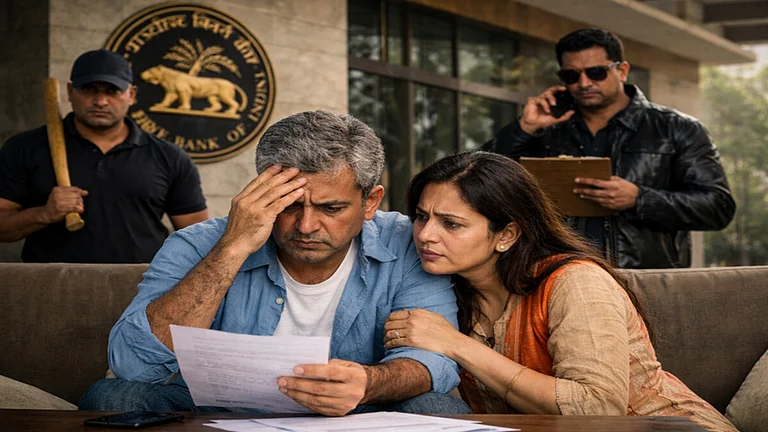

Loans taken need to be paid back, but even if you cannot pay it back, loan recovery agents cannot harass you. Stories of harassment by loan recovery agents often make headlines, so it is important to know your rights.

Know Your Rights

“While the lender has the option to initiate recovery in case of defaults, the Reserve Bank of India (RBI) rules clearly stipulate that they should not resort to undue harassment viz; persistently bothering the borrowers at odd hours, use muscle power for recovery of loans, etc. Recovery should normally be made only at a central designated place,” says Adhil Shetty, CEO, BankBazaar.com.

Field staff shall be allowed to make recovery at the place of residence or work of the borrower only if the borrower fails to appear at a central designated place on two or more successive occasions.

Furthermore, recovery agents are required to adhere strictly to specific communication guidelines, restricting contact with borrowers to the hours between 8:00 AM and 7:00 PM. “They are also required to use only the contact numbers provided to the borrower by the bank. Additionally, agents are required to present proper identification and an authorization letter from the bank to ensure transparency and accountability,” says Pranav Bhaskar, partner & head of corporate practice, SKV Law Offices.

The lender cannot take any actions, such as acquiring or auctioning your property or assets kept with the lender as collateral, without providing you ample notice of 30-60 days. If you are unable to reach an agreement with the bank during this period and the lender takes steps to auction the asset, they are mandated to get the valuation done from an approved valuer. This ensures that the repossessed asset is not sold at any price determined unilaterally by the lender.

“In case you believe that the valuation is incorrect or undervalued, you have the right to contest it. Also, if the sale proceeds from the auction of the asset is more than the total outstanding dues, then you are entitled to receive the balance amount from the lender,” says Shetty.

Finally, and most importantly, you are entitled to humane and dignified treatment during the entire process. You are entitled to protection from harassment, coercion, and undue interference.

What To Do In Case Of Harassment

In instances where the RBI’s recovery guidelines are violated, borrowers should immediately report the matter to the concerned bank. “Providing specific details, including the identity of the agent and the nature of the incident, can facilitate prompt action.

If the bank fails to respond adequately, borrowers have the option to approach the banking ombudsman, a designated authority to mediate and resolve disputes between banks and customers,” says Bhaskar.

Legal Protection

Borrowers who are subjected to harassment by recovery agents are afforded robust legal protections. “In instances of intimidation or coercion, they are entitled to lodge a complaint with law enforcement under provisions of the Bhartiya Nyaya Sanhita, 2023 (BNS), including but not limited to Section 351 (criminal intimidation) and Section 351(2) and (3) (punishment for criminal intimidation),” says Tushar Kumar, advocate, Supreme Court of India.

Additionally, borrowers may seek injunctive relief or damages through civil courts to address emotional distress or other injuries occasioned by the misconduct of recovery agents. Under the aegis of the Consumer Protection Act, borrowers may also institute proceedings before consumer forums if the actions of recovery agents constitute an unfair trade practice.

“It is imperative for borrowers to meticulously document all incidents of harassment, including call logs, messages, and witness testimonies, as such evidence is indispensable in substantiating their claims. Furthermore, borrowers must remain cognizant of the fact that no recovery agent possesses the legal authority to unilaterally seize property or assets without adherence to due process of law,” says Kumar.

Misconception Among Borrowers

There exist several misconceptions among borrowers with respect to their legal rights vis-à-vis loan recovery agents. A prevalent fallacy is the belief that recovery agents can arbitrarily confiscate property or assets; however, such actions necessitate a court-sanctioned legal process.

Additionally, borrowers often erroneously assume that they are obligated to respond to recovery agents at any time; the RBI explicitly restricts communication to designated hours, reinforcing the primacy of the borrower’s convenience and privacy. “Another misapprehension is that recovery agents wield unchecked authority; on the contrary, their actions are circumscribed by stringent regulatory oversight, and financial institutions bear vicarious liability for any misconduct,” says Kumar.

Finally, some borrowers perceive harassment as an inevitable consequence of loan defaults, whereas the law unequivocally provides avenues for redress and the assertion of dignity. “A thorough understanding of these rights enables borrowers to address such challenges with confidence and recourse to the rule of law,” says Kumar.

Also, follow Outlook Money's Budget 2025 expectations stories here.