You click Book Now, pick your seat, maybe add a meal and quietly, almost invisibly, a travel insurance cover slips into your ticket. For a few extra rupees, your train or flight journey suddenly promises protection too. It’s convenient and feels reassuring.

But here’s the catch: you usually end up buying bundled travel insurance without reading the fine print. What looks like a smart safety net can turn out to be a patchy cover with sub-limits, exclusions, and other surprises that spring up at the time of claim. So, before you pay that small add-on fee, it’s worth asking: is it worth it?

We unpack bundled insurance that comes with train and flight tickets to help you decide if you need it or should you go for standard travel insurance.

1 July 2026

Get the latest issue of Outlook Money

Bundled Rail Insurance

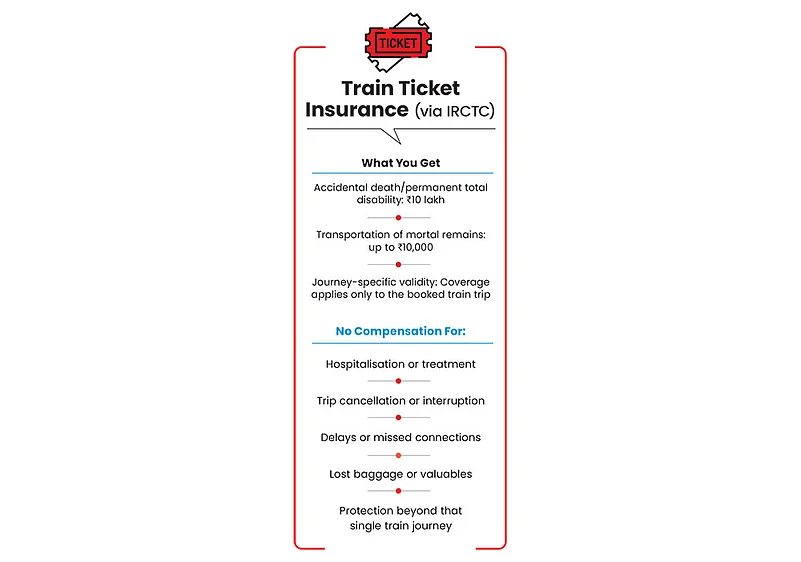

Launched in 2016, the Optional Travel Insurance (OTI) policy offered by the Indian Railway Catering And Tourism Corporation (IRCTC) provides Rs 10 lakh compensation to passengers in the event of death or permanent total disability. The premium is 45 paisa for a single trip. This is exclusive to passengers booking tickets via IRCTC’s website or mobile application.

“No such provision exists for passengers with unreserved tickets, season tickets, or reservations made via Passenger Reservation Systems (PRS). This suggests that the primary objective of introducing OTI was to reduce congestion at reservation counters and promote digital or cashless transactions rather than to provide an additional safety net for train passengers,” says Raju Meka, deputy manager, The New India Assurance Co.

The coverage supplements the compensation of Rs 8 lakh guaranteed under the Indian Railway Act, 1989. This means OTI opt-in passengers are eligible to receive a total of Rs 18 lakh compensation in the event of a train accident resulting in death or permanent disability. The Rs 8 lakh cover is guaranteed for all bona fide passengers with a valid ticket, and you do not need to purchase any additional insurance for that.

Additionally, the OTI policy offers a dedicated benefit of Rs 10,000 towards the transportation of the mortal remains to the victim’s home. Though modest, this benefit provides significant support to bereaved families amid the chaos following an accident, something statutory provisions often overlook.

Should You Opt For It? The 45 paise premium for a single trip for Rs 10 lakh coverage appears remarkably low because it has been democratised on a per-person, per-journey basis.

Even when calculating the annual premium based on average train travel duration, the cost is affordable.

