cost credit will help them to do it in even less time.

Still, problems remain. 18 per cent of families are concerned about education costs, and 15 per cent are ill-prepared for emergencies because they do not have savings. Another 58 per cent of respondents also said that they would like some financial guidance, highlighting the need for greater awareness and advice.

Among female respondents, increased employment opportunities were also strongly correlated with financial success, and hence gender-sensitive financial inclusion policies are the need of the hour.

A Financially Conscious Segment in Transit

The findings paint the picture of a financially savvy and technologically active segment that, short of constraints, continues to stay ahead and plan for a better tomorrow. From rising incomes and changing expenditure patterns to embracing digital technologies and seeking credit responsibly, India's lower middle class is rewriting its financial story in subtle ways.

With the right kind of support in the form of low-cost financial products, stronger digital schooling, and accessible advice, this market can contribute constructively to broader economic progress.