Summary of this article

· Seniors often face challenges managing multiple loans post-retirement

· A home loan top-up can aid in repaying high-interest loans

· Borrower should evaluate loan amounts carefully to avoid excessive borrowing

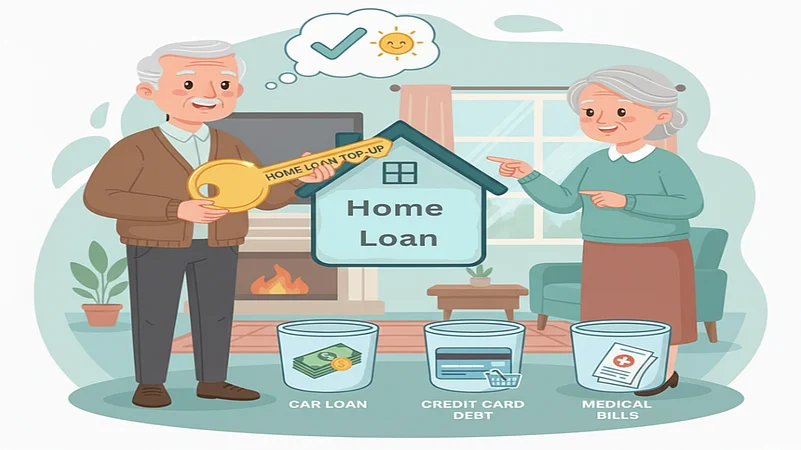

Seniors need a financially independent life after their retirement, and while doing so, they need to manage their loans efficiently. Multiple loans after retirement can be difficult to manage. If you have multiple loans, you may close some of them so that you can easily manage fewer loan repayments. Using a top-up on your existing home loan can help you reduce the size of your loan portfolio.

Rajat Kumar, Age 63, lives in Mumbai with his wife, Sharda Devi, Age 60. They took five loans for various purposes, including a home loan, a car loan, a personal loan, a travel loan, etc., and later experienced difficulty in remembering their repayment dates and managing them. People nearing retirement should try to minimise their loan exposure. What to do if you couldn’t close your loans and carry them in your retirement? You can use the highest loan, like a home loan, to get a top-up loan facility and use it to repay your other loans, especially those with high interest rates. Let’s check out the steps to set up a top-up facility for your home loan and how to manage it.

A home loan top-up facility is available only to existing home loan borrowers. Depending on the lender, there can be a minimum top-up loan amount that you can apply against your home loan. Usually, banks allow a top-up facility on a home loan with a residual repayment period of up to three years.

You can get a top-up loan in the form of a term loan or an overdraft (OD) facility. Typically, the interest rate on a top-up as a term loan is lower than that of the OD facility.

In most cases, a top-up loan can be applied for through online banking of your existing home loan lender, or you may also apply offline through your bank. The processing fee and interest rate on a home loan top-up facility are usually lower than those on unsecured loans and other alternative loan options.

Things To Keep In Mind

You should avoid taking a higher loan amount than what’s required. A top-up loan is secured against your home, and until you clear the entire loan amount, you won’t be able to get your home debt-free. You must evaluate between the OD and the term loan facility when applying for a top-up loan, and choose the one according to your repayment needs.

The author is an independent financial journalist