Summary of this article

The shift towards a higher basic salary will increase taxable income for many employees, particularly those who were earlier drawing less basic pay and relying on more tax-efficient allowances.

While there may be some loss of flexibility in salary structuring, a significant increase in taxable income is not expected, as employers are likely to restructure compensation in a manner that broadly neutralises the impact.

Employees should reassess their revised salary structure by evaluating the new basic-to-allowance ratio and computing tax liability under both regimes.

For many salaried employees, a pay hike usually brings a sense of comfort - until the take-home figure tells a different story. With India’s new labour codes coming into play, that gap between what you earn on paper and what you actually receive could become even more noticeable.

At the centre of this shift is the new rule: basic pay must account for at least 50 per cent of your total compensation. It may sound like a small change, but its impact is anything but minor. Changing your salary structure impacts your take-home pay.

Impact Of 50% Basic Pay Rule on Salaried Individuals

According to tax experts, the shift towards a higher basic salary will increase taxable income for many employees, particularly those who were earlier drawing less basic and relying on more tax-efficient allowances such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), and education allowance, among others.

“As basic pay is fully taxable, the reduction in exempt allowances may result in higher tax deducted at source (TDS). However, this impact is partly offset by increased provident fund (PF) contributions (if contributing on actual), with the employee’s share qualifying under Section 80C and improved gratuity benefits,” says Pratham Aggarwal, employment matters expert at SVAS Business Advisors LLP.

Overall, while there may be a marginal increase in tax outgo, the change strengthens long-term retirement savings and should be viewed in a balanced manner.

Will Higher Basic Pay Tilt Preference Toward The New Tax Regime?

The 50 per cent basic pay rule is unlikely to significantly increase the attractiveness of the new tax regime. Since the new regime disallows most exemptions and deductions, a higher basic salary does not provide any incremental benefit. Under the old regime, however, a higher basic component does proportionately increase HRA exemption.

“Moreover, enhancement in the limit of meal voucher allowance, child education allowance, and fuel expenses supports deductions like Section 80C. Therefore, taxpayers with rent obligations or structured investments are likely to find the old regime more beneficial. The new regime may still suit individuals with limited deductions, but it does not gain a distinct advantage due to this structural change,” points out Aggarwal.

Can Higher PF Contributions Lead To Any Direct Tax Benefits Or Liquidity Constraints For Taxpayers?

The New Labour Code defines ‘wages’ as all remuneration payable to an employee for work performed, subject to specified inclusions such as basic pay, dearness allowance and retaining allowance and exclusions such as HRA, conveyance allowance, bonus, etc. Importantly, if the total value of these exclusions exceeds 50 per cent of the overall compensation, the excess must be added back to 'wages' for the purpose of calculating statutory contributions such as provident fund (PF) and gratuity.

Says Sandeepp Jhunjhunwala, Partner, Nangia Global, “Under the earlier framework, there was no requirement to link PF contributions to a minimum percentage of total compensation. As a result, employers commonly structured salaries in a way that maximised employees' take-home pay. With the implementation of the New Labour Code, however, PF contributions need to be recalculated on a higher wage base. This could increase the mandatory employee contribution (typically 12 per cent of wages), thereby reducing take-home salary. However, for employees contributing only up to the statutory wage ceiling of Rs 15,000 (ie, Rs 1,800 per month), contributions beyond this limit are not mandatory and would depend on the employee's choice.”

Higher PF contributions mean lower liquidity in the near term since take-home pay is lower. However, the PF contribution by the employer helps you get tax benefits. They are not taxable income to you (subject to the overall annual limit of Rs 7.5 lakh contribution to all retirement funds). This will reduce the effective tax rate of your employee income.

Additionally, for individuals opting for the old tax regime, higher employee PF contributions are eligible for deduction from gross total income under Section 123 of the Income-tax Act, 2025 (corresponding to Section 80C of the earlier Income-tax Act, 1961).

“Although the new social security framework replaces the earlier PF law, the existing EPF Scheme, 1952, is expected to continue to apply during the transition period until a new scheme is notified. Importantly, the current wage ceiling of Rs 15,000 per month, effectively capping PF contributions at Rs 1,800 per month for both employer and employee, remains relevant. As a result, even though the new law broadens the definition of ‘wages’, in practice, PF contributions may continue to be computed based on the earlier structure (ie, 12 per cent of basic salary), subject to the statutory ceiling,” informs Jhunjhunwala.

Will This Change Significantly Increase Taxable Income For High-Income Earners?

It's unlikely that taxable incomes for top earners will materially rise as a result of just this change. While the requirement to allocate a higher proportion of compensation to ‘wages’ may reduce the scope for tax-efficient structuring through certain allowances, most employers are expected to realign CTC structures to ensure that the overall cost to the company remains unchanged and the tax impact is largely neutralised.

