Summary of this article

With medical inflation outstripping general inflation by a wide margin, and treatment costs increasing year on year, many financial planners suggest that families maintain a separate corpus for health care.

Unlike a general emergency fund, which is designed to cover any sudden financial shock, a health corpus is purpose-built for medical contingencies.

Ideally, the two should work together. Insurance takes care of the catastrophic risk, while the healthcare corpus supports everything around it.

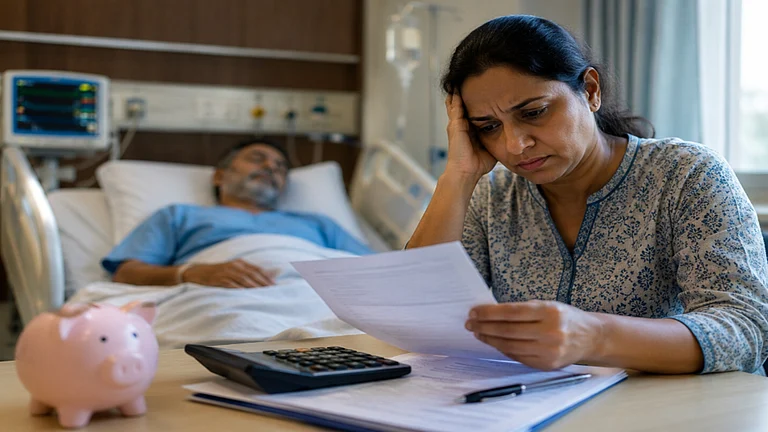

Health insurance is often seen as the first line of defence against rising medical costs. However, most families who actually end up hospitalised realise that insurance does not take care of everything. Medicines, diagnostics tests, homecare, travel costs and policy exclusions are just a few categories that come directly out of pocket.

With medical inflation outstripping general inflation by a wide margin, and treatment costs increasing year on year, many financial planners suggest that families maintain a separate corpus for health care. Think of a health corpus as an emergency fund with a specific purpose.

But how much should you set aside? Can a health corpus ever replace health insurance, especially when premiums become expensive in old age? Or do both serve different purposes? Here we take a look at why every household should think beyond buying health insurance and start planning for the true cost of staying healthy.

What Is A Health Corpus? Is It Different From An Emergency Corpus?

Unlike a general emergency fund, which is designed to cover any sudden financial shock (job loss, urgent home repair, a major car breakdown, etc.), a health corpus is purpose-built for medical contingencies.

The distinctions matter in practice:

• An emergency corpus is typically sized at 3 to 6 months of household expenses and is kept highly liquid in a savings account or overnight/liquid mutual fund. It is a broad safety net.

• A health corpus, by contrast, is sized based on one's healthcare risk profile - age, number of dependants, existing chronic conditions, the adequacy of insurance cover, and the city of residence (which determines hospital costs). It is larger, may be invested slightly less conservatively (e.g., in a short-duration debt fund or a laddered FD), and is drawn upon only for medical needs.

“In essence, a health corpus is a financial sub-account dedicated to health, sitting alongside - not replacing - the emergency fund,” says Arun Ramamurthy, Co-founder, Staywell.Health.

“Mixing the two pools is a common mistake. When a family dips into the emergency fund for a hospitalisation and then faces another emergency shortly after, they are financially exposed on both fronts,” he adds.

Why Do We Need A Health Corpus?

Buying health insurance is an important first step, but it doesn't eliminate medical expenses. India continues to have one of the world's highest out-of-pocket healthcare spends, with nearly 40 to 47 per cent of healthcare costs still being paid directly by households.

“Even policyholders often end up dipping into their savings. Consumables such as gloves and syringes, OPD consultations, diagnostic tests, physiotherapy, travel, attendant charges, and home care are either excluded or only partly covered by most policies. Add waiting periods, room-rent limits, co-payments and exclusions for certain treatments, and the gap becomes even wider,” says Ramamurthy.

The result? A family with a Rs 20 lakh health insurance policy could still end up paying Rs 2-6 lakh from its own pocket during a single hospitalisation. That's why a dedicated health corpus has become an essential financial buffer that works alongside health insurance, not in place of it.

Determining The Size Of The Health Corpus

Most people think health insurance is enough, until they actually go through a medical emergency. That is usually when they realise how many expenses still come from their own pocket like medicines that are not covered, follow-up care, recovery costs, loss of income, or even the simple need to access better treatment without hesitation. That’s where a healthcare corpus becomes important.

“The size of it really depends on your life stage and responsibilities. A 30-year-old with corporate insurance and no dependents may not need the same buffer as someone in their 40s, supporting parents and children together. Your city matters too. Healthcare costs in metros have risen sharply, and medical inflation today is growing much faster than regular inflation. I think people should also look at their family medical history, lifestyle, existing insurance cover and income stability while deciding this amount,” says Sanjiv Bajaj, Joint Chairman and MD at Bajaj Capital Ltd.

The idea is not to build a massive corpus overnight. It is about slowly building a financial cushion that gives you confidence during uncertain moments. Because during a health crisis, the biggest relief is to know that you can focus on recovery and not worry about which investment to break or where the money will come from.

Is Building A Health Corpus Better Than Paying High Premiums In Old Age?

According to insurance experts, a healthcare corpus and health insurance solve two very different problems. Insurance protects you from a large, unexpected financial shock. A corpus gives you flexibility and liquidity when life becomes complicated.

“The reality is that one serious illness today can cost far more than most families anticipate. Even people with strong savings can see decades of wealth creation disrupted if they try to handle everything on their own. That is why relying only on self-insurance can become risky, especially in old age when treatments are expensive and prolonged care may be needed. At the same time, I understand why many people feel anxious about rising premiums later in life. That is exactly why health planning cannot begin at 55. The earlier people buy insurance, the more continuity benefits they build over time,” says Bajaj.

Ideally, the two should work together. Insurance takes care of the catastrophic risk, while the healthcare corpus supports everything around it like uncovered expenses, recovery needs, home care, or even future premiums. They build financial resilience together.

Can A Health Corpus Become A Substitute For Health Insurance?

There are definitely situations where people may have no option but to depend more on their healthcare savings. This is often the situation for people who delay buying insurance until later in life, have serious pre-existing conditions or face very high premiums due to age and medical history.

“In such situations, a dedicated healthcare corpus becomes less of a choice and more of a necessity. But honestly, these are situations people should try to avoid reaching in the first place. One thing we consistently see is that people underestimate healthcare planning when they are younger because they assume there is still time. But health insurance works best when bought early, before health complications appear,” informs Bajaj.

A healthcare corpus is a strong support system, but depending entirely on self-funded savings for medical care in today’s environment can put immense pressure on retirement goals and family finances. The smarter approach is preparation, not replacement.