“Considering that average train journeys in India last between 18 and 36 hours, the annualised premium per person effectively ranges from Rs 110 to Rs 219 for Rs 10 lakh coverage. This translates to an annual premium of roughly Rs 11 to Rs 22 per lakh coverage. Still the premium is quite modest,” says Meka. Note that this is just for comparison; you can add travel insurance only per ticket, per trip.

What To Keep In Mind: Once a passenger opts for OTI, an email is sent requesting nominee details. If this step is skipped, family members must submit a succession certificate or legal heir certificate to establish kinship with the deceased. This process often leads families to court, particularly when multiple legal heirs dispute the claim amount.

Also, once insurance is opted for, all further correspondence must be handled directly with the insurance company. IRCTC acts merely as a facilitator for policy issuance and assumes no responsibility thereafter.

Further, it lacks additional features such as hospital daily cash, children’s education grants, or loan protection or equated monthly installment (EMI) cover, which are common in conventional policies.

Essentially, it’s an accident-only cover, which cannot substitute a full travel insurance cover.

How To Make A Claim: If an accident occurs, the passengers or their next of kin can contact the insurer directly. One of the primary advantages of OTI is that policy copies, along with terms and conditions, are sent to passengers via email. This transparency eliminates ambiguity during emergencies and helps contact insurers promptly.

In contrast, statutory compensation under the Railway Act, 1989, often remains opaque, with passengers frequently unaware of their entitlements or claim procedures.

Whenever a train accident occurs, the kin of the deceased or injured passenger must file an application before the Railway Tribunals to seek statutory compensation under the Act. The eligible compensation is released only after a formal legal process, which may take several years. “Even interim relief or ex-gratia payments require an application before the tribunal. This prolonged process can exhaust the rightful kin,” says Meka.

Bundled Flight Insurance

Typically, travel insurance that comes with flight tickets is offered on an “opt-in” basis.

Says Chandrakant Said, vice president, consumer underwriting, TATA AIG General Insurance: “The travel insurance premium of such an offering varies and mainly depends upon the number of benefits included, their limits/sub-limits, area of coverage, age of the insured, and trip duration. Because of the potential to sell a high volume of travel policies, opt-in travel insurance can come at a lower premium than a standalone travel insurance product purchased separately.”

Travel insurance bought as an add-on is usually inexpensive, up to just Rs 300 for domestic trips and Rs 150-800 for international travel, but typically offers only limited, basic coverage. In contrast, comprehensive standalone travel insurance generally costs about Rs 300-1,200 domestically and Rs 800-4,500 or even higher internationally, depending on the location, age, and other factors.

Bundled Vs Standalone: The additional cost in standalone travel insurance, typically, translates into substantially broader coverage, fewer exclusions, and more comprehensive protection. The difference in premium generally reflects the enhanced benefits—particularly in areas, such as medical treatment, emergency evacuation, and trip cancellation coverage—where bundled airline plans often have limited provisions.

“Overall, it is imperative not to evaluate travel insurance solely on price. Instead, travellers should assess the overall risk exposure and the potential financial impact of the unforeseen events, which can be far more significant than the difference in premium,” says Anshul Mittal, joint president and appointed actuary, HDFC ERGO General Insurance.