“Importantly, the shift primarily results in a reallocation of salary components rather than an absolute increase in income. In many cases, the higher basic pay will be offset by a corresponding reduction in allowances, with no significant change in gross taxable salary. Further, increased employer contributions to retirement benefits within the prescribed tax-exempt threshold of Rs 7.5 lakh, along with higher gratuity accrual (which is not taxed at the time of contribution), may provide some tax efficiency,” says Jhunjhunwala.

Accordingly, while there may be some loss of flexibility in salary structuring, a significant increase in taxable income is not expected, as employers are likely to restructure compensation in a manner that broadly neutralises the impact.

Grey Areas Or Compliance Challenges

One issue that seems uncertain with the new labour codes is the mismatch between labour law and income-tax rules. Gratuity is an example. The New Labour Code has expanded the definition of ‘wages’ for computation of gratuity (potentially allowing higher gratuity. So, you could see a part of your higher gratuity getting taxed, defeating the purpose of tax saving.

“Until corresponding amendments are made under income-tax laws, employers will need to carefully compute the tax-exempt portion of gratuity based on the existing criteria and ensure appropriate tax withholding at the time of payout, particularly during full and final settlements,” advises Jhunjhunwala.

How To Reassess Salary Structures And Tax Planning

As the new rules have come into force, tax experts advise employees to reassess their revised salary structure by evaluating the new basic-to-allowance ratio and computing tax liability under both regimes.

“The focus now shifts to optimising other exemptions available, such as HRA and LTA. Higher contribution to PF will wipe off a part of the 80C limit, so you may have to revisit your investments there,” adds Aggarwal.

Employees will also have to plan for a lower take-home salary as PF deductions will be higher. Each individual case must be assessed, and one cannot assume the convenience of employer-provided structures without analysis.

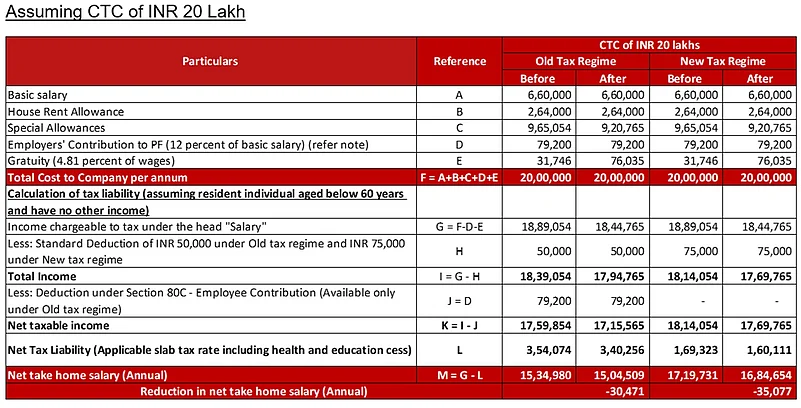

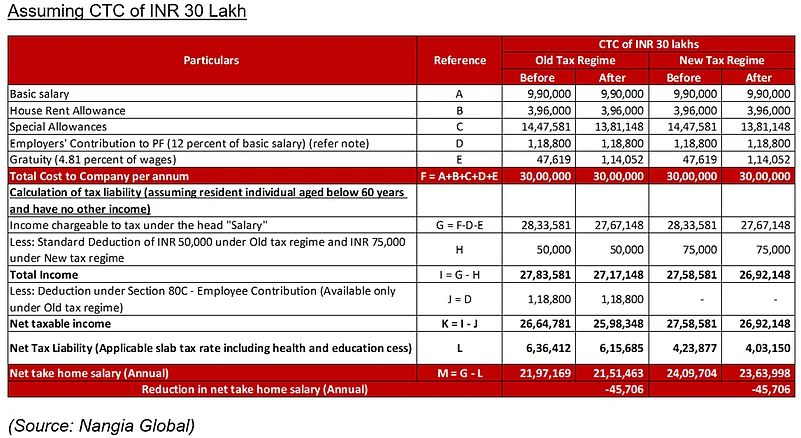

Example: The following table depicts the effect of the New Labour Code on payroll composition, tax payable and take-home pay for employees with CTC of Rs 20 lakh and Rs 30 lakh, respectively.

(Please note that for the purpose of this computation we have assumed that the employee would be contributing PF on the basic salary under both the erstwhile labour law and under the new labour code. As PF contribution over INR 1,800 is not mandatory (both under the erstwhile labour law and the new labour code), any contribution to PF over INR 1,800 would be voluntary)