Summary of this article

According to the BajajCapital Suraksha Kavach Report 2025, only 19 per cent of working women in India currently have life insurance in their own name.

Among women buying insurance today, the motivation is evolving from viewing insurance primarily as a tax tool to seeing it as an essential form of personal protection.

Women are asking sharper questions about exclusions, waiting periods, mental health cover, and long-term affordability.

The change isn’t loud. There are no dramatic campaigns or sweeping announcements. But across India’s cities and emerging urban centres, women are steadily changing how insurance is bought and why.

Mrs Bose, a 32-year-old marketing professional in Bengaluru, already had a health cover through her employer and was listed as a dependent on her husband’s policy. Yet in 2024, she bought a separate health insurance policy in her name. “It wasn’t about lack of cover,” she explained. “My employer policy is tied to my job. My spousal cover is tied to my marriage. I wanted protection that stayed with me.”

That single decision reflects a deeper behavioural shift quietly taking shape across the market.

According to the BajajCapital Suraksha Kavach Report 2025, only 19 per cent of working women in India currently have life insurance in their own name. Yet among women buying insurance today, the motivation is evolving from viewing insurance primarily as a tax tool to seeing it as an essential form of personal protection.

“Women today are not buying insurance because someone advised them to,” says Venkatesh Naidu, CEO, BajajCapital Insurance Broking Ltd. “They’re buying it because they recognise their own health, income, and life risks. That shift from compliance to consciousness is one of the most important changes we’re seeing.”

From Tax Planning To Protection Planning

For years, insurance purchases among women were largely transactional often driven by Sections 80C and 80D, bundled with investment products, and initiated by a spouse, parent, or advisor. Protection existed, but it was rarely the starting point.

Today, protection is increasingly primary.

The emergence of women-focused products reflects this changing demand. These products are not positioned as savings instruments. Instead, they address gaps women have historically navigated on their own - maternity complications, reproductive health, mental wellness, and conditions that affect women differently across life stages.

“What’s changed is intent,” Naidu explains. “Women are asking sharper questions about exclusions, waiting periods, mental health cover, and long-term affordability. Tax benefits are now a bonus, not the reason.” This shift may not yet be captured in a single percentage figure, but it is increasingly visible in how conversations are unfolding at the point of purchase.

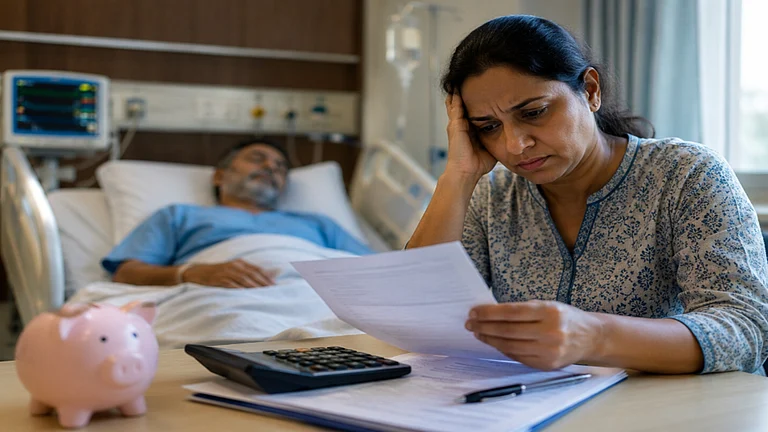

Maternity As A Catalyst For Early Planning

Maternity has played a particularly important role in accelerating insurance awareness.

With maternity waiting periods ranging from two to four years on most standard health insurance policies, women are forced to plan well before the need arises. That reality has created a more informed buyer, one who understands that insurance must be purchased before life events, not after them. “Maternity often becomes the entry point to a much broader protection conversation,” says Naidu. “Once women understand waiting periods and exclusions, they begin evaluating health and income risks far more seriously.”

The result is not just earlier purchase, but more deliberate decision-making.

Smarter Separation Of Protection And Investment

There is also a visible move away from bundled insurance-investment products.

Many women today prefer pure term insurance for income protection and separate instruments for wealth creation. Industry data supports this behavioural shift. Over the past two years, term insurance purchases by women have risen sharply, reflecting a clearer understanding that combining protection and investment often leads to inadequate cover and compromised returns.

“This is financial maturity,” Naidu notes. “Women are no longer being sold insurance as a product. They’re choosing it as infrastructure, something that quietly supports everything else in their financial lives.”

The Gap That Still Exists

Despite this progress, the protection gap remains significant.

Four out of five working women in India still do not have life insurance in their own name. Many contribute meaningfully to household income, yet the financial impact of their absence is often underestimated both within families and in financial planning conversations.

Health coverage gaps persist as well. While insurance penetration has improved, women remain vulnerable to underinsurance across their lifetime, even as their healthcare needs tend to be higher and more prolonged.

What This Means For The Industry

Products must reflect real female health journeys, not stereotypes. Communication must address women as primary decision-makers, not secondary beneficiaries. And transparency - especially around claims, exclusions, and long-term costs - is no longer optional. “The future growth of insurance will come from consumers who understand protection deeply,” Naidu says. “Women are leading that shift not loudly, but decisively.”

This International Women’s Day, the story isn’t about women being included in insurance conversations.

It’s about women rewriting them on their own terms.