Summary of this article

If you’re paying high fees for a policy with mediocre returns, getting out early will sting. But watch those fees over the long term - they can exceed your upfront surrender charges.

Traditional life insurance plans commonly offer policyholders returns of just 3–6 per cent. Many buyers don’t even realize this until reading the fine print.

Term insurance with a dedicated investment vehicle can leave you with a better overall long-term solution.

Consider converting to a paid-up policy or waiting for a lock-in period to expire before surrendering.

We have often heard that surrendering a life insurance policy is a mistake. Walk away early, and you lose money. Stay the course, and the policy will eventually prove its worth. It sounds reasonable. In practice, it often isn't.

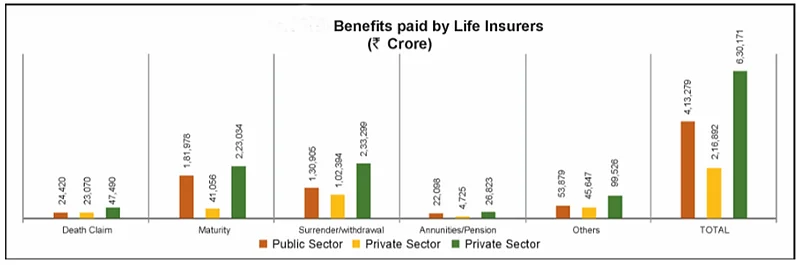

According to the RBI’s Financial Stability Report, total benefits disbursed by life insurers witnessed a sharp increase from Rs 4 lakh crore in 2020-21 to Rs 6.3 lakh crore in 2024-25. "Scheduled maturity as a percentage of benefits shows a declining trend, indicating a shift from scheduled maturity towards unscheduled exits," it states.

IRDAI data for FY 2024–25 shows surrender and withdrawal payouts touched Rs 2.33 lakh crore. Behind that number are millions of policyholders who bought something they did not fully understand and eventually stopped pretending otherwise.

“Most of these policies were not bought badly on purpose. They were bought in March, under tax-saving pressure. Or recommended by someone trusted, without adequate explanation of what the returns actually looked like over time. Traditional life insurance plans, in many cases, deliver 3–6 per cent annualised returns, quietly, without ever being said aloud at the time of sale,” says Manju Dhake, Head - Insurance Advisory Practice, 1 Finance.

The cost of exiting early is real. Surrender values in the first couple of years are painfully low, sometimes a fraction of what you paid in. That sting. And that sting is precisely what keeps people locked in, year after year, hoping the math eventually works in their favour.

But the question worth asking is not "How do I recover what I've already paid?" That money is gone regardless. The real question is: What happens to my finances if I stay versus if I leave?

“In many cases, even after absorbing the surrender loss, reallocating those funds into a term cover that truly protects your family and a separate investment that builds wealth can deliver better outcomes over ten years than continuing with a policy that was never suited to your needs,” says Dhake.

There are intermediate options worth considering: making a policy paid-up stops future premium outgo while preserving some value. For ULIPs, for instance, waiting until the five-year lock-in ends before exiting avoids unnecessary penalties. These are useful where full surrender feels premature.

But where the product fundamentally does not fit, has inadequate cover, poor returns, or no alignment with where your life is now, staying in it is not cautious. It is just inertia.

“Surrendering a policy is not a failure. Buying the wrong one was an error. Recognising that early and correcting it with a clear plan is simply good financial sense,” says Dhake.