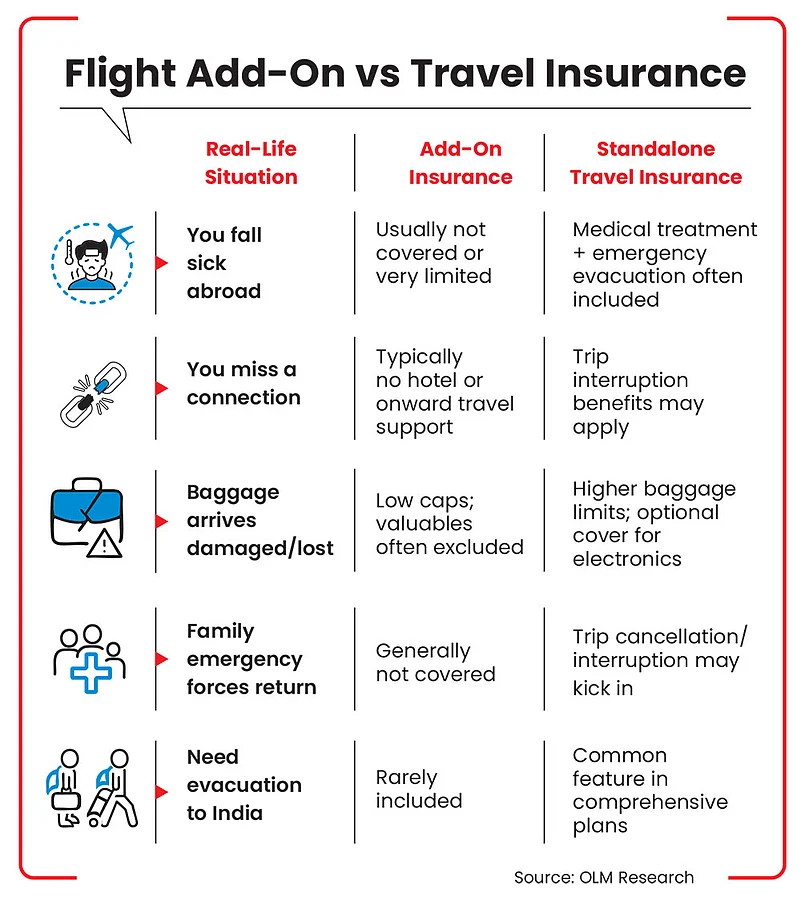

Bundled airline plans often exclude or limit several key protections that standalone policies provide. “Bundled products are usually group plans with sub-limits or payout restrictions, and standalone plans have higher sub-limits and are more comprehensive,” says Meet Kapadia, head of travel insurance, Policybazaar.

One, many airline plans offer minimal or no medical coverage or only cover emergencies tied directly to flight incidents. “In contrast, standalone travel insurance plans offer substantially higher medical and emergency evacuation coverage, protecting travellers against risks that can arise abroad,” says Mittal.

Two, standard airline add-on policies, typically, cover only flight-related cancellations and do not protect the overall trip or cancellations arising from other life events such as illness, injury, or family emergencies. “In contrast, comprehensive standalone travel insurance plans often include trip cancellation and trip interruption benefits, usually with higher limits and wider triggers,” says Mittal.

Three, airline bundled policies operate on a one-size-fits-all model, offering little to no flexibility. In contrast, comprehensive standalone travel insurance allows travellers to tailor coverage based on their itinerary, risk factors, trip value, and personal needs.

Four, baggage coverage in airline plans has low caps and often excludes valuables such as electronics and jewellery. However, standalone policies can include optional endorsements for expensive gear, adventure sports, and others.

“It’s also important to note that, in absolute terms, travel insurance remains a small fraction of the total trip cost. This means that choosing a bundled plan over a standalone one usually doesn’t translate into significant real-world saving, while the reduction in coverage can be substantial,” says Mittal.

Should You Opt For It? Bundled travel insurance plans are often priced lower because they are structured to offer standardised coverage with defined limits on key benefits, such as medical expenses, trip cancellation, or baggage loss. The pricing is, therefore, linked to the scope and limits of coverage.

“For travellers, especially those undertaking short, low-risk trips, bundled plans can be cost-effective, as they combine essential protections under one policy at a consolidated premium,” says Rakesh Kaul, chief distribution officer of retail business, Bajaj General Insurance. However, it is important to review the sub-limits, deductibles, and exclusions carefully to ensure the coverage aligns with the nature and duration of travel.

Frequent travellers or those going on long international trips should opt for wider coverage with a standalone policy that provides higher medical coverage or broader trip protection.

In any case, don’t forget to do your due diligence and buy a policy whose coverage satisfies you.

meghna@outlookindia.com