Summary of this article

India’s unclaimed funds have witnessed an exponential rise in the last five years, driven by a lack of succession planning, asset documentation, and financial literacy at large.

The issue goes beyond regular savings. There are over 31.87 lakh dormant EPF accounts holding Rs 10,915 crore.

Mutual funds held Rs 3,452 crore in unclaimed dividends and redemptions in FY2024-25, and even REITs, InvITs, and NCDs now contribute Rs 764 crore in forgotten distributions.

Digitalisation has not solved the forgotten wealth problem; it has simply given it new addresses.

A new study by 1 Finance Research has mapped unclaimed assets worth Rs 2.2 lakh crore lying with banks, financial institutions and market utilities as of December 2025. These assets lie dormant in various financial vehicles such as bank accounts, equity shares, insurance policies, provident fund accounts, mutual funds, and market-linked instruments. Such unclaimed funds have risen exponentially over the last five years, driven by a lack of succession planning, asset documentation, and financial literacy.

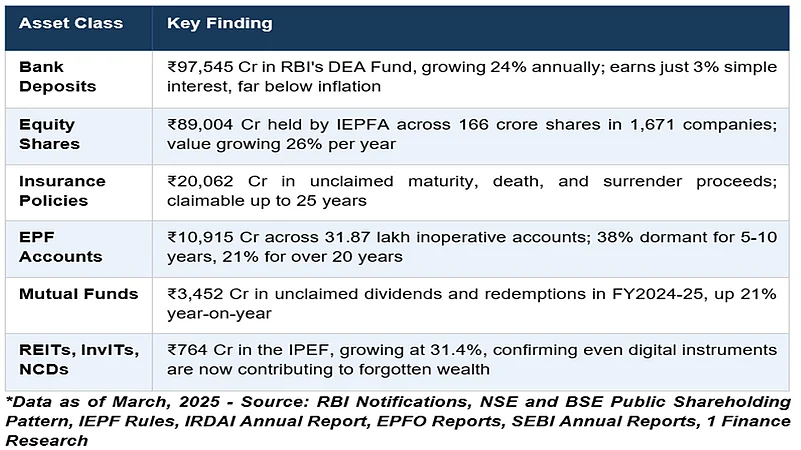

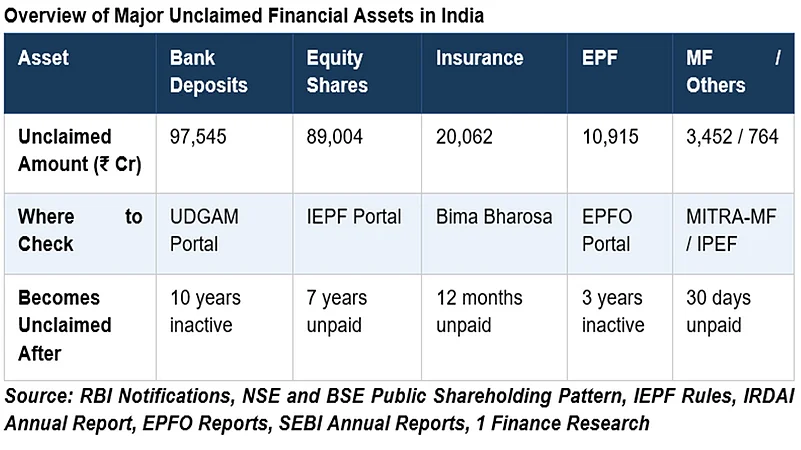

Assets unclaimed lie at every tier of the banking system. The largest share of unclaimed assets is in the form of bank deposits. Between March 2015 and December 2025, the RBI’s Depositor Education and Awareness (DEA) Fund corpus increased by nearly 34 times from Rs 7,875 crore to Rs 97,545 crore at the rate of mere 3 per cent simple interest while costs of living shot up manifold. The Investor Education and Protection Fund Authority (IEPFA) held 166 crore shares across 1,671 listed companies as on November 30, 2025. The shares are worth Rs 89,004 crore as on date (calculated on the basis of current market price of shares).

Reliance Industries alone accounted for 15.6 per cent of that value. Unclaimed insurance proceeds stand at Rs 20,062 crore at the end of FY2023-24, claimable for up to 25 years, though interest earned during that period accrues to the government fund, not the claimant as per Section 126 of the Finance Act.

The issue goes beyond regular savings. There are over 31.87 lakh dormant EPF accounts with Rs 10,915 crore in them. Even after the launch of the UAN system in 2014, inactive EPF accounts have risen from 9.8 lakh in the year 2020 to 31.9 lakh in 2025. Close to 50 per cent of unclaimed EPF money is locked up in 0.4 per cent of accounts. Mutual funds held Rs 3,452 crore in unclaimed dividends and redemptions in FY2024-25, and even REITs, InvITs, and NCDs now contribute Rs 764 crore in forgotten distributions, growing at 31.4 per cent annually. Digitalisation has not solved the forgotten wealth problem; it has simply given it new addresses.

Animesh Hardia, Senior Vice President, Quantitative Research at 1 Finance, says, “What struck us most in this research is that India's unclaimed wealth problem hasn't shrunk with digitalisation, it has actually expanded into new asset classes. We mapped over two lakh crores across six categories, from decades-old bank deposits to distributions from REITs and InvITs that are barely a few years old. The infrastructure to invest has outpaced the infrastructure to ensure that wealth reaches the people it belongs to.”

Conclusion

India's unclaimed wealth problem is not a relic of the pre-digital age. It is growing, diversifying, and now reaching into the most modern corners of the investment ecosystem. Three structural failures persist: poor nomination practices, low awareness of asset recovery mechanisms, and fragmented reclaim processes.

For households, the action is clear: every financial product needs an active nominee, updated contact details, and a documented trail for heirs. “Wealth that cannot be found cannot be used. And wealth sitting at 3 per cent in bank deposits while inflation runs higher is not saved, it is slowly lost,” says Hardia.