Summary of this article

Modern retirement planning needs more than a single figure. It needs a structured approach that can handle inflation, longer life and unexpected costs.

A retirement corpus that appears comfortable on paper can quickly come under pressure if these costs are not planned for.

Retirement today needs a plan that grows, protects and adapts. NPS helps create long-term growth. PPF and EPF offer stability and predictable returns.

For a long time, most of us believed that Rs 1 crore is the golden number to aim for retirement. It sounded simple and achievable. The problem is, the world has changed since then. Inflation has affected healthcare. Education, the real estate sector and even grocery bills. Not to mention people are living longer. The fact is, one crore will not go as far as it used to. Which is why pension planning in India has become important. Nowadays, retirement planning is more of a strategy than just one magical number. It has to factor in inflation, increased life expectancy and sudden medical emergencies.

This is why a balanced financial plan matters. A long-term plan needs growth to counter inflation. It also needs stability for capital protection.

“For most Indians, the right mix often includes the National Pension System (NPS) for market-linked growth, and PPF or EPF for dependable fixed-income comfort. Mutual funds also add important layers of long-term growth. Together, they create a retirement plan that grows with discipline and protects when needed,” says Vishwajeet Goel, Head of Pensionbazaar, a retirement planning platform.

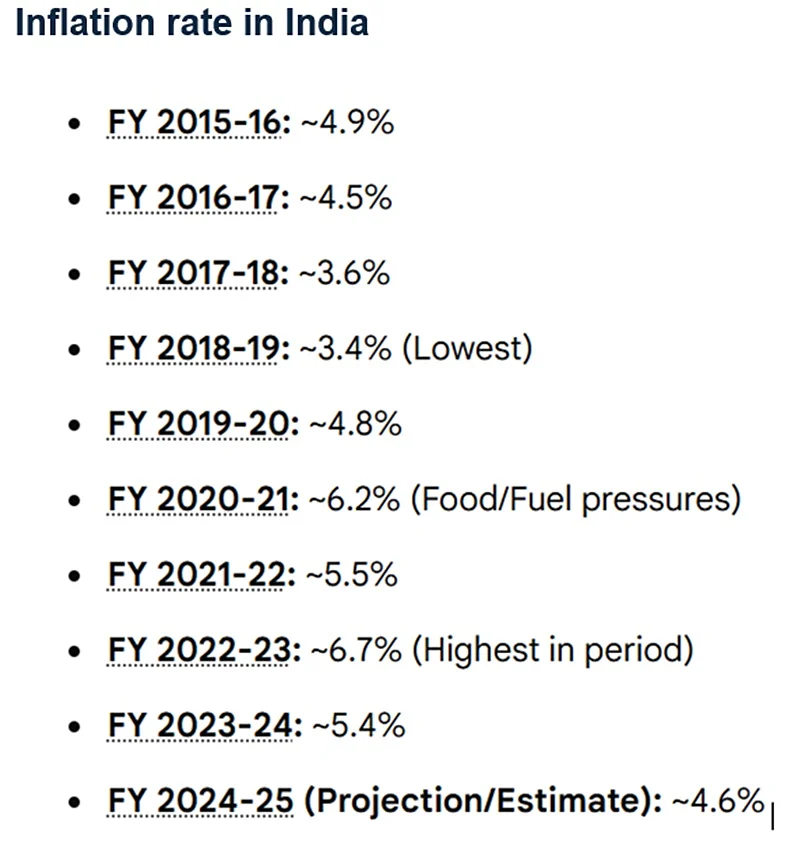

How Inflation Eats Into Buying Power

Inflation quietly erodes what money can buy over time. Take a simple example. If a set of goods costs Rs 1,00,000 today, the same basket will cost about Rs 2,65,000 after 20 years at an inflation rate of 5 per cent. Looked at another way, Rs 1,00,000 today will have the buying power of only around Rs 37,700 two decades from now.

The risk becomes sharper with healthcare. Medical inflation in India is often higher than general inflation. “As people age, vulnerability to lifestyle diseases such as diabetes, heart conditions and joint problems increases. Hospitalisation, medicines, diagnostics and long-term treatment can run into lakhs over time. A retirement corpus that appears comfortable on paper can quickly come under pressure if these costs are not planned for. This is why inflation, especially medical inflation, is often called the silent killer of retirement savings,” informs Goel.

Why NPS Deserves A Central Role In A Retirement Portfolio

NPS stands out because it balances growth and stability through a clear structure. Under the updated NPS rules, eligible investors can now take up to 100 per cent equity exposure, offering greater flexibility for younger contributors. This helps early-career earners benefit from long-term compounding. Equity grows faster over long periods. Early exposure helps a small contribution turn into a large corpus over time.

Recent returns show this clearly. One Tier I equity fund under NPS delivered a 14.82 per cent return in the past year. Over three years, many long-running NPS equity schemes have averaged around 13.5 per cent.

“As investors get older, NPS shifts towards safety. The auto-choice option steadily reduces equity and increases corporate bonds and government securities. This protects gains made in earlier years. It also reduces volatility as retirement approaches. Those who want control can use active choice. The default option still handles rebalancing automatically. Tax benefits under 80CCD make the product even more efficient,” says Goel.

However, there is a catch. At age 60, you can withdraw 60 per cent of the NPS corpus tax-free. The remaining 40 per cent must be used to buy an annuity, and the income from that annuity is taxable as per your slab. This differs from PPF, which is completely tax-free at withdrawal.

Another important advantage is discipline. The NPS lock-in ensures savings stay untouched for the long term. With this mix of growth and protection, NPS becomes more than a savings tool.

How PPF And EPF Provide Stability And Predictability

NPS works best when steady instruments support it. PPF and EPF provide this support. These instruments offer stable returns and also preserve capital. Best of all, they’re ideal for investors close to retirement who cannot afford to take big bets in the market. PPF comes with a long lock-in and a government guaranteed interest rate. EPF accumulates through your contributions and the interest earned over your working life. Top it up with your employer’s contributions and you have a very strong safety net. Together, NPS, PPF and EPF allow you to build a portfolio that can grow with you and provide stability when you need it.

Why Financial Planning Must Start Early

Starting early is a real game changer. Time allows compounding to work quietly and efficiently. Young earners can invest small amounts in NPS and combine them with PPF or EPF. They can also include mutual funds and Unit Linked Pension Plans (ULPPs). Over decades this creates a large and dependable pool. As the investor ages, they can shift to safer instruments. This keeps the plan aligned with changing priorities.

“Diversification also matters. Equity gives growth. Debt gives safety. A mix protects the investor from any single market shock. Fixed deposits and ULPPs also play an important role. FD offers good stability with steady interest rates. ULPPs today provide competitive long-term market-linked returns along with life cover, making them a strong addition to retirement planning. A combination of these tools builds a retirement plan that is practical and resilient,” observes Goel.

Conclusion

One crore is no longer a guarantee of security at sixty. Retirement today needs a plan that grows, protects and adapts. Your long-term corpus is built through NPS. You attain stability with instruments such as PPF and EPF which give you guaranteed returns. FDs, mutual funds and pension ULPPs balance your portfolio further. Not one instrument can stand alone but together they provide you with a diversified portfolio that enforces financial discipline. This portfolio is what you need to prepare for your retirement. Retirement goals include taking care of your ever-increasing expenses due to higher standards of living, higher longevity and medical costs. The right time to build this plan is now.